The Federal Reserve of Kansas City puts on the big event every year – and why not throw a big party when your territory includes Jackson Hole, Wyoming? This year’s production concluded after presentations and official pronouncements from all the top central bankers of the world – Mario Drahgi of the European Central Bank (ECB), Haruhiko Kuroda of the Bank of Japan (BOJ), and our own Janet Yellen. It’s a must-see event if you want a front row seat for the big show of policy changes among the most powerful people in the world.

This year, the theme was “Re-Evaluating Labor Market Dynamics”, and the power players from around the world made it clear that nothing is going to change in the near future. If that sounds like the biggest let-down for a big show ever, you’re right. The Fed never intended for this to be a huge theatrical spectacular. It’s a place for central bankers to get together and agree on things. And what they agreed on, more than anything, is that in the developed world there is nothing more important than figuring out just how much “slack” there is in labor markets and how to take it up.

But it’s more exciting than it seems if you want to predict what will happen in the next year.

“This is how it is. Got it?”

The coverage from the financial press is huge for this annual conference. Last year, both Fed Chair Ben Bernanke and ECB Chief Drahgi stayed away, making it seem far less important. This year they all showed up and more or less said the same thing:

Labor markets are in trouble, and there are in more trouble than we currently know how to measure. Wages are stagnant or falling, and that’s the biggest contributor to income inequality in the developed world. And something has to be done about it.

The focus on labor markets is far from academic or boring. It’s common for most people who worry about income inequality, which is to say the political left, to not trust big institutions that measure money in trillions of dollars. That sentiment is only logical, but it’s horribly misplaced. In a time when governments are constantly pulling on the leash of austerity, central bankers are the ones who are doing everything possible to not only improve life for the average worker, but to make sure that they know what “improvement” means.

That may sound completely backwards and hard to believe. But it’s true.

Workers of the World, Unite!

Exactly how powerful central banks came to be the best friends labor has in power (other than the power they can create) remains a mystery, but it’s definitely true. It’s simply not spoken in terms that most people can easily understand. Consider Yellen’s pronouncement that “Tightening monetary policy as soon as inflation moves back toward 2 percent might, in this case, prevent labor markets from recovering fully and so would not be consistent with the dual mandate”. In other words, she isn’t going to support raising interest rates until there is a rise in wages.

Yellen went on to tell us what it will take to raise interest rates in the next year. “If progress in the labor market continues to be more rapid than anticipated by the Committee or if inflation moves up more rapidly than anticipated… then increases in the federal funds rate target could come sooner” and that “if economic performance turns out to be disappointing…then the future path of interest rates likely would be more accommodative than we currently anticipate”. To translate this: it’s all about the jobs and how quickly we see them being created.

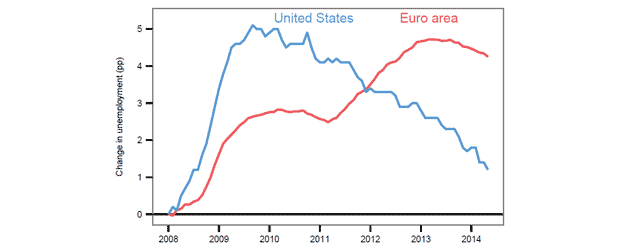

Drahgi of the ECB was even more blunt. The chart, shown here, comes from his presentation. He pretty much told the audience, “If you think you got problems, hoo boy,” and confessed that the Eurozone is lagging way behind the US in job creation, a figure he’s watching carefully. BOJ’s Kuroda said about as much for Japan, too. It’s all anyone is watching all around the world.

Most of the conference was much more technical and focused on ways of measuring key aspects of jobs and their creation. The leaders all agree that there is too much “slack” in labor markets, but figuring out just how to measure that so that they know when there is improvement coming remains a mystery. We have Yellen’s Dashboard, for one, but the elves who toil away in her workshop to deliver a good Christmas for all have to figure out just what is going on to make it happen. And they are focused on it.

What’s the big takeaway from the Jackson Hole Conference? That nothing is going to change anytime soon, at least until there is upward pressure on wages and much fuller employment. No matter what you read in the next year, this is the bottom line. And the central banks of the world are, apparently, the only ones who really care about the workers of the world all the time – as backwards as that seems.

The idea that the Fed is looking out for working people more that anyone else is never going to sit well. They have their own agenda and besides even if they do want to improve things there is only so much they can do. I think its just window dressing.

The Fed is very much on the side of labor here. I know that sounds strange, but it is very true. Everything they are doing is for more employment right now.

At least someone is doing something even if it’s not nearly enough. Do you think they can do more? It seems like this isn’t what the fed is there for.

It isn’t what they were designed to do, but they are now claiming it is part of their “dual mandate” to keep the economy moving. I honestly don’t know that they can do more.

One thing I forgot to mention again is that the current stimulus is still running very hot, about 2% less than it should be by the best calculations.

Pingback: Bizarro World Finance | Barataria - The work of Erik Hare

Pingback: Job Loss Hits a Milestone | Barataria - The work of Erik Hare

Pingback: 2014, ex Machina | Barataria - The work of Erik Hare