In the old days, if you needed money you went to a bank. They might loan you money for your home, your car, or your business based on an interest rate slightly higher than the net paid out for deposits. They made their money on the “spread” between the two, matching up assets they had with liabilities (like you) outstanding. It was a quiet, conservative life. It was boring.

Today, most loans wind up not being held by banks in anything like the traditional sense. Nearly all liabilities are packaged up and sold to a “shadow banking” system where people buy these “asset backed securities” and make money based on the float. It’s a more flexible system that allows nearly all risk to be offloaded onto investors – who bear it as a system. It’s good for the borrower, it’s good for the bank – but the risk is held by the investment world as a whole.

That “brittleness” is the bane of the modern financial world – and the future. How we learn to manage it is the future of finance and the difference between a world that is stable and reliable or capricious and impossible to understand.

“You’re money’s not here … it’s in your house, and yours!”

The old system was simple enough to understand and remarkably easy to regulate. Any bank, or bank regulator, simply needed to add up the assets and liabilities held by a bank to determine how solvent the institution was at any given moment. Banks were the center of credit in the world, and their relationship with their depositors and borrowers defined them.

The term “shadow banking” sounds terribly ominous, but the concept has been around for a long time. GM and GE both got into the credit markets by making loans to consumers who would buy their products without an actual bank ever stepping into the picture. If you think about it, the diversity of money flowing in and out of the consumer market away from banks makes for a more robust system overall. But how do we judge its soundness?

This became the issue in 2007 when it became clear that it was impossible to judge the overall strength of shadow banking without summing up the risk of each individual loan in the system. That was the problem. A company that only writes mortgages, and then offloads the risk to someone else, has an inherent interest in writing more mortgages no matter how dodgy they might seem. When that market goes bust, their income takes a dive – unless they can find new ways to sell mortgages.

Specialization like this is a recipe for a bubble, every time.

The same thing has happened in China, where regular banks never really did take hold as the center of the credit world. Large manufacturers finance their vendors because there is really no other option. Summing up the liabilities becomes very difficult because it’s hard to understand the credit risk taken by the manufacturer. What is clear is that a major downturn in Chinese manufacturing will be magnified into a huge credit crisis which many people have been waiting on for more than a year.

It hasn’t happened yet. It may not happen after all, but we’re still watching for it.

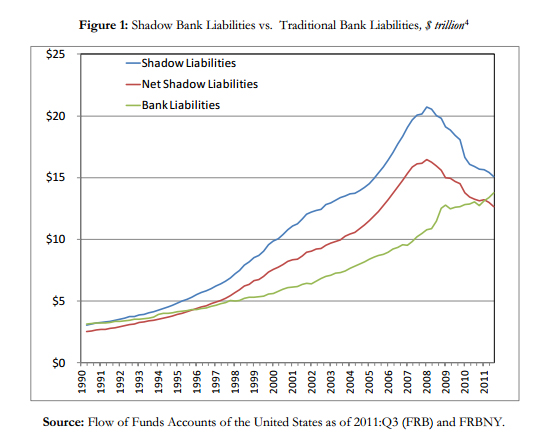

The size of the shadow banking system in the US is roughly the same as the regular banking system, and has been since 1990, as shown in this chart from the New York Federal Reserve:

Liabilities in traditional and “shadow” banks, from the NY Fed.

Note that it was the shadow banking that ran away in the 2000s before collapsing. Regular banks more or less kept on keepin’ on through the crisis. Shadow banking is declining in net terms, avoiding all double-counting of liabilities held by different institutions (red line). But it’s still over $12T today and very much still growing.

The problem remains a truly fundamental problem for any capital system, which is how to properly evaluate the risk. Old fashioned banks operate much like today’s credit unions, in that they spread out risk over many different kinds of loans but were concentrated in a geographical area. Investors in the shadow banking system have geographical diversity but have to build their own diversity in their portfolio as they see fit – assuming they know what they have purchased.

This system, built in an information age, is plagued by inadequate information of the kind that used to be handled on a more personal level.

Oooooouch!

The key to the system of the future is resiliency, built up by properly understanding risk. Any regulation of this new system has to start with disclosure, like any good system in a free market. But what is being disclosed and how good is that information? It’s hard to know just what is happening in St Paul when you’re sitting at a desk in Germany, for example.

Meanwhile, shadow banking is the wave of the future – as it should be. If we can figure out how to manage this risk as a system it means more fluid credit and likely better access to credit in a robust, distributed system. Where we are failing is where so many things today fail, in the connections between the holder of the liability and the person on the hook for it.

Without that, the system itself holds far too much of the risk. That’s where bubbles and bailouts come in – as well as the desire to start regulating more more stringently. Shadow banking is far from new, but it is the state of banking today. What we do to manage it defines the future like absolutely nothing else.

Banks are terrible. If they didn’t charge fees for everything they probably wouldn’t be in this much trouble. There is no reason to use a regular bank anymore and they did it to themselves.

That is a lot of what happened. Once banks lost the personal touch they lost the one edge that they had. Credit Unions own that now. The rest of it is just money.

At some point this goes back to my “Economy of People” musings.

I wouldn’t say this is the most important issue but it sure gets expensive when it isn’t handled right. What are the regulations in place now after 2008?

It comes down to proper evaluation of the loans and how good they are, which I don’t think has been figured out adequately – and most of Wall Street agrees. The industry needs to clean itself up, and they really haven’t.

Any system that gets us away from banks is a good one. REITs are a good way to bundle and manage home loans as long as they don’t lie about who they pushed the loan onto. I guess I have to accept that some regulation is needed to make it work but fraud is still fraud and there are already laws in place to stop that, they just need to be enforced.

Congratulations to the Donkeys or Elephants or independents tonight.

“When you were young and your heart was an open book…You used to say live and let live…”

“Live and Let Die”

It’s all just blather, really.

Pingback: Chinese Meltdown, Latin America Next? | Barataria - The work of Erik Hare

Pingback: Other People’s Money | Barataria - The work of Erik Hare