The stock market has rallied for two days, with the S&P500 back at 1987 from its low of 1869. It’s still down 6.8% from its peak of 2130, set in May, (and nearly matched just a month ago) and down 3.5% for the year. It’s almost like the crash never happened, right?

Well, no. But there is a lot of good news for the underlying economy, some of which came in this week. The really good news is still out into next year, which is essentially forever to this market. We have to get over an interest rate hike, which will definitely come this year no matter what you read elsewhere, and a lot of jitters.

Bad stock news requires a picture like this. Apparently, these traders still exist.

Let’s start with the bad news, since that’s how the week started. The convulsions out of China are starting to be ignored by other stock markets around the world, but they are far from over. Before this is done we can reasonably expect the Chinese Central Bank to lower interest rates further, currently at 4.6%. This will weaken their currency and continue to spook markets just as it did last week.

There is still the question of corporate profits, which are relatively low – down from an all-time peak set just two years ago, a ridiculous standard. But the overall price to earnings ratio (PE) of the S&P500 is still at 20, which is hardly the signal for the start of a bull market.

Lastly, investors are still nervous after all this. The Volatility Index (VIX) remains high after bouncing off a “Hang on to your guts” 42 on August 24th. At 26, it implies there is a 66% chance the market will go up or down 26% in the next year. Popularly, it’s taken as a good measure of anxiety in the market.

The Volatility Index (VIX) for the last month. The spike is nasty, and hasn’t entirely retreated. From Yahoo! Finance.

There seem like a lot of reasons to stay out of the market, but the positives are huge. The first revision for Gross Domestic Product (GDP) for the second quarter of the year (2Q15) came in at a stunning 3.7%. That comes after William Dudley, President of the New York Fed, called a rate increase in September “less compelling”.

This is the plan, yes.

Strong growth and cheap money? Can it get better?

Oh, yes. If you leave out the part of the economy dedicated to exploring and drilling for oil, the net expansion in 2Q15 was a stunning 4.5%, the highest since 2006. More interestingly, the collapse in this field of 68% means that the bloodletting is already over and 3Q15 might indeed come in over 4% unmodified. This includes a strong growth in consumer spending, the last thing to revive at the end of this Depression, which grew 3.1% – the highest growth since 2008.

It’s worth noting that with 1Q15 only showing 0.7% growth, some of this may be a bad “seasonal adjustment” in the figures. But it still looks good no matter what.

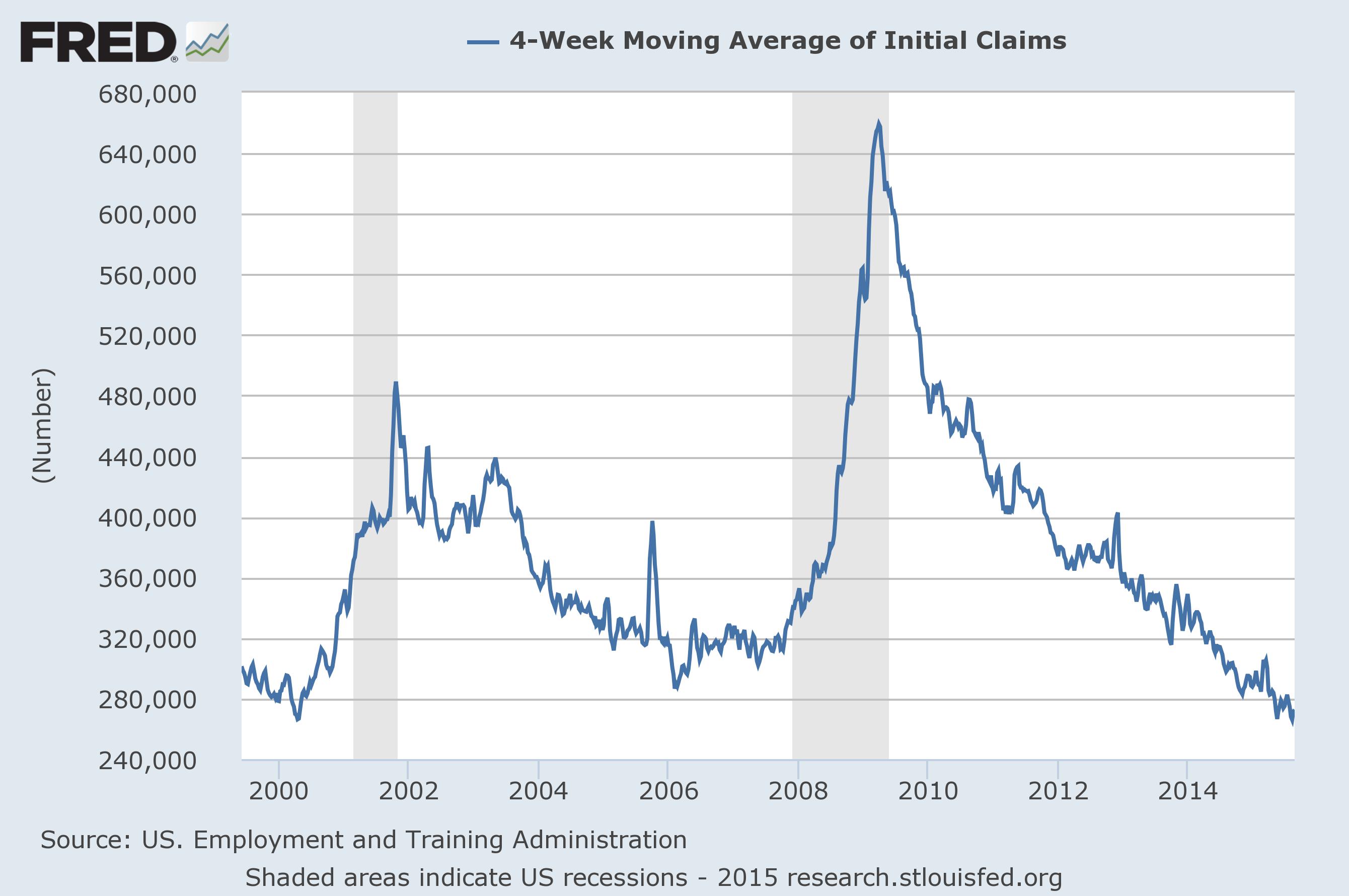

The good news extended to jobs, where new claims for unemployment insurance (Initial Claims) fell below where they were before the Depression started in 2000 at 266k (4 week average). That doesn’t mean that companies are hiring, but they are definitely not firing.

Initial Claims for Unemployment, a measure of how many people lost their job in the last week. Data from the St Louis Federal Reserve.

Indeed, business investment is up significantly in the GDP figures, 3.2%, which explains why corporate profits are down. That investment won’t pay off until at least some time in 2016, but the investments are being made.

Strong capital investment today looks like a net negative on Wall Street. But the benefits come later.

On top of all this, now that the dust has settled we can see where things stand around the world in currency exchange. The US Dollar will today only buy you €0.89, down from its peak of €0.95 last April. It’s still a lot stronger than last year’s €0.77, but our goods are not as expensive as they were – and the rise has certainly stopped.

How good is the leading economic news? Even the worst threat of all, an interest rate rise, has a strong potential of turning into a net drop as interest rates around the world start to harmonize a bit.

It’s still hard to see the stock market suddenly getting its resolve and pushing back to where we were just a month ago even with all this good news. After all, the best news looks good years out and the stock market has become notoriously short sighted, hardly an indicator of anything in the future.

Still, most in the US have their retirements invested in this nonsense and over the very long haul it does have to reflect at least something in the underlying economy. Now that the drama appears to be over it’s best to ignore the daily bumps and feel confident that something good may indeed be coming.

I heard a whisper in the wind- “It’s a rigged deal.”

At least part of it is. As long as they have the dough to cram into it, they won’t let it fall too much. In 2008 they ran out of options to be able to rig it.

Why does this feel so reminiscent of the 80’s and all those fears of the Japanese taking over the World’s economy and buying up America, only to later have their economy implode? The idea of Japanese hegemony back then was so ominous, that by the start of the 90’s suspense movies like “Rising Sun” were being made about it. I suspect that Gary Bertnik is on to something and that perhaps we’re seeing yet another swindle of great magnitude, that’s been perpetrated against yet another “rising star” in the strange saga of Global Economics.

YES!

I have never been one to fear China too much for exactly this reason. This will end in a similar way, too, when Chinese money comes to the US in search of a safe haven. Remember when Japan was buying real estate here, including Rockefeller Plaza? Caused quite a stir.

The truth is probably not entirely sinister, I believe. Things are just evening out around the world and the process is messy. China has a rightful place in world leadership and assuming that is going to take a lot of ups and downs. We’re about to see the limits of their centrally planned economy, IMHO.

I vote that its rigged too. Maybe it does reflect the economy eventually but only a fool tries to trade stocks against these guys. Have you read Bill Fleckenstein lately? He says that the programed trading is going to cause a major crash.

I love Fleck! He’s kind of a perma-bear, always finding a reason for a crash, but as a short that’s his biz. I saw some stuff maligning shorts again, as happens in every crash, but who else will keep the market honest?

I know, no one can. But hey.

I don’t see a crash from them, but I do see a major war between the programmed traders. They can be manipulated, too.

Is it just me or is all news taken as bad now? Financial people seem to be in a fowl mood. That is probably all that matters.

A very good point. I think there is a lot of good news, but it all seems to dissolve into worry and panic. What will it take to reverse that? Dunno. But bears do seem to rule the financial media right now.

Put your money away and forget about it. What have the returns been for a SP500 index fund over the last 10 years? It may not be as great as the boom before but it has still been good. I always advise people to not pay attention to this stuff however. It goes up and then it goes down and it will just make you crazy.

Over the last 14 years we have averaged 4%. Adjusted for inflation it’s nearly zero, however. A shorter time frame from say 2009 looks much better, like a 17% return.

http://www.moneychimp.com/features/market_cagr.htm

Yes, it’s best to just forget the day to day fluctuations.

Pingback: Good News! It’s Good News. | Barataria - The work of Erik Hare