Low interest rates are a good thing, right? They are if you are a borrower, but not if you are a saver. People salting money away for retirement right now are getting almost no return on their savings, thanks in large part to a zero interest rate policy (ZIRP). Banks can borrow money from the Fed with no interest, so why would they pay interest on ordinary deposits, CDs, or any other money making instrument?

There is a lot of talk about the Fed’s policy of quantitative easing, which currently is performed by buying $85B in mortgage backed bonds every month. They may or may not start “tapering” to zero sometime in the near future. Beyond that, at some point interest rates have to come off of the peg of zero that they have been at since 2008, but that’s even further into the future. And the implications are vast.

The speculation that Barataria has centered around lately is that this economic cycle can’t last forever, and indeed is on track to end sometime around 2017-2018. Somewhere around that time there should be a year in which everything changes – and the economy picks up rather suddenly. Cheap money, pent up demand, and freeing up jobs by the retirement of Baby Boomers has to have an effect. There’s even reason to believe that the current labor force will not be able to make up for the loss of Boomers on its own, requiring skilled workers to be imported.

The speculation that Barataria has centered around lately is that this economic cycle can’t last forever, and indeed is on track to end sometime around 2017-2018. Somewhere around that time there should be a year in which everything changes – and the economy picks up rather suddenly. Cheap money, pent up demand, and freeing up jobs by the retirement of Baby Boomers has to have an effect. There’s even reason to believe that the current labor force will not be able to make up for the loss of Boomers on its own, requiring skilled workers to be imported.

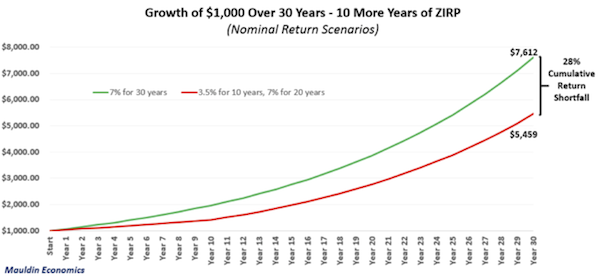

But that doesn’t mean that everything is rosy. An extended period of zero interest rates, already in its fifth year, means that saving is almost a stupid idea. The driving force behind a move away from fixed pensions to a 401(k) model was that the private market would provide a greater return. What will GenXers get for the money they put away for their retirement? The answer is in this chart below, showing the difference between rates stuck at zero for the first 10 years versus a more typical rate of 3.5%, provided by John Mauldin:

Low interest rates make saving far less profitable.

Over 30 years, the difference between the two is a shocking 28% less compounded savings ready for retirement. While there may be more economic opportunities in the future for people of working age, those planning to retire around going to have to think twice – and probably keep working long past the 67-70 years they will have to live before they are eligible for Social Security (it rises gradually for GenXers).

Where the 2020s are likely to be a good time to be young, they are likely to be a lousy time to be old.

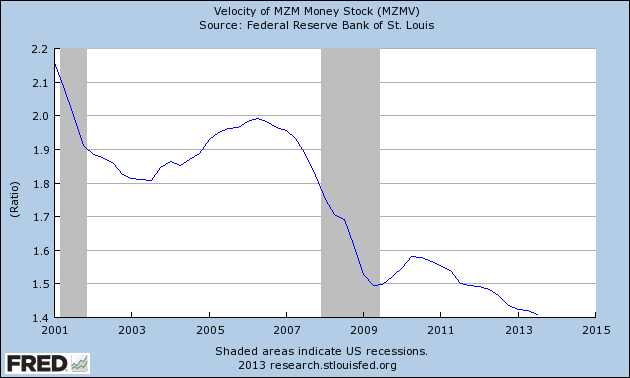

That’s not to say that zero interest is likely to continue forever. As shown before, the key interest rate should probably already have risen to 1% or so, and would have if there was any sign of inflation on the horizon. But with all the money out in the economy that can change very quickly. Consider for a moment the continuing drop in the velocity of money, or the number of times that the money which is out there turns over in any given year. It’s still dropping as Fed policy encourages the growth of the money supply well ahead of the growth in the economy. Updating the graph from the last time we looked at this 17 months ago shows it’s still diving:

The broadest measure of money supply shown by how often it turns over in the economy. It’s still diving.

That means that once things turn around there could be a very sudden rise in inflation. And that turnaround will come from upward pressure on wages caused by the labor shortage we will certainly see once the Baby Boomers retire. It’s inevitable that money will turn around faster and, if there’s too much of it, will devalue through inflation.

So we can’t reasonably expect zero interest rates to be with us forever. Once again, there has to be a year in here when everything starts to change – and 2017 is looking like the best bet for that if it doesn’t happen before then.

No one can ever say that low interest rates are always a good thing – it depends entirely on where you are in life and what you need. Working people benefit from low rates, at least as long as labor is not at a horrible disadvantage to the capital markets. Retirees usually benefit from higher rates, especially when they are keeping inflation in check.

But the current rates cannot continue forever. They may be able to stay historically low through the 2020s if economic growth stays relatively low, but interest can’t be at zero forever. The day it starts to change will be huge.

Zero interest rates can’t go on forever. I think we will see them rise as early as next year.

If they do that, it will be towards the end of the year and only a quarter point. But it is possible, yes.

I stand by my prediction of a “normal” Fed Funds Rate in the 2%+ range in 2017 or so – unless inflation does suddenly heat up.

I think its safe to say that the 401k system is broken right now. Anyone who wanted to retire on it is not going to be able to. I don’t know what the answer is, maybe it’s more social security or something. But something has to give. I don’t think the baby boomers will retire as quick as you think they will.

I think I have to agree with that. It does seem that with no good return on the horizon it’s not something that anyone can count on. With low inflation the real return is still decent, but it’s not much. Compound interest is just not a reality today.

Pingback: The Year Everything Changes | Barataria - The work of Erik Hare

Interest rates have been low for 5 years, I think we have adjusted to them by now.

Yes, there is no real “shock” in this. But it’s still hard on retirees, and we are about to have a lot more of ’em.