Are you ready for retirement? While the idea might have its appeal, especially with the winter weather making for long commutes this year, an awful lot of workers are not on a track to be able to retire. That’s according to a survey from the Employee Benefit Research Institute (EBRI), conducted annually. They found that only 18% are “very confident” that they’ll have enough for retirement and a further 37% are “somewhat confident”. That’s up from the 2013 survey, in which only 13% was “very confident”.

The implications go beyond any one family’s ability to retire, however. The decline in workforce participation has been largely due to retirement since the start of 2011, and retirement opens jobs for young people. The wave of retirement that should accelerate after 2017 is one of the main reasons Barataria has hope for the 2020s. But is retirement nothing more than a dream for many workers today?

Making plans?

The survey of 1,501 people, 1,000 workers and 501 retirees, has been performed annually since 1991. By interviewing both current workers and retirees, it contains a complete picture of both expectations of retirement and how retirement was eventually realized over a relatively long period. We can see a lot of where we fit today and how the changing economy influences decisions.

The most prominent feature of the survey this year is that confidence about retirement is a strong function of income, which also correlates with membership in a retirement plan (401k or related). The improvements in confidence over 2013 came almost entirely among people earning $75k per year or more,

The biggest problem? Debt. Fifty-eight percent of workers and 44 percent of retirees report having a problem with their level of debt. Furthermore, 24 percent of workers and 17 percent of retirees indicate that their current level of debt is higher than it was five years ago.

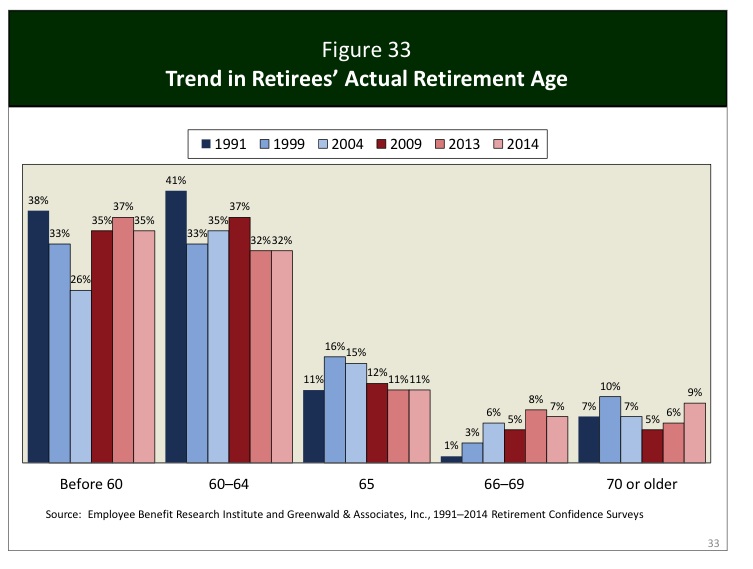

The question for macro-economics has always been whether the bad economy would force people to retire early because they could not find jobs or retire later because they did not have enough savings for retirement. The chart below shows the changes over the years:

Chart from the EBRI report

In 2004, 61% of all workers retired before they were 65, 15% right at 65, and the remaining 14% later. In 2014, that shifted to 67% early, 11% at 65, and 12% later. There may be a trend towards earlier retirement overall, but it seems to be shifting towards a binomial distribution, or a split between workers who can afford to go early and those who can’t afford to go at all. That may be a reflection of the growing income disparity as much as anything. That’s also shown in the general lack of confidence among those working who aren’t near the top.

Overall the median age at retirement is 63, meaning that if anything the projected retirement of Baby Boomers is going to accelerate even faster than we previously though. By 2020, those retiring will be the heart of the Baby Boom, born in 1957. Workers will be in short supply by then.

But the strain on public assistance will be a great concern if worker’s fears are realized. While 29% are very confident they will be able to pay for daily living expenses (43% somewhat confident), only 17% are very confident that they can pay medical expenses (29% somewhat confident). If workers are right, what will destroy their retirement are medical costs, which a majority figure they won’t be able to pay for on their own.

If these trends continue and today’s employees are right, the net retirement age won’t change much but the social burdens will be much higher. There will be opportunities for young people to enter the workforce and that should result in upward pressure on wages, but taxes are likely to increase to pay for medicare.

Overall, the conclusion is that while confidence in the ability to retire is improving overall, the effects of income inequality will be felt more strongly by those in their golden years. They won’t be as golden as many would like. But there is still reason to believe that the 2020s will be a good era for those looking for work as the retirement wave accelerates.

One of the problems with 401 K’s is that they claim they only have 1% fees which in reality is closer to a 25% fee. If your growth is 4% a 1% fee is 25%. Also some boomers are getting hit with high college costs. Within some families money trickles to where it is needed most right now. And there is great inequality between families. There are seniors who give money to juniors for housing, service for daycare etc. This is a hard thing to quantify altho I hope Nate Silver and 538 will approach this subject sometime. Sorry I haven’t written more I did like your article and link to Ukraine. 538 and the NYR of books have also had good articles on same subject. Also could you please write about the ACT test sometime. Am enjoying Danish police dramas like Broen and The Killing.

I hadn’t thought about the fees – I guess the banks are always the ones who get rich off anything.

I’ll think about the ACT – my daughter has some things to say about it, too. Many colleges don’t really worry about it too much anymore, which is interesting.

This is very interesting because I don’t know anyone who is saving enough for retirement. Maybe people closer to it than I am are doing more for it but I know I am behind. Having a 401(k) is one thing but actually adding to it is another. Not many employers contribute at a level that will help it grow without a substantial contribution from employees.

At least the stock market is rising so there is growth there.

The survey was about people’s opinions, so it didn’t get too far into how much they had saved – just whether it was “enough”.

Again I want to congratulate you on that great chart. I have been looking for a similar one for months. Many people are surprised at the number of classmates who are retired or will retire soon when they go to their 40th class reunion. Here’s an idea for another topic. The regulation (some say the over) of the housing industry and zoning. I am enjoying seeing a five story building in the Midway now and I know there is some controversy in the Victoria crossing Grand area.

Thanks. I have been wondering for a while what the retirement age is and how it’s changing, too!

Zoning is … one of those things. I honestly don’t know how I feel about it in the abstract. Some zoning seems obviously necessary, but it’s so easy to go overboard. But don’t property owners have some right to protect their value? I can go many ways at once with it.

I don’t know what I would say if someone asked me if I saved enough. Depends on how I want to live or have to live. I could make it but not as well as I am now. Quality of life is the issue.

Good point. I’ll bet many people retire before they think they are ready to.

On zoning I have been struck by the Danish polysci aspect of The Killing (Forbrydelsen) One candidate calling for 1000 new apartments and an end to immigrant ghettos and a move to section 8. I think Zoning is such a crucial issue now with looming enviro changes

Pingback: Smaller Government, Peaceful Government | Barataria - The work of Erik Hare

Pingback: Smaller Authorities, Peaceable Authorities | Posts

Pingback: Demographics is Still Destiny | Barataria - The work of Erik Hare

Pingback: A Smaller Government is a Peaceful Government | Barataria - The work of Erik Hare