After years of low interest rates and quantitative easing that amounts to more or less printing $4.5T, it would be easy to predict that inflation is bound to rise eventually. More dollars means, by supply and demand, that they have to be worth less, yes?

But the opposite is happening as the US economy charges ahead as the strongest economy in the developed world. While we have stopped stimulating our economy, Japan and Europe are only accelerating their programs. The US is poised to lose the currency war with the strongest currency standing – and a guarantee of lower prices for a lot more than just gasoline in the near future.

What keeps the global economy keepin’ on.

The strengthening of the US Dollar comes as pressure grows on the Federal Reserve to raise interest rates above a nominal zero Fed Funds Rate for the first time since 2009. Most analysts agree that it has this has to come by April, increasing along with it rates for everything from cars to homes and even credit cards.

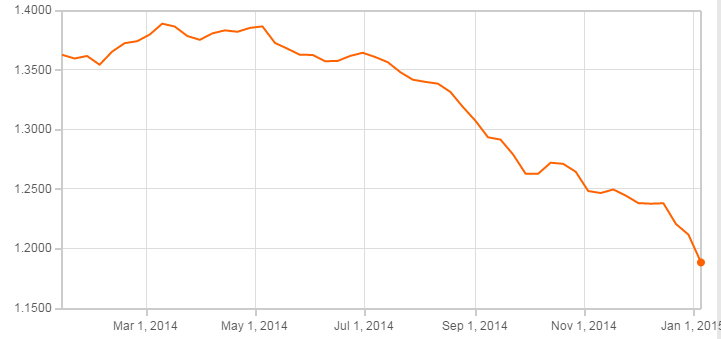

This will only increase the value of the Dollar, which has been on a huge run lately. It’s up 13% against the Euro over the last year. It’s also likely that this trend will continue as the Euro and the US Dollar move towards parity, which could come as early as 2015.

US Dollars per Euro over the last year, from Oanda.com

Ready for a trip to Europe? It’s 13% cheaper than last year and falling.

Because nearly every commodity is priced in US Dollars, the price of nearly everything is likely to keep falling, too. This could easily pick up steam as the greenback’s gains continue. It’s likely to be the story of 2015 as our currency gains throughout the world.

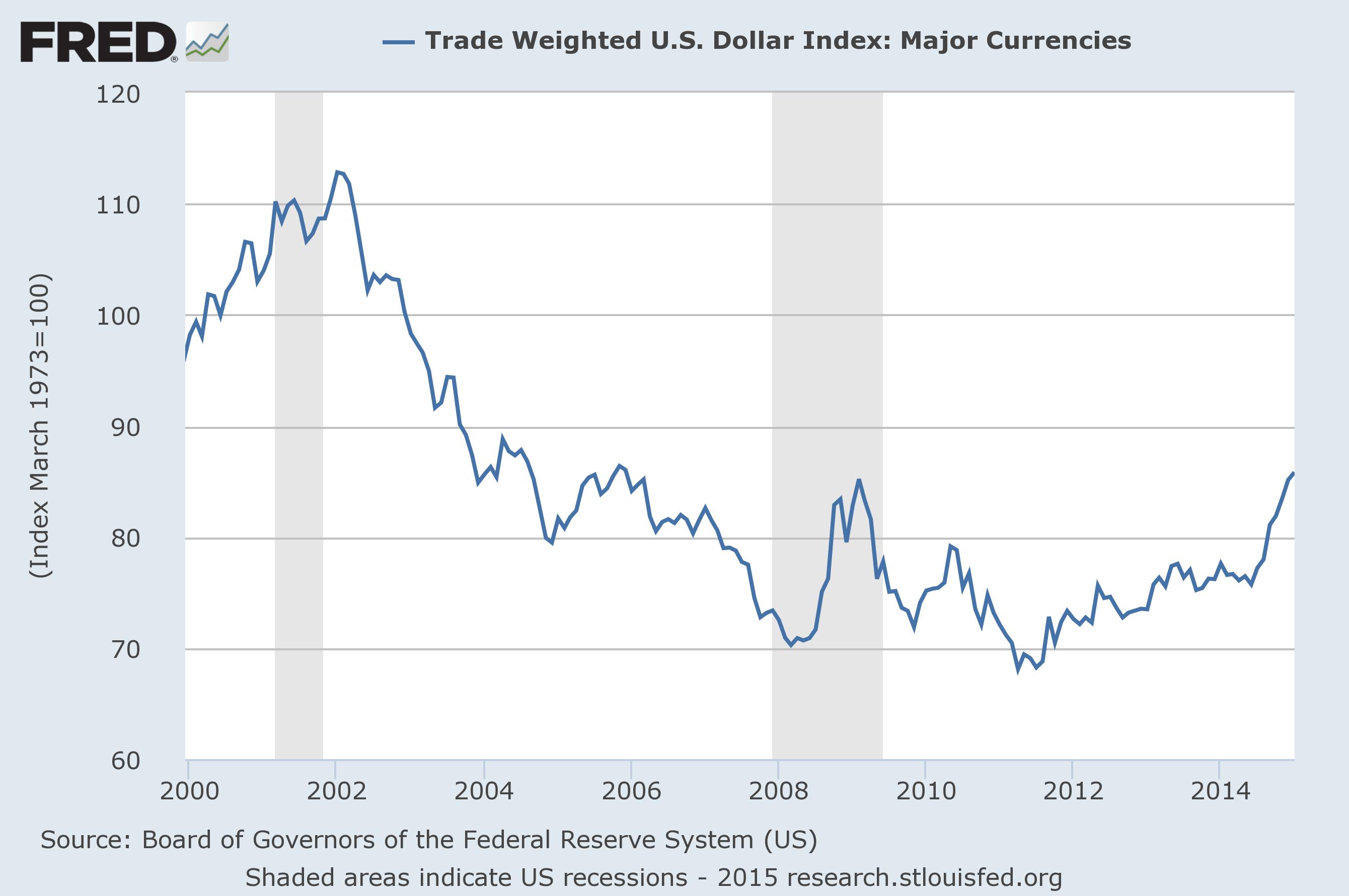

In historic terms, it has a long way to go, too. Below is the US Dollar Index, a measure of the strength of our currency against a basket of other currencies weighted by how much trade we do with them. We’re nowhere near the level of strength we enjoyed back in 2000, before the recent Depression started, despite the recent increase:

The US Dollar Index since 2000, from the St Louis Federal Reserve. The recent gains have room to continue in historic terms.

The only thing that doesn’t seem to be getting cheaper against the US Dollar is gold, which has been rising lately. The same pressure for a safe haven investment is also increasing the yellow stuff, which is rising just a bit faster than the green stuff lately.

Where are all those containers going?

Where will this end? The short answer is that there is no reason to believe it should end any time soon because there is no reason to have any faith in the economies of other developed nations. A general slowdown also appears to be gripping global trade, which is not increasing as quickly as it did over the last four years, meaning the developing world isn’t going to pick up quickly either.

While this means great bargains are coming for US consumers and a Eurotrip is going to be the hot feature of the summer, it’s a dangerous thing for the economy. Like any other nation, we benefit from a weaker currency that makes our goods cheaper and thus encourages hiring. As strong as things have been, we still need jobs. A slowdown in job growth is not going to help us over the long haul.

Predictions of inflation that have been a regular staple of Federal Reserve criticism will not only prove wrong, they will likely prove dangerously wrong. We have exactly the opposite problem as the deflation and stagnation that have plagued Japan and Europe are exported as effectively as their central banks can engineer it.

There will be almost no pressure on the Fed to raise interest rates much in the coming year, tempting as it may be to remove the punch bowl before the part starts. The years of stimulus and cheap money are likely to continue until there is a growth in global demand no matter what we do.

And that’s more likely to come from the developing world than anywhere else, especially if the US economy continues to expand. Inflation? Just the opposite is likely. How this shakes out is going to be the story of the coming year.

You said in the past that the dollar would not be the world currency for much longer. Are you backing off of that? I agree that a strong dollar is a double edged sword but will this last?

The timeline on that is up in the air. 85% of world trade is still denominated in US Dollars,but it’s slipping a little all the time – slowly. Developing nations like China and Russia are very hot to put an end to that, but they only have so much pull.

A strong US economy alone in the developed world puts the brakes on that change, I think, at least for the time being. Moving away from the USD won’t accelerate until after the next boom cycle starts, I think, which is to say after 2017.

It would be wise for us to support that effort, but a strong USD has such great political pull with US consumers I don’t see that happening.

Low gas prices are a huge benefit but people are going back to buying gas hog SUV’s again. If this is going to continue through 2015 we are going to need that oil from North Dakota after all.

We will need it. Maybe not now, but eventually. 🙂

Time to plan a trip to Europe?

Yes! Expect that to be the trend of the summer – “Go to Europe, everything is so cheap!”

Pingback: Forward! 2015 & Beyond | Barataria - The work of Erik Hare

Pingback: Franc-ly You Must be Kidding | Barataria - The work of Erik Hare

Pingback: A Tale of Two Classes | Barataria - The work of Erik Hare

Pingback: Fed Raising Rates …. When? | Barataria - The work of Erik Hare

Pingback: Fight for $15 | Barataria - The work of Erik Hare