If you’re like most people living paycheck to paycheck, you have a simple problem at the end of the month – not enough cash. There’s nothing to be embarrassed about here – it’s a common problem that is faced by a large number of families as the economic recovery struggles on.

But if you’re an S&P 500 company, you may have a different problem – too much cash. Not precisely too much cash on hand, that is, since that’s never a problem. You may have something like cash sitting around somewhere in the world that you have trouble bringing home to make use of the way you want to.

Therein lies the problem with this economy – not that there isn’t enough to go around, but that it isn’t going around.

Not everyone can do this.

The amount of cash on hand held by non-financial US corporations has been discussed by many people for a long time. It’s fueled by many things, but the main problem remains that companies do not feel that they have something in hand that is worth turning that cash into an investment. The money is being hoarded and not released onto the world at large.

We discussed this previously with respect to the large financial institutions that have been allowed to deposit their money with the Federal Reserve and how that has turned everything upside down. The problem, however, is much larger than that.

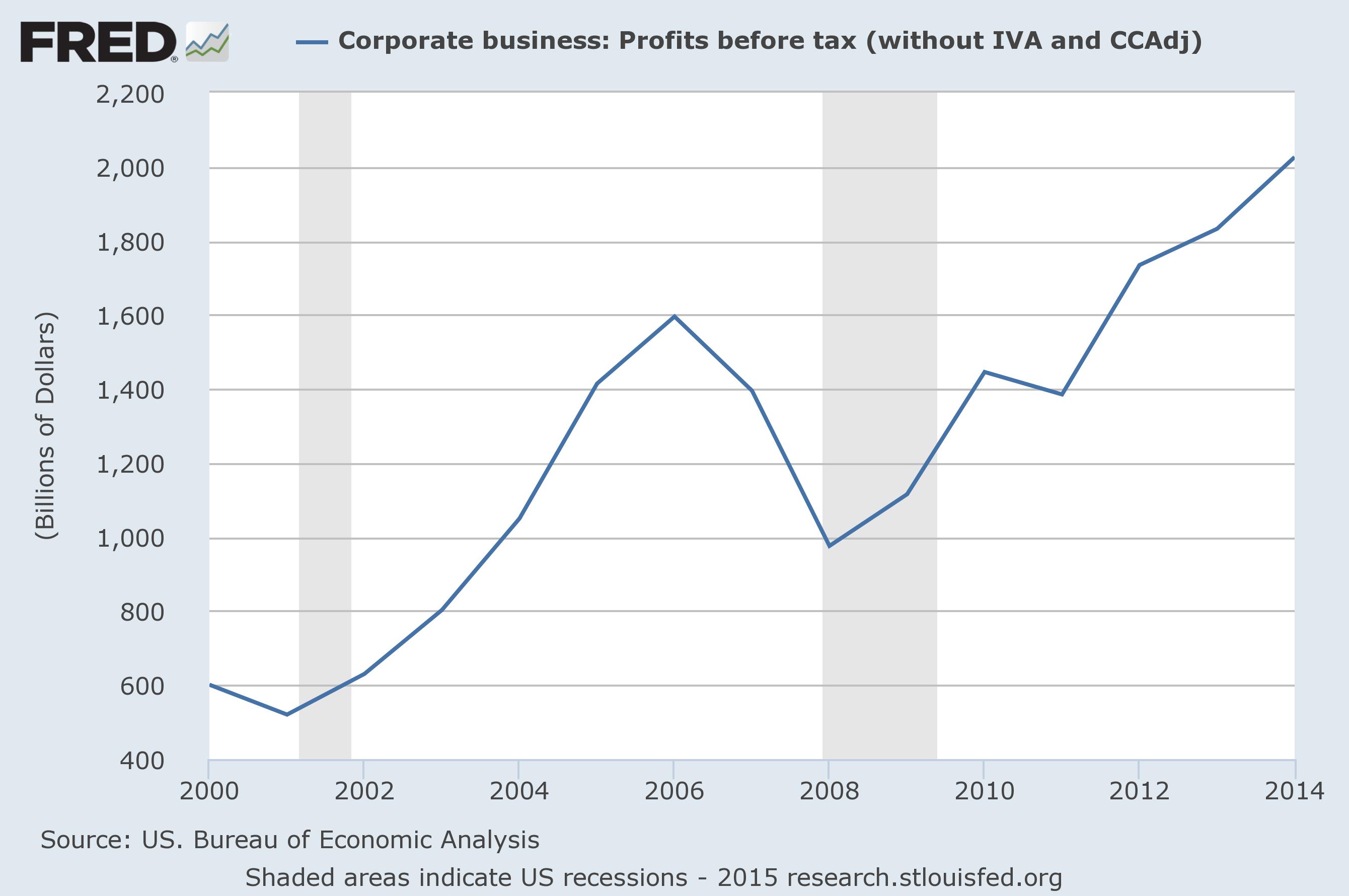

We have to first start with corporate profits, or where the cash comes from. They are up 25% overall since 2006, the last really good year before the last official recession:

Those profits are, in normal times, re-invested in either the company’s main operations or in some kind of expansion into another field that is expected to be more profitable than the company itself. We have discussed this problem before here as well – companies are not confident enough to re-invest in themselves and their own expansion. Thus the recovery is slow.

But what’s happening is even worse than that. Companies have no confidence in anything and are sitting on their cash as idle money. US corporate cash holdings in non-financial companies are approaching $2T. The trend is hardly a new one, either, having started as early as 1990 during the last solid economic boom. There was a time when some of the excess profits went into real estate holdings and the like, the root of the bubble, but even that has stopped lately.

But what’s happening is even worse than that. Companies have no confidence in anything and are sitting on their cash as idle money. US corporate cash holdings in non-financial companies are approaching $2T. The trend is hardly a new one, either, having started as early as 1990 during the last solid economic boom. There was a time when some of the excess profits went into real estate holdings and the like, the root of the bubble, but even that has stopped lately.

This is what is so dangerous about the “liquidity trap” formed by very low interest rates and very high savings. It is impossible for the Federal Reserve, or anyone, to inject money into the economy to get things rolling because we are already awash with far more than we need – at least at the large corporation level. There are several good guesses as to why this is happening:

The search is it’s own reward, but you re-search to find the $$$.

Research is expensive and requires a stable company: As we move to a higher tech economy, the need for more long-term research requires a larger pool of cash on hand to weather any storm. This is the main force credited with the change around 1990 in a paper by the St Louis Federal Reserve. It is definitely true that high R&D expenses carry with them a lot of risk, making the rest of the company’s operations necessarily more risk adverse to balance it out. Self insurance of a kind is also critical when carrying that kind of risk, too.

Globalism and high tax rates: Another cause cited in the same paper is that much of the cash is overseas and thus away from US corporate taxes. Repatriating them to the US in some form would make them taxable at the marginal rate of 35%, the highest in the world. GE recently announced that they would pay a dividend and buy back stock by repatriating $90B from abroad – triggering a staggering $4B tax bill. Reading the tea leaves properly you can see why the need to flash their cash around at such a high cost is hardly a sign of any confidence in the operations of GE.

Money is plain cheap: Another reason is that with debt as cheap as it is capital expenses can be paid for with cheap bonds now while holding onto cash and increasing the company’s overall assets. This may not make sense on the face of it, but increasing debt is another trend in the same companies. The theory is that money is so cheap you might as well borrow as much as you can now and expand your credit, even as you build up cash at the same time.

Yikes!

No matter what, there is little doubt that a general rise in interest rates will hardly choke off large corporations which are now immune to money markets. The solution for the US economy may well be to lower corporate tax rates, at least at the margin, or at least make it harder to shield money overseas. But the trend to higher cash has been growing for a long time and will not go away soon.

The growing pile of corporate cash is a sign that the economy remains out of balance in some fundamental way. It’s worth watching along with the total corporate profits. Both will probably turn down when there is a genuine change in the economy. This may sound illogical, but when companies start re-investing in themselves they will draw down their reserves and increase their expenses. That is the trend we can expect to see sometime by 2017 if there is going to be a new economy and a genuine new bull market.

A few thoughts…there has been something bothering me ever since I read the story about GE bringing back money from overseas. Here, you say they are repatriating $90B and paying a “staggering” $4B tax bill. A story I read was $36 billion being brought back and paying $6 billion in tax. The numbers aren’t as important to me as the way the numbers are presented. Virtually every reporter writing a story on this has used language that makes the tax bill sound extreme and shocking, but never mentioning that GE still gets A SHIT-TON OF MONEY AFTER THE TAXES ARE PAID. If the bill is so shocking, the amount they get to keep is obscene. The other issue everyone brings up is the 35% tax rate; however, whatever the number is, either $6B on $36B or $4B on $90B, that is no where near a 35% tax rate. Sorry…the high tax rate story is crap. Let’s say the GE tax bill is $4 billion. The governor of North Carolina recently sent a bond proposal to the state legislature that he is hoping to get approved and in front of voters this Fall. It is for $2.8 billion to pay for badly needed upgrades to North Carolina roads and to pay for desperately needed new buildings across the many campuses of the UNC system. If the GE tax bill is $4 billion, ONE COMPANY’S tax bill could pay for all that..and then hell, why not tack on the $700 million that has been cut from the UNC system and you STILL haven’t used all the money from one company’s tax bill. Throw that tax money at North Carolina, and it would create thousands and thousands of jobs and, if giving it to universities, result in tons of research and development. Money would flow into the economy, people would spend it, it would get taxed and bring revenues back into the government, and it would result in a ton of infrastructure and R&D that could benefit GE! Instead, we have to ask individual North Carolina citizens to come up with the money over the next decade. Again, this is one company. What could we do if all the other companies that are hoarding cash overseas would repatriate it and pay taxes. It seems to me so much could be accomplished and the companies could still keep obscene amounts of cash. Why aren’t reporters doing some contextualizing on what this money really means rather than throwing around biased words like “staggering” which really reflects our internal bias against paying taxes. Taxes are not bad….we need to stop talking like that.

I won’t argue that my bias didn’t come out in that. But it wasn’t so much that I am personally against them paying taxes, it was that I was assuming that they wouldn’t pay that much unless they were forced to.

In this case, the blatant attempt to puff their stock came at a rather steep price. I find it shocking that they were willing to do pay out so much in taxes. That doesn’t mean I’m against making corporations pay more. But the way we do it with a high marginal rate is hurting our collections because so much can be hidden overseas.

It was an unfortunate choice of words all around. It could have been done much better.

Good point. I think part of this has to do with manufacturing being held outside the US and companies having more faith in manufacturing. Also as you mentioned it makes for easier spending due to corporate taxes. This probably has to do with the need to build infrastructure for production outside the US. Regardless, your articles really highlights that economic activity is disproportionately shifting outside the US.

The investment is certainly overseas, even as the income is from here. The economy is turning around, slowly, but the net investment in America is very slight. I believe this is worth looking at very carefully. I would start with the overhead per employee, which I’ve been harping on for years, and work out from there. Wholesale reform is obviously necessary, IMHO. I also don’t see a liberal or conservative approach as being appropriate – this will take a deeper understanding of how corporations have changed and how we need them to change in the next economy.

If rates go up, won’t that cash appear more valuable as an investment of some kind? Seems to me just about anything that gets it out into the economy would be a benefit. So maybe the secret is to raise interest rates?

Maybe. If rates go up, the interest on cash goes up, too. So rates have to remain abnormally low to favor investment in something that is not passive. That’s the nature of the liquidity trap – it’s very hard to get out of.

What will change things is when income from investments in job and growth producing things outweighs that passive income. Getting there is the hard part.

When all that money gets out there will be inflation, mark my words. Growth is good but we cannot grow into all of this overnight. There will come a day when we long for it sitting around as idle cash.

It depends how fast it goes out, but that does seem likely at some stage, yes.

It is true that with some creative accounting you can expand your apparent net worth by holding cash and using debt instead. This makes perfect sense as a reason for a large increase in net cash on hand when interest rates are historically low.

I appreciate the expert opinion! 🙂 Thanks!

Unfortunately, this is a repeating cycle with many companies. Some have it right in certain aspects, where others strive in areas that others lack. Part of the core solution could follow as this:

1. Lean Six Sigma. More companies are relying on things such as this to cut excess waste and to “streamline” the process. Unfortunately, this creates an environment where people ask the question “Am I part of this waste?”

2. Improve employee morale. One of the perks of the company I work for is that all profits are split among employees multiple times a year. There is a little set aside for expansion, but in the end it’s the employee that gets the real benefit. Companies like Chick-Fil-A practice both of these to great lengths, and it has turned into a high quality product with a pleasurable experience for the customer.

Excellent comment – this could be expanded to a post by itself!

I think you hit the nail on the head, especially with the cyclical nature of this. In the 1980s, a company with a lot of cash was a takeover target more than anything. It was dangerous to have too much cash on hand. Perhaps those predators need to come out again? 🙂

With regard to running a company, I can’t agree more. Insisting on the highest standards from employees and giving them real authority to improve things is at the heart of Six Sigma. That has to be combined with a great work environment that includes good compensation. That is how you run a company that provides good service and quality, which is to say a company with a decent and sustainable profit margin.

Pingback: Productivity Panic! | Barataria - The work of Erik Hare

Pingback: Betting on Low Interest | Barataria - The work of Erik Hare

Pingback: Catching Up on Old Stories | Barataria - The work of Erik Hare

Reblogged this on Today's Economy and commented:

This article relates to my blog entry about corporate inversion. Bringing cash into the country has so many barriers that companies are simply letting it sit. An infusion of corporate cash in the economy may cause some issues but far fewer than keeping the cash in a vault. America has a right to provide a disincentive to keeping cash overseas, it undermines the tax structure and removes it from circulation; but it has to realize that people are doing it anyways and getting that money back would benefit everyone. It’s an interesting policy del are that has been ongoing for years, it’ll be interesting to see what happens.

Pingback: Fear Doesn’t Glitter | Barataria - The work of Erik Hare

Pingback: Drama Over Yet? | Barataria - The work of Erik Hare

Pingback: Careful What You Wish For | Barataria - The work of Erik Hare

Pingback: Forcing Investment | Barataria - The work of Erik Hare