It’s been one week since Barataria made the prediction that if good news came in on jobs the stock market would tank. The good news came in, with the headline unemployment number slipping below 6% for the first time since 2008. Immediately, the market proved Barataria to be wrong. Then right. Then wrong. Then right, again.

It’s been a roller-coaster of a week. How does that stack up with any prediction at all?

It’s probably time to make another prediction. Let’s stick with the first one, that the stock market is due for a decent but not horrific “correction” that re-affirms that we’re really still in a secular bear market. But with the focus on Fed action we are also entering a time when the logic of the market finally turns rightside up – and good news will once again become unalloyed good news.

We just have to get through the ride before we know what’s up – literally up.

While looking at stocks over a five day period is going to give anyone invested in the market an early death, the last five days have been particularly interesting. There isn’t actually a direction to this market other than volatile. Here is trading on the S&P500 over the last five days:

The last five days of the S&P500, from Yahoo! Finance.

What seems to have started this off was, indeed, the good jobs report. A summary in table for is called for, using the last close before the Employment Survey came out.

| S&P500 | Date | % Change |

| 1946 | 2-Oct | — |

| 1968 | 3-Oct | 1.13% |

| 1965 | 6-Oct | 0.98% |

| 1935 | 7-Oct | -0.57% |

| 1969 | 8-Oct | 1.18% |

| 1928 | 9-Oct | -0.92% |

This is crazy behavior by any means, but in retrospect it should have been predicted. OK, in retrospect everything can be predicted, but this is especially interesting. As we’ve noted, there is a lot of good news in the world as people are finding work and the economy is stumbling towards a decent looking recovery.

But that’s bad news only to those who are worried about the excessive reliance on cheap money that’s built up because it looks like, at this rate, the Fed will have to raise interest rates to a positive number sometime in mid 2015.

Good news or bad? Hard to say right now. But “bad” has to win out before we can set it up so we can recognize just what’s “good”. If that doesn’t make any sense, consider this one of those financial news stories a year in the works.

You’ve been warned

Barataria has noted the rhythm of financial news, where big events take a full year to blossom and develop into stories which hit the mainstream of American thought and are amplified through the mainstream media. There are two problems with this long cycle of news stories for those of us who note them towards the beginning – one is that sometimes the problem is taken care of before it becomes a mainstream story and the other is that the details of how the problem will manifest itself can’t be known until it bubbles up – that is, the story isn’t quite written yet.

Actually, there are three problems with this news cycle in that no one remembers who wrote about something a year ago, but I’ll assume you don’t care about that as much as I do.

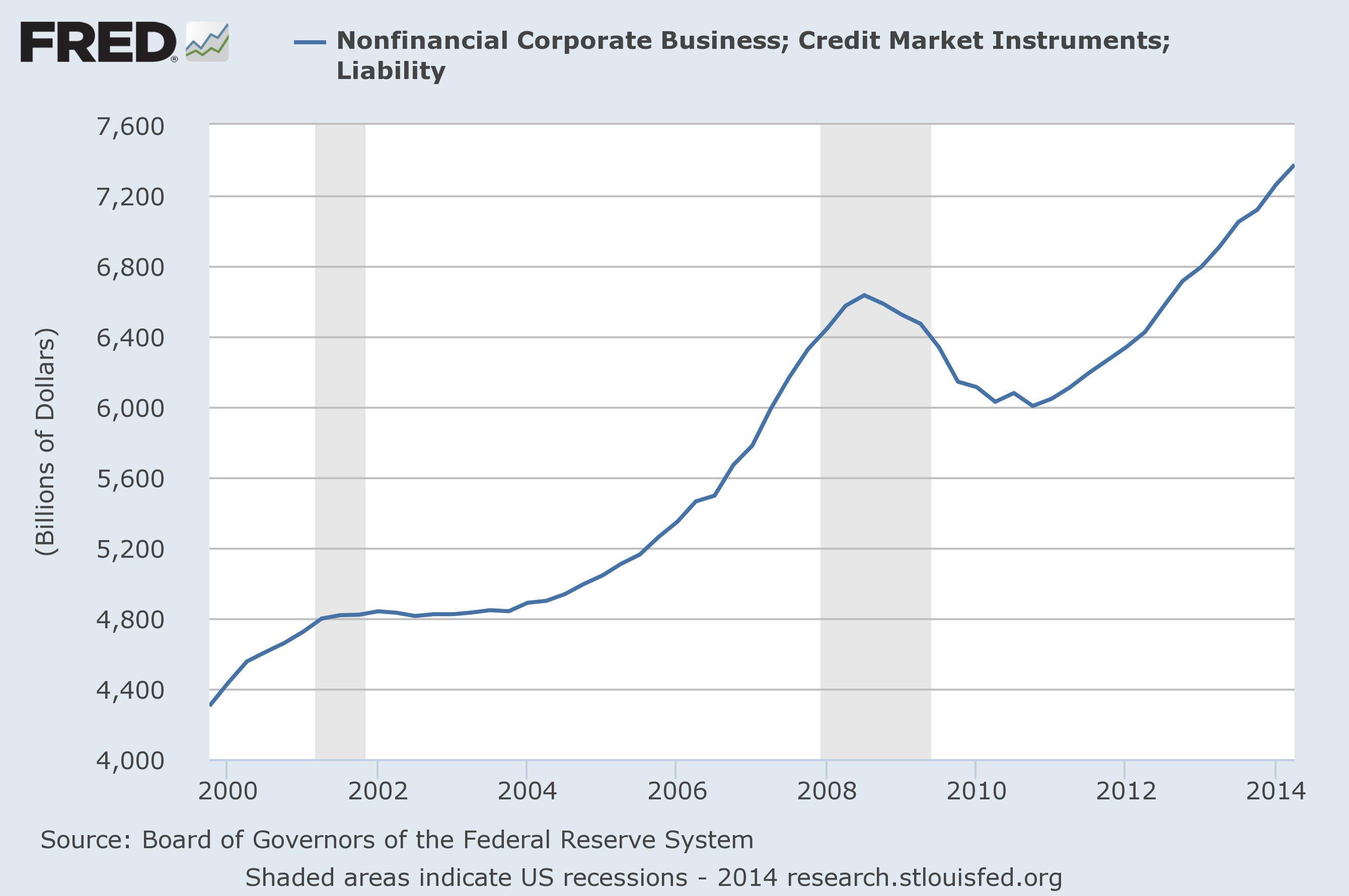

The problem with rising interest rates is there is so much debt out there dependent on cheap money that even a small rise will become a big expense in a big hurry. And you can bet this will be taken care of before the problem can fester into a really big story, at least in part. Take a look at total debt from nonfinancial (goods or service producing) companies since 2000:

Nonfinancial corporate debt since 2000, from the Federal Reserve.

We’re way above the danger levels hit in 2007. What to watch for? This curve to at least level off to give companies a chance to grow into their debt, meaning that they will be less reliant on cheap money for real growth. At that moment, the darlings of the stock market will become those companies who are genuinely growing – which is to say bullish about their own business and hiring people to make it grow.

Suddenly, good news will be just good news again and all will be right with the world. But in the meantime we have something else to keep an eye on, which is the level of corporate debt.

In the meantime, the stock market will be something like a rollercoaster – which as we all know has a big drop at the end before everyone gets off the ride and stands around dazed. That’s still the best bet by the end of the year.

If you are going to start trying to predict the stock market you need your head examined.

General trends, is all. General trends. 🙂

I think you called this well even if it took a bit to start. All the talking heads are now focused on downside. Check out the breach of the 200dma on the SP500, pretty scary.

It is going about as it should. October will be a down month, hard to say on November, December probably dead. January it all should start up again, I think. This is just a temporary correction that reverts us back to an overall no gain (inflation adjusted) since 2000.

From there, it will build again.

This makes more sense to me now. Basically, you are saying that the reliance on the Federal Reserve is ending and that is why there is all the volatility? I saw that somewhere else, too. It would be great if companies were rewarded for expanding, hope that comes in the next wave or whatever they call it.

That is what we all have to hope for. I see that happening in about 2 years at this rate, so we’re pretty much on track for 2017.

Pingback: Glad Tidings | Barataria - The work of Erik Hare

Pingback: Forward! 2015 & Beyond | Barataria - The work of Erik Hare

Pingback: A Tale of Two Classes | Barataria - The work of Erik Hare