The stock market is tanking. It has to bode poorly for the economy, yes?

If we’ve learned one thing over the past six years, it’s that what is good for investors is not necessarily good for workers – and vice versa. As Herman Miller, an accountant friend of the family told me as a child, “Never forget that the stock market is only a market for stocks.”

So what is the future for stocks? In the short term, not good. For workers? That may be a better story. And if the fortunes of these two classes cross each other it’ll be the story of this year as the ups and downs and devilish details read something like a novel.

The good numbers are always buried.

The stock market itself is hardly in trouble. Last year, the S&P500 managed an 11.4% gain, about 10% after inflation. It’s worth going back to the Barataria prediction in the market-spooky month of October to see how we did.

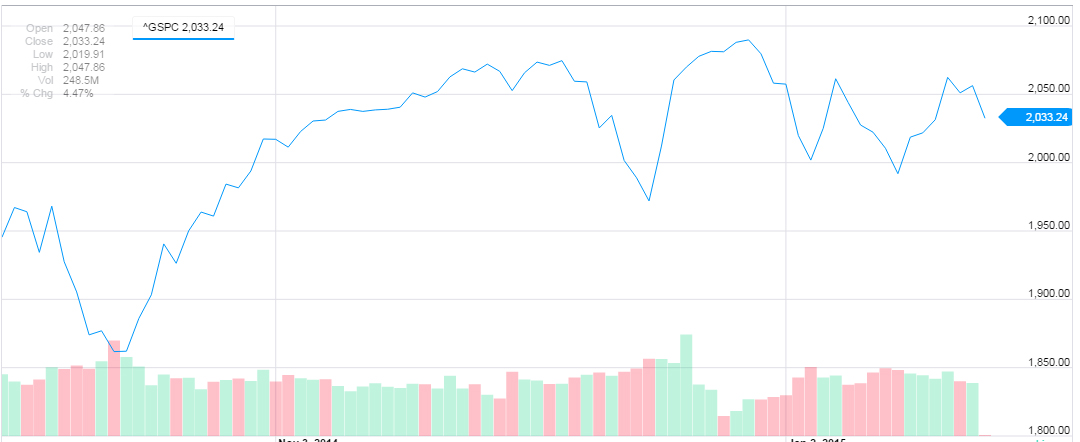

At that time, the prediction was for a lot of volatility and a small swoon by the end of the year. What we got shortly after that posting was an S&P500 dive back down to where it started the year, followed by a ragged increase. Not exactly a good prediction. Here’s what it looked like from October until today:

The S&P 500 since October. It’s been one Hell of a ride, and it’s probably not over.

Given this track record, why would anyone listen to Barataria now? The short answer is that while we were off on the timing, the direction is utterly inevitable. Corporate profits are down as the strong dollar limits income from overseas and puts competitive pressure on US manufacturing. The European situation has only become worse with Greece electing an austerity hating government that is willing to take on the Germans like no one did before.

It seems like fun when you’re at the top.

The volatility in stocks is a result of two forces on them, an uptick in the economy facing a corresponding uptick in interest rates. Since the market doesn’t look forward more than a few trading days anymore, we can expect that future events, no matter how certain, are simply not priced in. The fall we see now is something that should have come last year – but didn’t.

We will find out about interest rates on Wednesday as the Federal Reserve Open Market Committee releases their intentions, and we will know more about 4Q14 GDP on Friday. It should all point to a mid-year rate increase, even with mild inflation pressure. That’s about all anyone cares about.

No one is paying attention to jobs anymore for one simple reason – it’s been going well. We’ll find out next week how well, but it’s been a good ride so far. The economy remains on a pace to absorb the unemployed over the next two years, with labor markets tightening already. In an era where bad news is good news, driven by Fed watching, we can say that the only unequivocal good news is no news.

Which is to say, stop watching the news – it’ll drive you crazy.

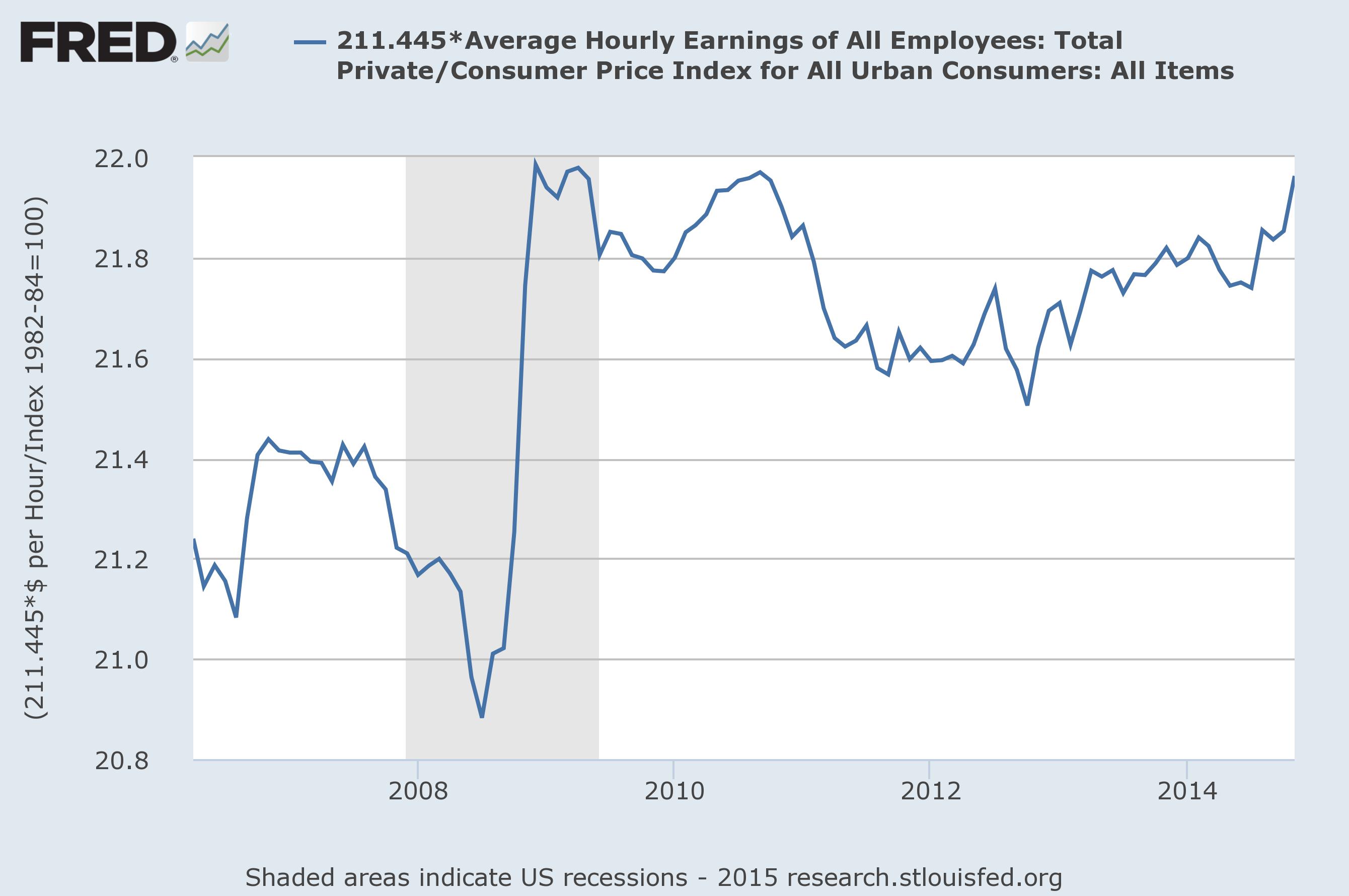

We can see how upward pressure on wages may already be happening in this chart that shows average wages, adjusted to constant 2008 Dollars:

Inflation adjusted hourly wages, on average, since 2006. From the Federal Reserve of St Louis.

Note that wages spiked upwards right in the middle of the huge firing binge of 2008. That’s an artifact of the marginal workers being let go and the most productive employees staying on – often working long hours. It makes the wages of 2006 look pitiful by comparison.

Wages started to fall as the economy trudged along, hitting a low point in 2012 – two years after the bottom for employment. When any given worker can be replaced by someone off the street, wages stagnate or even fall. We saw that.

Construction is picking up along with everything else.

But now they are going back up and are, in real terms, higher than ever before. It’s an important milestone. It’s also a trend that we can expect to continue as employment moves forward and there are fewer workers competing for every job opening.

How does this all shake out for investors versus workers? Certainly, the big gains for investors starting in 2010 gave them an early lead in the race between the classes, widening the problems with income inequality. But this should be the year that this starts to change as the economy normalizes and gets back on track.

It may be a bad year for investors, but it’s most likely to be a neutral year of few gains. Those should go to the workers if trends continue. And those trends didn’t get started a moment too soon for working families in America.

Wall Street: it it time to innovate and get off intersection of Easy Street and Fed

Yes! Absolutely. And that will happen once some people start making more money the old fashioned way. Who knows, maybe even manufacturing can become “hot” again!

Unfortunately I doubt that manufacturing will revive, but I certainly hope it does!

With a strong Dollar it’s unlikely, but the more we have customized / specialized demand the more advantage there is to being local in the same economy. So there is hope!

http://www.economonitor.com/blog/2015/01/the-battle-going-on-in-the-financial-markets-right-now/

The shocker in this article is that the author thinks wages will remain flat or decline a bit. I don’t think he proves it, but he attempts to interpret the bond and equity market recent performance

This implies that salaries are dependent on the bond / equity markets, which I disagree with. I think they have their own markets based on their own supply and demand. I see supply of labor going down and demand if anything going up in the next few years. Yes, that money has to come from somewhere, but it will have to come. Automation is the only alternative.

Unemployment has been going down, so a decreasing supply of labor is not a likely phenomenon.

I meant supply of available labor or excess labor.

http://www.voxeu.org/article/ecb-s-qe-decision

European QE above.

Maybe the joy of the new year fading and international affairs concerns is affecting the markets too….

Europe is a real basket case right now. It’s the biggest threat to our own economy, but we’re not heavily dependent on them. I could well be wrong, but I think we can march ahead without them – especially if our trade with the developing world keeps improving.

When I see that graph of wages jumping UP! in 2008 the first thing I think of is the skills gap. Is this proof that it is real? Higher skilled workers not only keep their jobs but they are paid better right?

That is an excellent call! I will think about it. It certainly shows the perception of the skills gap, if not the reality.

The price of stocks is more about the available investment capital than anything else. If the stock market keeps its status as a relatively safe haven for capital around the world it will continue to go up no matter what else is happening anywhere. Pay attention to the saying you have in this post that the stock market is just a market of stocks. That is all it is at the end of the day.

I agree. They are all their own market.

Investment income is definitely up this year. Its not so much the stock market being up as clients were in it more. I don’t know if that means anything.

If inequality has been a growing problem, it doesn’t seem logical that wages would be going up.

If you look back at 2012, wages were still falling. Most of the data used for income inequality arguments is older than that. It takes time to have a good picture put together with Gini Index, etc. So my guess is that Income Inequality is already improving, or at least stabilizing.

Also worth noting is that this graph can’t be used for income inequality arguments by itself, since it leaves out the unemployed (zero income). I can dig up the total earned income charts at the St Louis Fed for that and compare it to investment income.

There is a difference, of course, between paid wages (unadjusted) and real wages, which often leads to confusion over living wages, the cost of living, and how much money people are actually making that goes to anything more than subsistence. In my analysis, this is one of the major issues of North American economics, that the ability for a North American worker to actually amass a savings, let alone push past debt, is not specifically reflected in statistics like this. Moreover, when we are talking about an increase in wages (of any kind) we need to also discuss increases in other costs, such as health care, that often increase at a quicker rate which effectively reduces wages.

I completely agree. The stat that I presented here can be used ONLY for a narrow argument that we are finally starting to see upward pressure on wages – a reversal of the trend downward from 2008-2012.

A lot has to happen before we can say workers are in good shape, yes, and I still predict that things won’t look genuinely positive for another two years. But we can see the trends developing that have the potential to create a real improvement in the life of working families as lessen the inequality problem.

That it comes at a time when we can reasonably expect investment income to stagnate is especially interesting, IMHO.

If I could have dinner with Milton Friedman, Hyman Minsky and Joseph Stigltiz I would ask them to fully discuss this this observation:

“One thing I read recently claimed that net impact of U.S. policy (local, state, federal, federal reserve) on the great recession was mildy contractionary, whereas the European Union took the path of austerity.”

_______

Even the casual observer would say the macroecnomics outcomes in the eurozone are different than those in the U.S. Of course the challenge is to explain why.

I understand that the German Central Bank opposes European QE. Larry Summers says QE won’t really work in Europe. Another note I would add is that Brazil is raising interest rates to combat inflation. Russia is… Well, we know that at times Russia makes deep historical mistakes, so I forgive them.

Local and state governments were definitely contractionary after 2008, and the Federal was after a binge in 2008-9. The Federal Reserve went whole-hog the opposite. It appears to have worked out, but the amount of QE it took is horrendous. There had to be a better way.

As for Europe – honestly, I don’t know, and I’m only comforted by the fact that no one seems to know. They have such huge demographic issues on top of the whole “What is Europe?” social and policy problem. I think the German hard-line is probably incorrect just because it’s a hard line. But they have a LOT to work out and I wish them the best.

As for asking Friedman and Minsky (not so much Steiglitz) I’d throw in Keynes and wish we could have a roarin’ panel discussion. But the great minds only live on in what they wrote and what we can interpret, sadly. Not so many great minds today, eh? Larry Summers? Yeesh.

Europe ought to reconsider monetary union since it is too hard to implement across so many sovereign nations.

If they wanted to united they should have done so under Bonaparte. That way they could all speak French, and eat more similar wines and cheeses. How can you unite a continent with so many hallowed food traditions.

Pingback: A Tale of Two Classes | My Blog

Pingback: Redefining Work | Barataria - The work of Erik Hare

Pingback: Redefining Work | Posts

Pingback: Fed Raising Rates …. When? | Barataria - The work of Erik Hare

Pingback: Logistics | Barataria - The work of Erik Hare

Pingback: Happy New Year! | Barataria - The work of Erik Hare

Pingback: Panic – or Laugh? | Barataria - The work of Erik Hare

Pingback: Work For All? | Barataria - The work of Erik Hare

Pingback: Work Redefined | Barataria - The work of Erik Hare