Since 2008, the Federal Reserve has more or less printed over $3.2 Trillion in three rounds of “Quantitative Easing”, now tapering off to zero. Many have speculated that this has to result in inflation for the simple reason that there are more US Dollars out there than ever before. That’s based on the most fundamental principle of any market, supply and demand –more of these things called “Dollars” around and the value has to drop, meaning it takes more of them to make a reasonable exchange with something real.

It hasn’t worked out that way. Inflation remains less than 2% per year as it has since the financial crisis that started in 2007. How on earth can that be?

The answer is that the number of US Dollars in the world is only one part of the equation. The “velocity of money”, or the number of times they turn over in the economy, is equally important. Data since 2007 shows what every freelancer and job seeker knows – it’s a tough world out there, and people are pretty slow to let go of the dough they have.

Before we can talk about the “velocity” of money, we have to define what we mean by “money” and how much of it is out there. The broadest measure we have good data on these days is called MZM or “Money at Zero Maturity” – a measure of the bucks printed and in coin, plus all bank accounts and money market accounts. It’s not a complete measure, since it does not include stocks and other investments that people can both borrow against or otherwise use to make themselves feel rich. It’s “demand money”, the stuff that is accessible right now.

Before we can talk about the “velocity” of money, we have to define what we mean by “money” and how much of it is out there. The broadest measure we have good data on these days is called MZM or “Money at Zero Maturity” – a measure of the bucks printed and in coin, plus all bank accounts and money market accounts. It’s not a complete measure, since it does not include stocks and other investments that people can both borrow against or otherwise use to make themselves feel rich. It’s “demand money”, the stuff that is accessible right now.

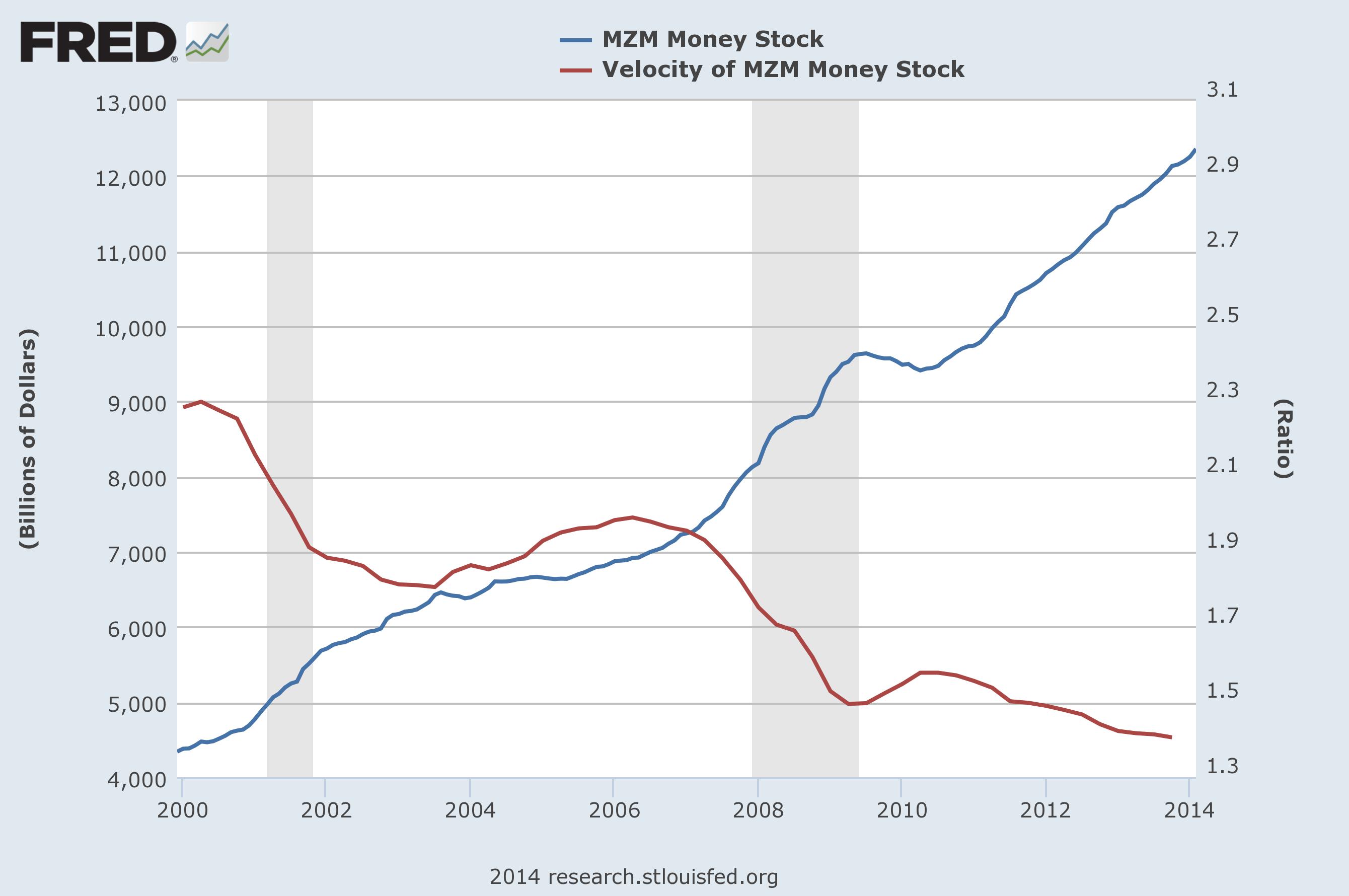

How much of that is there? About $12.3T in total, and it grows all the time (blue line on the graph below). But it has been turning over less frequently, as shown in the graph of velocity (GDP/MZM, the red line):

Data from the St Louis Federal Reserve

You can take the “velocity” as roughly the number of times a buck turns over in one year through the economy. The chart above shows that coming into the current Depression in 2001 it was over twice a year, falling to 1.75 times by 2002. It never recovered to more than 1.92 times (April, 2006) before it fell off a cliff in 2007 (before the “official” recession even began!) where it hovers today, about 1.4 times.

What this means is that for all the money out there in the world, it feels as though there is considerably less than there has been. The velocity today is only 75% of what it was in 2006, the last time anyone felt remotely flush with cash.

The presses keep rollin’

This suggests that if you wanted to have the same effect on the economy with the money you have, there is room for about one third more of it around, or about $4.1T. If the Fed wants to go in for one Hell of a lot more “Quantitative Easing”, it could print upwards of that much before we can reasonably expect a heavy dose of inflation.

That number is shocking for many reasons. It suggests that the shortfall in our economy is far more than anyone has even tried grapple with so far. It also demonstrates the key characteristic of a Depression over an ordinary Recession, two terms that have always seemed a bit murky. In a Depression the supply of money falls so hard that there simply is not enough to go around, representing a failure of the general money supply rather than an oversupply of any given product or service.

An argument could easily be made that the velocity of money is a function of far more than economics – that the rate at which people spend is not just what they have on hand, but how much they think they might have in the future. That’s why the we use the term “Depression”, a psychological term, to describe the situation. It also goes to the heart of FDR’s famous 1933 speech proclaiming that “The only thing we have to fear is fear itself.” Much of what is going on is a matter of attitude and anxiety.

“This is how it is. Got it?”

So can the Fed step up and print $4.1T more tomorrow? Sure, why not? It can print that much and cancel loans all over the place, getting that money into circulation and generally opening up wallets and convincing the world that tomorrow will be a better day. The problem is that if it over shoots and the velocity jumps up again, there are suddenly way more US Dollars than anyone needs and inflation erupts.

That is what Fed Chair Yellen is keeping her eye on as the stimulus continues. But without significant inflation, there’s no reason to panic – yet. But we can be sure that if the velocity of money did change quickly, there would be a lot more inflation overnight.

Good blog. All that money has to return as inflation someday. If you are anywhere near right about 2017 we may have a big problem.

Thanks, and we might very well have an inflation problem. But that would help free up all that money in a big way. More inflation might be good for us.

I can vouch that money doesn’t turn over like it used to. Anyone that has it is trying to keep it.

Yes. One thing I forgot to mention is that if someone is paid biweekly and they live paycheck-to-paycheck, their velocity is about 26. We found before that in the cash economy it’s at least 7. So how does it get to just 1.4 overall? A lot of money is being sat on.

Pingback: The Amazing Dollar | Barataria - The work of Erik Hare

Pingback: The Underground Economy | Barataria - The work of Erik Hare

Pingback: One Last Bubble? | Barataria - The work of Erik Hare

Pingback: Happy Christmas, Happy New Year | Barataria - The work of Erik Hare

Pingback: Fed Raising Rates …. When? | Barataria - The work of Erik Hare