The news whacked Wall Street and set off a slide of 1.4%. WalMart, the biggest retailer, reported slow growth and earnings below expectations for the second quarter. “The retail environment remains challenging in the U.S. and our international markets, as customers are cautious in their spending,” according to Chief Financial Officer Charles Holley. Should we be worried about it?

Probably not. While a turnaround consumer spending would be the quickest and easiest way to goose the economy and put people back to work, it shouldn’t come at the expense of fundamentals such as repairing household finances. A little caution now could make for a stronger economy in the long run – and that picture is continuing to look a bit brighter.

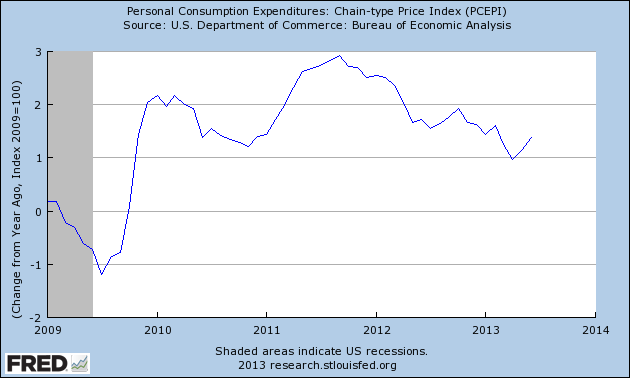

The details on WalMart are not as awful as the slide in the DJIA would suggest. Revenue was up 2.4% but same-store sales were flat, meaning that people are not really spending more. We can see that in this graph of year over year change in consumer spending adjusted for inflation from our old friends at the St Louis Federal Reserve:

YoY change in comsumer spending, less inflation

Inflation adjusted spending is rising at just 1.5%, down from the recent peak in 2011 near 3%. The trend appears to be running downward, suggesting that consumers are more than just cautious – they are actively trimming their expenses. If you’re in retail it certainly looks like bad news, and should be taken as such. But how bad is it?

The San Francisco Fed released their forecast for the rest of the year, and they predict economic growth to pick up from the surprisingly strong 2.3% recorded in the same quarter. The rest of the year should see us edging towards 3% gains, which would be healthy enough to see a good pickup in employment. But it’s not showing up in consumer spending – despite a decent uptick in consumer sentiment as noted here earlier.

Where is the money going? The average household in the US has a lot of debt to pay down and very little in savings. Improvements in those areas as unemployment gradually edges down may not make for a robust recovery now, but people are still cautious. The payoff will come much later, as we have been predicting in Barataria. It’s a matter of literally getting our houses in order first.

The trend may well be our friend

There is a lot more to it than that, of course. 1.5% growth in consumer spending isn’t much, but it’s better than the flat performance WalMart is seeing in their same stores. After inflation, they are pretty much treading water like so many of us. That means that WalMart’s share of US retail is not growing any longer, which can be taken as good news by many of us. There is additional room for small retailers and perhaps even craftspeople to take up the slack that is developing.

This should be taken as good news overall. That’s not a political slam to WalMart, but a statement of reality. Local businesses reinvest in local economies, meaning that the money that’s out in the US beyond Wall Street has a good chance of staying out there. The concentration of wealth that has marked the last several decades could be slowing. That can only be a good sign for the economy in the long haul.

It’s easy for those who own stock in WalMart to lament the situation, and they probably should. Part of the economic restructuring that is slowly taking place may indeed involve a return to cautious spending and less interest in mass produced consumer goods. That is consistent with an aging population with an awful lot of Baby Boomers looking towards retirement in the next decade. Slower spending combined with the prediction of relatively low inflation is a trend that we can expect to continue for a very long time.

No one actually likes long lines

So what is WalMart going to have to do about it? I don’t know and I don’t care. The age of the big box as an engine of growth is probably well over now. They are not necessarily a good indicator of the future of retail as the economy starts to change over – even if economic growth starts to pick up. They may still cause Wall Street to swoon over one less than stellar quarterly report, but it is still not the story that is worth following.

The restructuring is continuing, and it looks like it is moving away from WalMart. That can reasonably be taken as a good thing. Let’s cheer it on.

I read this report briefly on the WSJ (I think) their take was more sales we’re migrating to amazon. Our family is going to make a $400 purchase soon I’d prefer costco and best buy but we still haven’t splurged yet.

Amazon is the only online-only outlet to make it this far, and they are having problems, too. http://www.nytimes.com/2013/07/26/technology/amazon-reports-a-small-loss.html?_r=0 They are seeing growth, however, so you do have a point.

Wal-Mart is a cancer. Buying local returns money to the community that needs it. There may be things that are cheaper at Wal-Mart but there is no excuse for grocery shopping there. There is better produce made locally and it is usually cheaper.

Amen to all that. I didn’t want to get into the problems with WalMart as a destroyer of wages because I’ve talked about that before and it seemed like a diversion. But the mistake I think we can make that I’m dealing with here is that an uptick in consumer spending is not likely soon, but this is not necessarily a bad thing. Again, we have to wait 4-5 years before this is over, and that is playing out even with relatively good news.

We can only hope that the era of WalMart is over. Until they pay their workers a living wage they are nothing more than a cancer, as Annalise said. If that is the cost of cheap consumer goods and a consumer economy then it is just not worth it, not one bit.

Buying local is more than just a consumer movement, it is a moral movement. We don’t need WalMart and we don’t need a consumer economy.

We do need a “consumer economy” of a sort if we are going to have a stable middle class society. I think you put it better below. 🙂 What kind of consumer economy are we going to have? It is changing, and I would say for the better in the sense that it appears to be a more sustainable one that is developing.

I see little wrong with a consumer led economy esp. if it is spent on the “correct” things. You could concievably say that the affordable health care act is a consumer led economy as formerly marginalized groups most notably the working poor will have better access to care. Going without care especially in the early stages of a disease is very damaging. But Dale I do also agree with you its the choices that matter. One of my son’s friends is going to buy a large Chevrolet pickup truck. I have tried to convince him to think smaller perhaps a Scion B box or even a minivan as the cost of ownership would be lower. I have failed.

Another question that perhaps Erik or our readers could answer is where are people buying their clothes. Some people are not happy with the quality of low end retail, but the middle i.e. JC Penney is being abandoned. Personally I just bought a pair of marked down Carhart shorts at Fleet Farm along with high quality sports sandals (close out) at a sporting goods store. One more thing Farmer’s markets are not as accessible as we might wished them to be. I used to work downtown Mpls so it was always available there as some asian markets were available in the midway. But lately I had to pay higher prices at a co-op for carrots and tomatoes. I’ve even used the internet to locate markets but they do not mesh with my work and leisure. At least Aldi’s has organic spring mix at a good price ($2 to 2.50 per five oz.).

Amen to the first paragraph, but keep trying to convince the kids that they shouldn’t put it all into one thing like a truck!

On the second part – I met an apparel engineer who works for Target and is probably right now in Hong Kong working out a deal to buy clothes for them. She said that she can see a lot of apparel manufacture coming home to the US in the near future because it is finally being automated and the need for quick turn-around means the supply chain has to be shortened. Dealing with far-flung nations is a big expense that has to be weighed against the cost of production, and if we can make it all here despite relatively high wages it will all make much more sense. Perhaps not everything at once, but higher ticket items can move here first – the fashion stuff.

How is that for an item to keep in mind? I take it as an expert opinion.

Apparently the Gap which includes old navy is a huge retailer.

I think I might start watching retailers. It’s just not my thing, since I have no sense of fashion at all, but this may be the thing that has to turn around next, especially if young people start finding jobs this year as I have predicted.

I haven’t made too much of it yet, since it bounces around so much, but the gap between 20-24 year old unemployment and overall employment fell again in July to 5.2% (12.6% vs 7.4% overall). That’s down quite a bit from the 5.9% at the start of the year and remains my key indicator to watch if we’re really making progress in jobs. But that means an awful lot more to clothing outlets that deal in fashion for young people like Gap, etc.

I wouldn’t worry about WalMart, if you don’t like it don’t shop there. You make it sound like their business model is in trouble and that is the way retail works. Nothing stays on top forever. Look at Sears, they were the gold standard for all retail for a long time and now they are struggling to survive. It would be good if retail paid better, sure, but it never has.

I have been thinking about this. Retail is more automated all the time, just look at Amazon which you mentioned. WalMart doesn’t even need people on the floor to watch for theft because there are security cameras watching everything. There is no reason we can’t have a minimum standard for pay that is more like a living wage. The minimum wage should be raised to $10 an hour and maybe more. If everyone has the same cost rise it will all come out in the end.

Good line of reasoning for both of you, IMHO! Retail is just awful, no doubt about it. But if everyone had the same jack up in costs it would probably encourage more automation (you left out automated and self-serve check out, one of my faves!)

The Fed’s projections of 2-3% GDP growth have been greatly exaggerated. GDP growth is driven by 2 MAIN factors: demand, and money movement. If you look at the M2 Velocity, money isn’t moving from bank vaults. And if you look at the PCE minus food and energy (as a measure of demand), you’re going to see almost no movement there either. I’ll be shocked to see more than a 1.7% GDP growth, especially in a labor-rent environment (low wage) that does not allow for the expansion of demand.

The Fed was off on growth earlier this year, but it did pick up in 2Q13. They are basically saying that trend will continue, which is a decent bet for nearly any trend. Your point about velocity is a very good one – it keeps crashing as the money supply increases and GDP doesn’t move much.

Here are some key places that we’ve talked about velocity, particularly with respect to the low-end where velocity is clearly much higher but cash is in short supply. I prefer to use MZ for the money supply since it is so broad, and correspondingly MZM. I figure we’ll see a change there first.

But yes, it seems unreasonable to see an expansion in consumer demand until the employment picture is at least improving at a decent clip, if not much closer to full employment. That is what we have been really focusing on for 2013 as the key indicators, as we’ve noted before in Barataria. That consumer spending is not coming around does not bother me much yet, given that, but the apparent drop in YoY change since 2011 is a bit disconcerting. It seems to be worth watching.

You make a great point about MZM over M2, since the Fed is only paying 0.25% on reserves. Since service industries make up some 30% of GDP, that means that there has to be consumers with money to consume the services. I agree that consumer spending isn’t a great issue with regards to GDP. If PCE in a consumer market can’t raise GDP, then maybe manufacturing can. However, that’s going to require an additional $12 Billion (my math is approximate) in new orders before the end of the year in order to show at least a 2% GDP growth. But hey! You never know! Weirder things have happened; like the multitude of things that’s redefining both Economic and Sociological Theory by the minute.

My schtick is Political Economy type Sociology; so I’m always concerned about unemployment and consumption in this service-based environment. Consumption changes people’s perceptions of their socioeconomic status, and will give a better “pulse” to social sentiment toward the economy.

My prediction by the end of the year, a 1.5% GDP growth with not much movement in U6, and a -2% change in disposable income. Also, keep an eye on Temp Employment – I predict a sizable movement there by the end of the year – beyond their norm.

Great insights though, and makes me re-think the way I run data!

We’re on the same page here. My bias was to never look at retail, which may have been a mistake, but I also stopped looking at manufacturing too closely because I can’t see it going anywhere as long as the Dollar is strong. But the loss of 1/3 of our manufacturing jobs since 2000 (down 6M from 18M, roughly) very much describes how we got into what I call the “Managed Depression”. It is hard to imagine us getting out of this without replacing those jobs.

This is at the heart of why I talk about a “restructuring’ rather than a “recovery”. The economy is going to have to change in ways we really don’t have our fingers on yet before we get out of this. The new economy will contain an area of growth none of us are really thinking about today and when fully-fledged in the 2020s will look like something we wouldn’t recognize today, I’d say. It’s my best guess.

But some manufacturing component probably fits into this, or at least I hope it does, given the importance of manufacturing jobs for young people to get into. This is part of why I’m watching the 20-24 year old unemployment rate – the more important part being that employers will hire people with less experience once they really have confidence in the future.

OK, I’m rambling. I think GDP growth will be higher, but still not stellar. Now that we’re seeing hiring by big companies the job market will improve – but your point that U6 won’t budge because it’ll be through temps on part time gigs (or that’s how I read it) is an important one. That is a good call, IMHO, and U6 probably won’t improve much this year. I think you’re just a little pessimistic, but people call me Mr. Sunshine for being too rosy. It beats being called Dr. Doom as I was back in 2007-2009. 🙂