We’ve discussed many times before how the Federal Reserve sets the interest rates for everything from used car loans to mortgages to savings accounts across the US. The task has always fallen to the Federal Reserve Open Market Committee (FOMC) and its “Fed Funds Rate”. As far as anyone can tell they perform a calculation based on the prevailing conditions as to what the optimal rate should be. They balance out the need for more jobs (favored by cheap money, or low rates) with a desire to keep inflation in check (with high rates) and a rate is published. From that baseline for the cost of no-risk money a premium is added by a bank based on the risk (low for a mortgage, high for a used car) or subtracted (the value of savings) and all is good.

Except for one small detail – that mechanism has been horribly broken since 2008 when every calculation suggested the optimal rate was below zero. As long as rates are near zero and there’s a flood of cash in the financial world (not that you are getting any) we have what’s known as a “liquidity trap”. And the way interest rates are going to be set in the near future is going to turn on some far more obscure things such as the “Reverse Repo Rate”.

Yes, it’s complicated.

The headquarters of the Federal Reserve. Imposing, yes?

The problem with the traditional mechanism is simply that big banks are not interested in borrowing from the Federal Reserve at the moment. The Fed is supposed to be a central bank, which is to say that big institution where other banks get the money they need to make loans. The problem is that in a risk-adverse world where there is a tremendous amount of money sitting in the hands of big banks no one needs to borrow from the Fed.

Instead, the Fed has become a place to park money that has no place else to go. It could go out into the world to make low interest loans to small businesses that hire people and promote growth, but no one wants to do that. Such a loan has risk written all over it, which is to say that there’s a good chance it’ll never be repaid.

The first goal when you have a lot of money is called “capital preservation” – you don’t want to lose it.

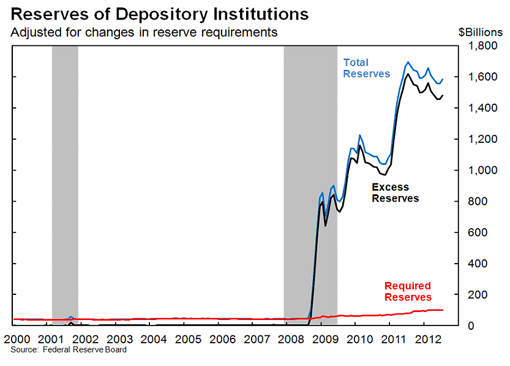

Deposits by banks alone total $1.8T now, far exceeding what they are required to maintain.

Deposits at the Federal Reserve have soared recently – from $25B in 2006 to about $3,000B today (3 trillion dollars). The interest paid is a measly 0.25%, but that money is at least safe. As discussed before, some central banks such as in Switzerland are paying negative interest – you have to pay them for the privilege of parking your money.

If that seems bizarro to you, you aren’t alone. But there’s a lot more to it than that.

The money on deposit has started to be dominate the financial world, and the interest rate paid on it now sets the standard for the cost of money. Why would you loan money out at less than the rate given for a sure thing when you are incurring some risk it will never be paid back? It’s a powerful force, one that is eclipsing the rate set by the FOMC.

As noted by Fed Vice Chair Stanley Fischer, this is the new method for determining the market rates throughout the US. The only thing it needed was to be goosed a bit to completely dominate. Interestingly, that’s what the Fed is doing.

Repo men are always intense. But that has nothing to do with this repo rate.

As if the $3 trillion is not enough, the Fed is encouraging many large institutions to park money “overnight” at by loaning them some of the $4.5T in government bonds that they own in exchange for hard cash. This is then paid interest at what’s called the “Reverse Repo Rate”, named after this kind of swap. It’s set separately from the interest rate on deposits, but is currently the same 0.25%.

According to Fischer, “The reverse repo counterparties (eligible institutions) include 106 money market funds, 22 broker‐dealers, 24 depository institutions, and 12 government‐sponsored enterprises, including several Federal Home Loan Banks, Fannie Mae, Freddie Mac, and Farmer Mac.” In other words, it dominates consumer lending like nothing ever has before.

The rate set for this is the new standard for lending everywhere. It comes from the simple fact that large institutions are not borrowing money from the Fed but are in fact depositing large sums in it – and are being encouraged to park even more all the time.

Not everyone can do this.

This has the net effect of taking money out of the system, but more importantly it means that the Federal Reserve is effectively losing control of banking as we know it. Money does not come from the central bank – it comes from the market. The status of the Fed as the most perfectly safe institution available for capital preservation is its one great asset now.

What does this mean for policy? At some point, large banks will become less risk adverse and be willing to start lending money. It’s likely to be inflationary as the growth in the economy will not come from a calculation that balances the need for growth in the real economy against the growth of the money supply. But the Fed can control how much money goes out into the world by adjusting how much it is paid for deposits, putting the brakes on overheated inflation by adjusting the rate up.

However, we’ve moved from a world where the Fed is a net charger of interest to one where the Fed is a net payer of interest. And that means that a certain amount of stimulus is going to be with us forever – or at least until this balance is cleared.

In the end, the traditional way that interest rates on everything are set has changed, possibly forever. How exactly this plays out once we are past the liquidity trap and into a more normal financing world is unknown. But we know that, at least for now, the way growth is balanced against inflation has changed.

A much appreciated article.

Read over several times (high interest!).

I recall an axiom from Drucker that an established business suddenly awash in profit is actually getting a warning of great change coming (I think he was discussing the 70’s).

That is all I can grasp from “experience”.

I know you are watching something else, Captain Ahab.

I am indeed looking for changes in public policy that are necessary to reverse this trend. I find it very disturbing, especially when you realize there is no quick way out of this. Even at just 1% the interest on $3T is $30B every year!

This is very scary but I don’t know why. Perhaps more elaboration is in order. Are you saying that the Fed has limited ability to set rates now?

Yes, the Fed is in a corner. They have limited ability to influence anything real as long as they are trapped near zero rates. Those deposits have to go out into the economy before they will have the freedom to set rates they used to enjoy.

So the big banks have us by the nose now?

Pretty much, yes. The private banks are now running the show because they have the resources.

There is definitely more to say on this topic. If the Federal Reserve can’t set rates for borrowing then who can? Who has all this money on deposit with them? How will they set the rates?

That is exactly the problem. If you think it through for a while it gets scarier all the time.

Yeah the near zero interest rates supporting the liquidity trap are quite scary. Although it’s not called a trap for no reason; the Fed will be hard pressed to escape the current set of policies. Every press release pushes back the timeline for normalizing interest rates. Sustaining this could be really problematic.

Exactly. We have to see that $3T out into the economy before we can say things are “normal”. And that means that with all the risk in the world investors have to believe they will get a better return investing than they will parking it in the Fed.

To me, this only puts more pressure on the need for major policy/tax reform. We have to do something to shake things up and tell the world “It’s different from today forward”. I hope to tackle that on Friday once I get my head around it some more.

Pingback: Sitting on Cash | Barataria - The work of Erik Hare

Pingback: Betting on Low Interest | Barataria - The work of Erik Hare

Pingback: Bad Weather Ahead? | Barataria - The work of Erik Hare