When is junk a good thing? When you can’t afford a new car, a rusty old one might do just as well, at least for a little while (even if it is purple, like mine). And if bond rates are so low that you might as well put your money in the mattress, you might also develop a taste for junk – junk bonds, that is, or more politely known as “high yield bonds”. It’s been the latest trend in the bond market and, strangely, it might be proof that things are getting better. It’s not the quality of the debt that really counts, it’s what they do with it.

The reason for the popularity of high yield bonds is two-fold. A good company can borrow a lot more if it’s willing to trash its credit rating, which they are usually not willing to do. In good times, a “junk” rating can cost around 4.5% more in interest – but with today’s low rates that penalty is only 2.5% or so. Investors like the additional return, often running around 7%, and are willing to look the other way if an otherwise well-run company is the one offering the extra vig.

The reason for the popularity of high yield bonds is two-fold. A good company can borrow a lot more if it’s willing to trash its credit rating, which they are usually not willing to do. In good times, a “junk” rating can cost around 4.5% more in interest – but with today’s low rates that penalty is only 2.5% or so. Investors like the additional return, often running around 7%, and are willing to look the other way if an otherwise well-run company is the one offering the extra vig.

It’s become a big industry, really taking off in 2012 and still accelerating today. The number of shares on Exchange Traded Funds in high-yield corporate debt (a kind of stock market for the things) doubled in February. There has been a bit of a pullback recently as investors apparently do not have an unlimited appetite for junk, however, and the market is still adjusting. But policy makers are so far not too worried about it. Fed Governor Jeremy Stein recently spoke at a Fed Symposium on the issue:

My reading of the evidence is that we are seeing a fairly significant pattern of reaching-for-yield behavior emerging in corporate credit. However, even if this conjecture is correct, and even if it does not bode well for the expected returns to junk bond and leveraged-loan investors, it need not follow that this risk-taking has ominous systemic implications. That is, even if at some point junk bond investors suffer losses, without spillovers to other parts of the system, these losses may be confined and therefore less of a policy concern.

To read between the lines a bit, as we always have to with the Fed, they see a healthy amount of risk in the market and as long as no one else gets hurt they aren’t going to intervene.

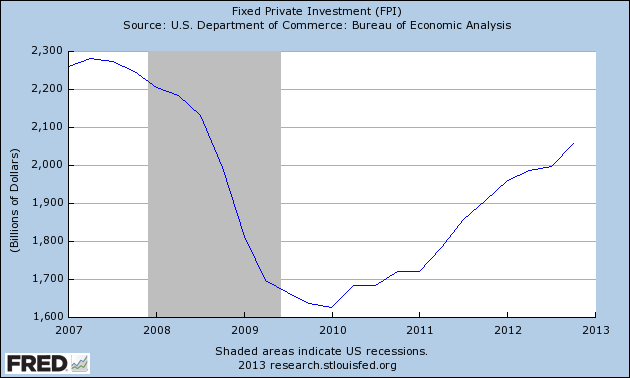

Where is this new flood of corporate bonds going? Some is going into stock repurchases, which is helping to puff up the market. But there has also been a decent rise in Fixed Private Investment – big equipment, land, buildings, and the like. It’s best shown in this chart from the St Louis Fed since 2007:

Like nearly everything else, the bottom came at the start of 2010 – but has been picking up nicely since then. The total rise of almost 30%, or $400B, is one of the most positive votes of confidence in the economy that we have. Some of that fixed investment is funded by junk bonds and represents a healthy investment in production. It’s a very positive sign for a turnaround.

What about the risk? Given the Fed’s opinion that it’s confined to the individual bonds and not shared across the system there is little reason to worry about it. This is a healthy sign that the money that has languished in the Fed and other places for years may finally be working its way into the economy. That can only be a good thing.

Overall the run to junk is a trend worth watching. As long as fixed investment picks up we can see the positive signs necessary for hiring to pick up and a general recovery to take hold. Given that the appetite for high yield is both logical and apparently not limitless it’s hard to believe that this is just another bubble waiting to pop. As long as the borrowing goes back into the economy it’s hard to say that this is anything other than what the Federal Reserve wanted to see happen all along.

Junk is good – especially when it can get the job done!

I agree that it is a positive sign & I don’t see a bubble forming at all. The recent shorting does prove that. Good blog!

Thanks! It’s another sign of a turnaround. There are many.

Hey, Mr. Sunshine is back! 🙂 No I agree this is positive especially if investment has picked up that much.

I prefer being upbeat when I can. 🙂

Interesting, I hadn’t heard of this trend. If investors are willing to take on more risk it may be a good thing, but more debt doesn’t sound so good even if rates are low. As you said if rates come up they will all be in trouble even if the Fed thinks its isolated. I guess this puts even more pressure on them to keep rates low.

That’s what I was discussing with the liability outstanding – and yes, there is a lot of pressure to keep rates low more or less forever. I think that will be the norm for a long time. But a little bit of managable risk is a good thing, yes!

Great blog, I really feel like I understand this issue.

Thanks!

Pingback: Risk and Reset – Who Pays? | Barataria - The work of Erik Hare

Pingback: Yellen’s Dashboard – Update | Barataria - The work of Erik Hare

Pingback: Crude and Junky | Barataria - The work of Erik Hare

Pingback: Coopertition | Barataria - The work of Erik Hare