The big story of the last 20 years has been a tale of two worlds coming together. While the developed world experienced a decade of growth in the 1990s followed by stagnation and decline in the 2000s, the developing world saw nothing but growth. The two phenomena are related in the tremendous expansion of credit and general money supply over this time, and are now starting to come together. The developing world is feeling the pinch the same as the developed world.

This story first appeared in Barataria back in September 2012, but it’s now quite fashionable to talk of the end of the great boom in “Emerging Markets” (EM). They have, simply, started to either mature or fall back. And investors are trying to find the next wave of fantastic growth stories to invest in.

One Big Marketplace

“The EM story is based on rapid growth, led by exports, which delivers large current account surpluses, which leads to the accumulation of foreign exchange reserves and the expansion of domestic credit,” according to David Lubin, head of emerging market economics at Citigroup. “Every single element of that story is no longer true.”

Some of the nations are quietly slipping back (Russia), others are finding ways to charge ahead and achieve superpower status (China), and some are seeking to normalized and mature into fully fledged developed economies (Brazil). The story is far from over, but the process of finding high-growth economies for global investment banks is going to be a lot stranger and riskier.

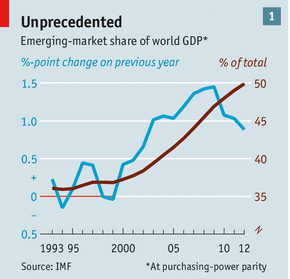

Chart from the Economist, date from the IMF

What we have seen in this period, however, is largely unprecedented in world history. Globalization has very much evened out the quality of life for people around the world, especially when you look at Purchasing Power Parity (PPP). This is a way of adjusting the size of an economy based on a basket of goods that can be bought locally – in short, because things are cheaper in a developing nation they can enjoy a good life with less money. Using this adjustment, half of the world’s net product comes from developing nations for the first time since such statistics were kept.

Arvind Subramanian and Martin Kessler of the Peterson Institute call it “convergence with a vengeance”. Rich, developed economies didn’t worry about growing balance of trade deficits with developing nations as new technologies such as the internet and containerized cargo hooked up the world. It was fueled by plenty of investment money that could fuel a rapid rise through global banks.

That can’t happen anymore. In many ways, the economic cycles that have strangled the developed world are finally catching up with the rest of the planet. It’s not possible for a nation to make a lot of money selling goods to the developed world because there just isn’t as much to give. It’s now up to the nations that experienced the big rises to normalize into consumer societies that generate their own consumption to keep it moving. A lot of credit and trade is no longer a ticket to a new generation of wealth.

Egypt has a lot to figure out

Is this the end? Investment bank Goldman Sachs, who first proclaimed the rise of the “BRIC” nations (Brazil, Russia, India, and China) in the last 1990s is now focusing on the “Next 11” (N11). This is a strange grab-bag of nations that include the largely developed South Korea, hopeful Mexico, horribly unstable Turkey and Egypt, all along with isolated Iran. It’s going to be a lot more difficult to pull of the same trick twice, but big banks like Goldman are known for throwing the dice hard these days.

“Long-term, emerging markets remain one of the most attractive asset classes,” says Christopher Cordaro, chief investment officer at RegentAtlantic Capital. “We know they’re going to be volatile, and we expect EMs to be the most volatile asset class in our clients’ portfolios.” But they are still the story for big growth in the long term according to investors. That’s even as the US appears to be pulling out of the worst of our own depression and possibly turning a corner.

When will this end? As Barataria has noted before, inequity is harmful for long term growth. As the world becomes one big economy, we can expect that struggling nations will be a drag for everyone. The problem will persist until the world has evened out substantially.

That is still what is happening, even as the developing world slows down and starts to look like a much riskier bet. That will make safer investments in the US look good – assuming we can get our act together, that is. The stakes for everyone are a bit higher all the time, and that includes us here at home. A faltering global economy is not good news for anyone.

The emerging markets relate to the end of the cold war.

Paris, Charter of (1990)

A declaration by all members of the CSCE (Organization of Security and Cooperation in Europe) which formally ended the Cold War between the NATO and Warsaw Pact alliances on terms wholly favorable to the Western alliance. It declared that future security relations within Eurasia would be based on liberal-democratic principles as enshrined in the Helsinki Accords, that is, upon the promotion of market economies and free flow and interchange of ideas, respect for human rights, and on the assumption of peaceful relations among law-abiding, free peoples.

signed by Austria, Belgium, Bulgaria, Canada, Cyprus,

Czech and Slovak Federal Republic, Denmark, Finland, France, Germany, Greece, Holy See, Hungary, Iceland, Ireland, Italy -European Community, Liechtenstein, Luxembourg, Malta,Monaco, Netherlands, Norway, Poland, Portugal, Romania, San Marino, Spain, Sweden,Switzerland, Turkey, Union of Soviet Socialist Republics, United Kingdom, United States of America and Yugoslavia

Paris, 19 – 21 November 1990

(greenwood encyclopedia of intl relations)

The Treaty on the Final Settlement with Respect to Germany was signed in Moscow, USSR, on 12 September 1990, and it paved the way for German reunification on 3 October 1990.

Under the terms of the treaty, the Four Powers renounced all rights they formerly held in Germany, including in regard to the city of Berlin. As a result, the united Germany would become fully sovereign on 15 March 1991, with Berlin as its capital. It would be free to make and belong to alliances, and without any foreign influence in its politics. All Soviet forces were to leave Germany by the end of 1994. (wikipedia)

A good point, I often forget the Cold War. Perhaps it’s from trying. So much changed after that and we could move to a more open economy globally – in addition to creating the great engine of Europe, Germany. More to think about, thanks!

I read an article yesterday on the BRIC , the emerging developing economies and the slowdown occurring there. So I will ask 2 questions. Please comment on Brazilian oil and India’s lack of oil. I still think that the Afghanistan war had to do with the future of an oil pipeline. Also read an article on tenure/turnover (or length of worklife) at some fortune 500 companies and found surprisingly that it is very short. Workers at Amazon esp. in their warehouses only last a year on average. Maybe that is an indication of the temp economy. Many other corporations had also short spans (taking into account that Amazon is still relatively new and growing and hence shorter). One of the firms with the longer career span was GM and not only had that had to do with unions but probably also that some younger staff were terminated In 2007-2009 leaving an older workforce. Hey what do you think of Consumer Reports making the Impala the car of the year beating some higher end Honda’s and Toyota’s. Hopefully the reliability will hold up.

India has many problems, and the lack of real resources is probably the worst. They also have a long way to go before they really turn the corner. Brazil has been doing an excellent job of not just using their resources but really adding a lot of value before they leave the nation – bauxite becomes aluminum (after the Amazon dams) and then a wide variety of parts and even airplanes. A lot of jobs are created along the way. It’s not just energy for Brazil, it’s an array of resources including open land – and making good use of them. Environmentalists, naturally, may disagree with the last part.

As for the temp economy, I haven’t written on that in a while, and I am thinking about it as you suggested before. There is more that can be said about this transformation and how to make it work – because I think it’s permanent.

Pingback: Coffee & Tea | Barataria - The work of Erik Hare

Its not like the whole world is anywhere near equal yet, so if the trends don’t continue there will always be a rich world and a poor one. If the goal is ending inequality we have a long way to go no matter how the last 20 years went.

Yes, the world will not be “equal” any time soon. But there are a lot fewer people in poverty, which is a good thing.

You make it sound like investing is all about trends. Well, it sure is if you follow the herd & you’ll never get ahead doing that. What should a contrarian do? That would be more interesting. What do you say, Mr. Sunshine? 🙂

I don’t think you have to be a contrarian to think the N11 idea is a lot of hooey. I think there will be far better investment ideas here in the US, but most will be small. There have to be companies that will make use of a lot of new technologies (not ‘net based) which will be better value and much easier to keep track of than, say, Iran. Yeesh.

Pingback: Government 101 | Barataria - The work of Erik Hare

Pingback: 5 years After Lehman | Barataria - The work of Erik Hare

Pingback: Triple Threat | Barataria - The work of Erik Hare

Pingback: Dia de la Raza | Barataria - The work of Erik Hare

Pingback: Three Million Reads, One Purpose | Barataria - The work of Erik Hare

Pingback: Resurrection | Barataria - The work of Erik Hare

Pingback: Stability | Barataria - The work of Erik Hare

Pingback: A New Cold War? | Barataria - The work of Erik Hare

Pingback: A Tale of Two Worlds | Barataria - The work of Erik Hare