This is not an ordinary election year in many ways. For one, it’s not really an election year – the actual voting doesn’t happen until 2016. It’s also going to be the first Presidential election without Obama since 2004 as the White House becomes open.

But more importantly, everyone seems to understand that the economy and the politics of this nation are both changing. Stuff is seriously up for grabs. A desperate cry for attention might make all the difference.

Enter into this a bid for more Congressional oversight of the Federal Reserve, an idea backed by no less than 30 Senators, 3 of which are clearly running for President. It seems like a good idea all around – what can be wrong with more oversight? That depends on what’s being overlooked now, of course, and what can be done with existing law.

Plus, of course, we have the omnipresent Fed itself. Does it need to be reigned in?

“This is how it is. Got it?”

To understand the need to regulate the Fed we have to start with what it does now and who it has to report to. Janet Yellen, the current Chair, has introduced a period of remarkable openness where her policy terms are announced months in advanced based on key economic indicators. As the most powerful person in the world Fed Chair Yellen is doing a remarkable job of being transparent in this key area. But what else does the Fed do?

The Federal Reserve has four main responsibilities:

- To be the “lender of last resort” in the case of economic panic of financial meltdown,

- To act as the clearing house for all checks and bank wire transfers,

- To regulate and supervise US banks in accordance with US law, and

- To maintain the value of the US Dollar through monetary policy.

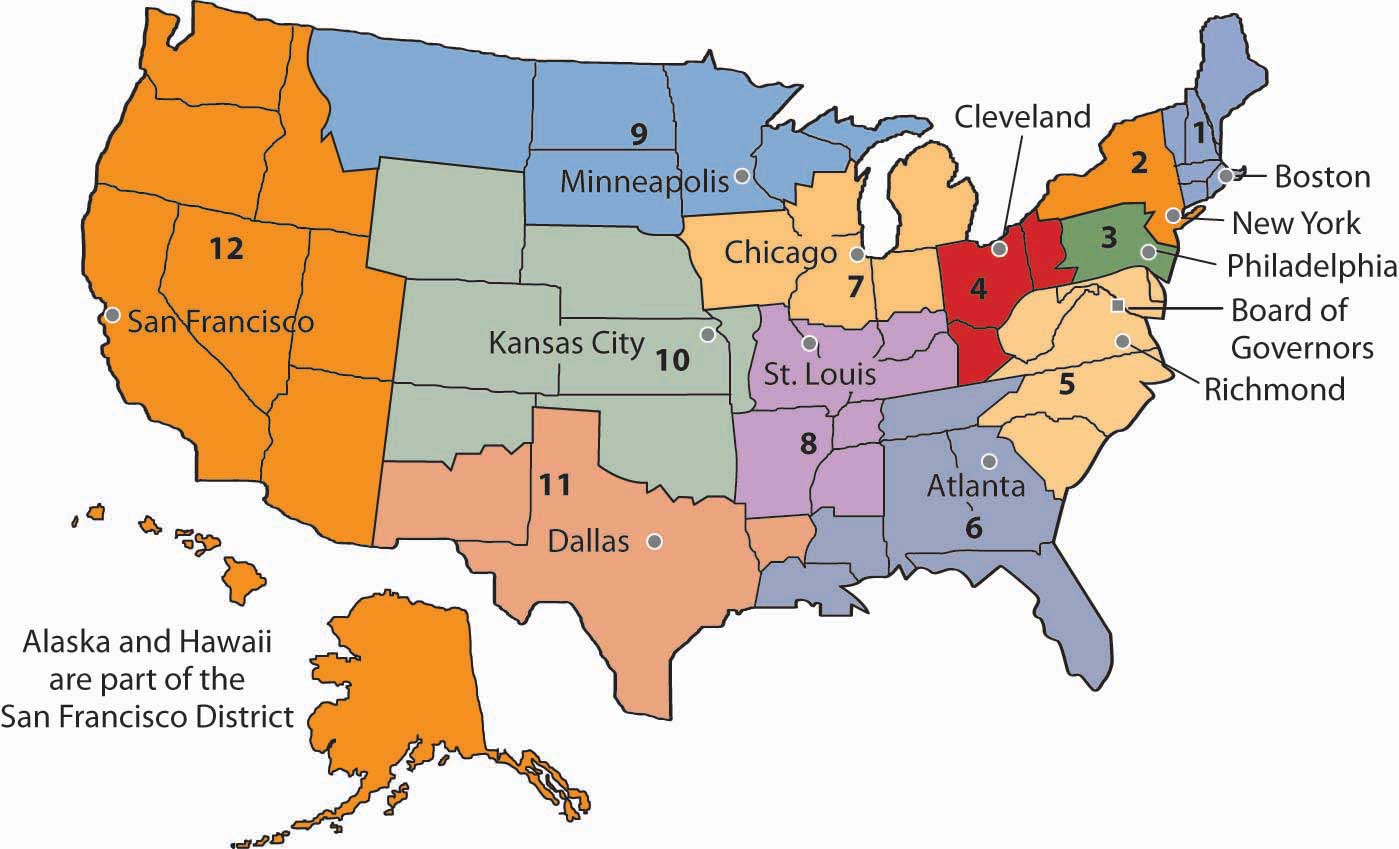

The 12 Federal Reserve Districts. All US Dollars are marked by which District issued them with letters A-L.

All of this is subject to Congressional oversight – which is absolutely never put into practice beyond the Fed Chair’s biannual testimony.

Monetary policy is the big deal, the one everyone focuses on. It is decided at the “Open Market Committee Meeting” where the 12 Governors from the regional Federal Reserve Districts (as pictured) decide, with the Chair, what their “Federal Reserve Funds Rate” will be. This is what they charge banks on overnight loans and, as such, influences the loans those banks in turn charge to commercial lenders.

The rest of the functions are never in question, but they should be. The Fed as a regulatory arm has set up a cozy relationship that has clearly given banks far too much leeway. The decision to give this power to the Fed was a decision to take bank regulation away from the messy world of politics. It appears to mean that, in practice, there is little pressure to enforce regulations and banks can get away with an awful lot.

But that’s not what is in contention here.

Sen Rand Paul (R-KY) is choosing to grandstand over doing actual work.

The proposal at hand is to “Audit the Fed”, which is to say conduct a full scale review of their books. The legislation, as discussed publicly, is all about checking over the books to be sure that it’s all in place. It sounds like a great idea, and an independent audit should be welcomed by everyone.

There’s only one problem – Congress could do that with the power it has already.

It’s unclear exactly what new powers would be given to Congress under the legislation proposed. Under Dodd-Frank, the detailed minutes of all Federal Reserve Open Market Committee meetings are released within two years. Everything the Fed does is relayed in a dizzying number of charts, graphs, and reports – much of which is available at the St Louis Federal Reserve’s website.

If you want to know what the Fed holds, that’s also easily available. They have $2.5T in US Treasury Bills on the books, for example, and you can see how that number has grown over time:

The Fed’s holdings of US Treasuries. Data, like nearly all the data publicly available, from the St Louis Fed.

What exactly that means is always an open question, of course. When the US Government pays interest to the Fed, where does it go? Can’t the Fed simply forgive these US Bonds and let us off the hook? They are the ones who print the money, after all, and owing them some of it back is a head-scratching problem – especially when the amount owed is so incredibly large.

We have the numbers already, and nothing is going to give us more information. What the numbers mean is the hard part.

Who is behind the curtain? There is no mystery here. Really.

But none of this is under consideration at this time. The call is for more openness from the Fed, which is arguably more open than most of the Federal Government. It certainly tells us an awful lot more about where the money goes than the Defense Department, for example, which has proven to be unauditable.

It’s an easy political call to write a bill that lifts the veil of secrecy and promises to reveal who the man behind the curtain is. The problem with this is that we know who is behind the curtain, and she’s a woman named Janet Yellen. Nothing is secret, and there are no mysteries.

There is a problem that very few people understand what is going on, but you can’t legislate your way through the mountains of detail that already exists.

If someone wants to propose that the Fed be stripped of its regulatory power in favor of a tough organization with a strong criminal investigation arm, by all means let’s have at it. But to simply audit the Fed? We can do that now. Let’s do it and put aside all the showmanship. There are other things we can worry about ahead of 2016.

It seems the more important question is why inflation is under the federal reserve target rate.

They should communicate that better.

_____

In the 19th century private banks could issue notes (money) if they held as capital a certain amount treasury bonds.

That tends to elicit different opinions.

The economy is just not firing up the way it should be. Velocity is still very low – but at least not dropping anymore.

Can you imagine what it would be like to have Wells Fargo Dollars in hand when you have little of the ol’ “Full Faith” in them? It must have been crazy to take paper “promissory notes” back then!

Well the banks discounted notes from banks further away or that seemed riskier.

The had more time back then and catalogs showing the different notes in the region.

The banks have always had to take into account demand for cash. I have to check but long term loans ma not have been as readily available.

… Silver coins were mostly the currency in the 1st half of the 19th century. So if you had gold you probably wanted to put it other than under your bed.

I think that the shakiness of this whole system is why there were regular panics – and huge spikes in the demand for silver and gold. It’s exactly what a Central Bank was created to put a stop to. It’s all about going to a system where banks could create reserves of capital and put money to work, rather than sit around in lumps of metal.

I should write about this, thanks. This is worth exploring. I think few people understand why we have a modern banking system.

I appreciate the way you explain how things work. I am slowly gaining a better understanding of the economy. Thanks for sharing!

Thank you again for reading and commenting! All of my posts include links to previous articles of mine or outside articles that I think really explain things well, if you want more depth on any one topic.

I definitely will do so. Thanks again!

More oversight is good. Perhaps the real problem is that none of this is reported & people have no idea what is going on. I agree that the Fed is not doing a bad job of running the economy, clearly they got us through this when politicians couldn’t agree on anything. But I agree that 2.5 trillion dollars in debt is just weird & have no idea what that means. Please explain it to us!

The mainstream press does not report anything related to the Fed worth a damn, no. That is indeed the real problem. Alternative sites tend to be anti-Fed and have a huge chip on their shoulder, probably because they are reasonably suspicious of the power the Fed has. But their judgement is horribly clouded and they can’t stand it when someone says “It’s actually all OK.”

I am trying to get my head around public debt held by the Fed. The more I think about it, the less I understand the implications, frankly.

the great apologist tells us to look the other way – nice

See answer above. You want to make change? Look for the real enemies and get something done.

There has to be a lot of oversight when this much money is at steak. Maybe you are happy with their bookeeping but how did they get so much debt on the books? It’s worth investigating.

They were very transparent about buying all the public debt, but it does deserve more explanation. If I were in Congress I would ask Yellen a lot of questions about it during her testimony. That hasn’t really been done yet. Congress can, and should, get more direction from them on this matter and use the power of oversight that they have to at least understand the risk fully.

Elizabeth Warren seems to agree with you for the same reasons. http://blogs.wsj.com/economics/2015/02/10/sen-warren-opposes-audit-the-fed-bill/ That’s good company to have.

Thank you! I am going to make good use of this. I expected a lot of flak from people when I posted this, but it is indeed good company to be on the same side as Sen. Warren. In fact, I think I nearly always am! 🙂

kudos to Obama for asking for war powers

Since we don’t actually declare war any longer, like the Constitution says.

Some financial things are tricky but an example is always helpful.

Say in a private transaction for selling a car the potential buyer doesn’t have enough cash on hand, but has annual income over a couple of years to complete payment. The seller can conceivably take installment payments. In accouting the seller then has a receivable or type of asset. The buyer obviously has increased debt. The seller extended credit. Credit should be extended upon proof that the person has the ability to pay. In a sense when credit is extended the money supply is kind of expanded. In haven’t mentioned interest rates but you get the idea. There is always a chance the debtor can’t or won’t pay back.

Most private car sellers want complete payment so the example doesn’t actually happen in real life.

Government debt is kind of a different story…but that is another story.

Back to Audit the Fed. The Federal Reserve System is a quasi private/public bank system. One of the chief complaints is that each of the district banks conduct their operations as if they were strictly a private corporation. Now the Board of Governors are appointed by the president and approved by the senate. The chair and vice chair are appointed from the board membership by the president and approved by the senate. But each Federal Reserve Bank bank appoints its own officers from the various member banks. Banks must buy into or own an interest in these bank branches. While there is a great deal of information that is openly available, there so much more than is guarded as private to the point that if congress wished to audit those branches it would need to use it’s subpoena powers to do so. If one wants to know the relationships tat Goldman Sachs has with any of the officers and other employees of any branch one would need a court order to produce such information. This is the real issue at stake.

It might also surprise you to know that the Federal Reserve System is the largest employer of economists, those with a PhD from an accredited university. The number is in the several thousands. Yes, there is a case for legislation to “Audit the Fed” simply for the reason that it considers itself a private bank and above oversight. I refer to the confidential investigation conducted by David Beim at the request of New York Fed President William Dudley.

Reblogged this on PenneyVanderbilt.

Pingback: Banks Amok? Perhaps Not | Barataria - The work of Erik Hare

Pingback: Curtain Rises on Kashkari | Barataria - The work of Erik Hare

Pingback: Careful What You Wish For | Barataria - The work of Erik Hare