Are you properly compensated for your work? As we discussed previously, between 1947 and 1973 worker’s salaries accounted for half of Gross Domestic Product (GDP). There was a solid if unspoken agreement that labor and capital split the spoils of the free market equally between them.

But what of output per worker? Is it possible that workers are slacking off and don’t deserve the same arrangement they had in the immediate Post WWII era? An analysis of productivity, or output per worker, shows some interesting trends that may point to more unspoken agreements that the various markets for capital and labor expect. These trends follow business cycles, and as such point to some important changes that are necessary as we move ahead into the next cycle in the next few years.

There is work to be done.

Productivity is a simple thing to define. It’s simply the net output per worker, which is to say GDP divided by the number of workers. Generally, as long as it is going up we can expect the standard of living for workers to constantly rise and economic growth to continue. It’s one of the basic underlying indicators of the long-term health of the economy.

When productivity growth seemed to be slipping back in May, a sense of panic ran through the financial press. Without rising productivity the “recovery” that we have been longing for will reasonably stall. The theory is that higher productivity makes each worker more valuable – pointing to a need for more workers to generate more profit for the company they work for.

Higher productivity means something different for workers, however. Theoretically, higher output per worker means higher salaries because each worker is worth more. But increasing use of automation has turned that upside down. Far too often, today’s productivity gains are tomorrow’s unemployment. The information age has replaced millions of clerks who pushed paper all day with online forms.

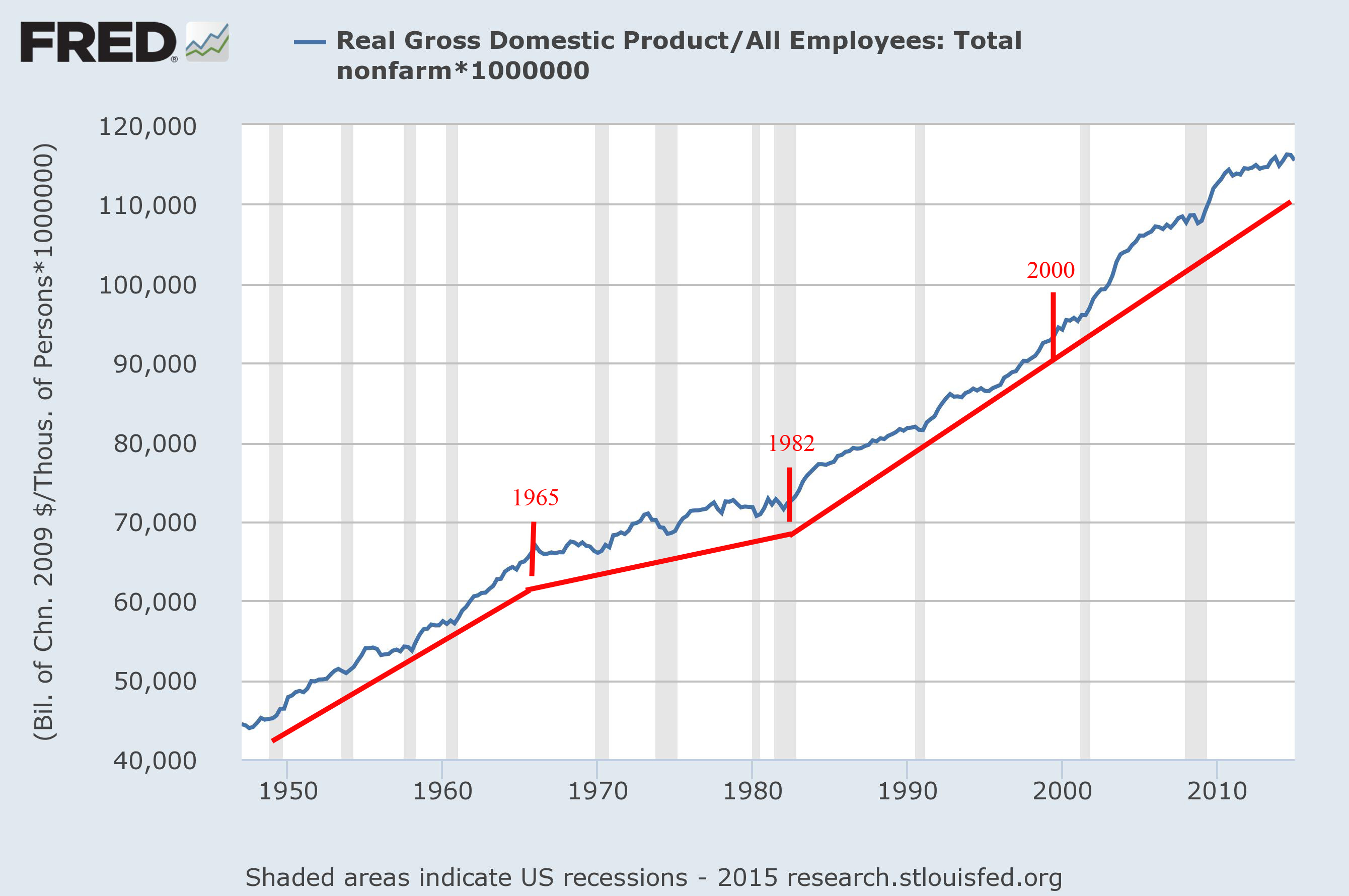

Here is the last graph from the discussion on worker’s salaries as a share of GDP, with a few additional comments. GDP is in constant 2009 Dollars:

Productivity since 1947 in constant 2009 Dollars. Data from the St Louis Federal Reserve.

The years when new business cycles started are marked with vertical lines. There are definitely trends that correspond to these cycles, which are best described in chart form:

| Start | End | Type | K-Wave Season | Productivtity Gain |

| 1947 | 1965 | Bull | Spring | $1.2k/yr |

| 1965 | 1982 | Bear | Summer | $0.3k/yr |

| 1982 | 2000 | Bull | Fall | $1.3k/yr |

| 2000 | 2017? | Bear | Winter | $1.2k.yr |

Longtime readers of Barataria will note that the “Managed Depression” that we are in started around 2000, which can be shown in many ways. The stock market today, despite being close to a record high, has not equaled the height of 2000 in real (inflation adjusted) terms, for example, so the long rise since 2010 has still not brought us back to even.

Through the four postwar business cycles, productivity has risen fairly consistently. The previous bear market period saw a significant slowdown, however, which explains the period of stagnation in stocks, wages, and eventually employment. But the most recent bear market has not experienced the same reduction in productivity gains.

Yet there is something very different about the period after 2000. Productivity gains are coming at the expense of workers and not in real gains in the economy.

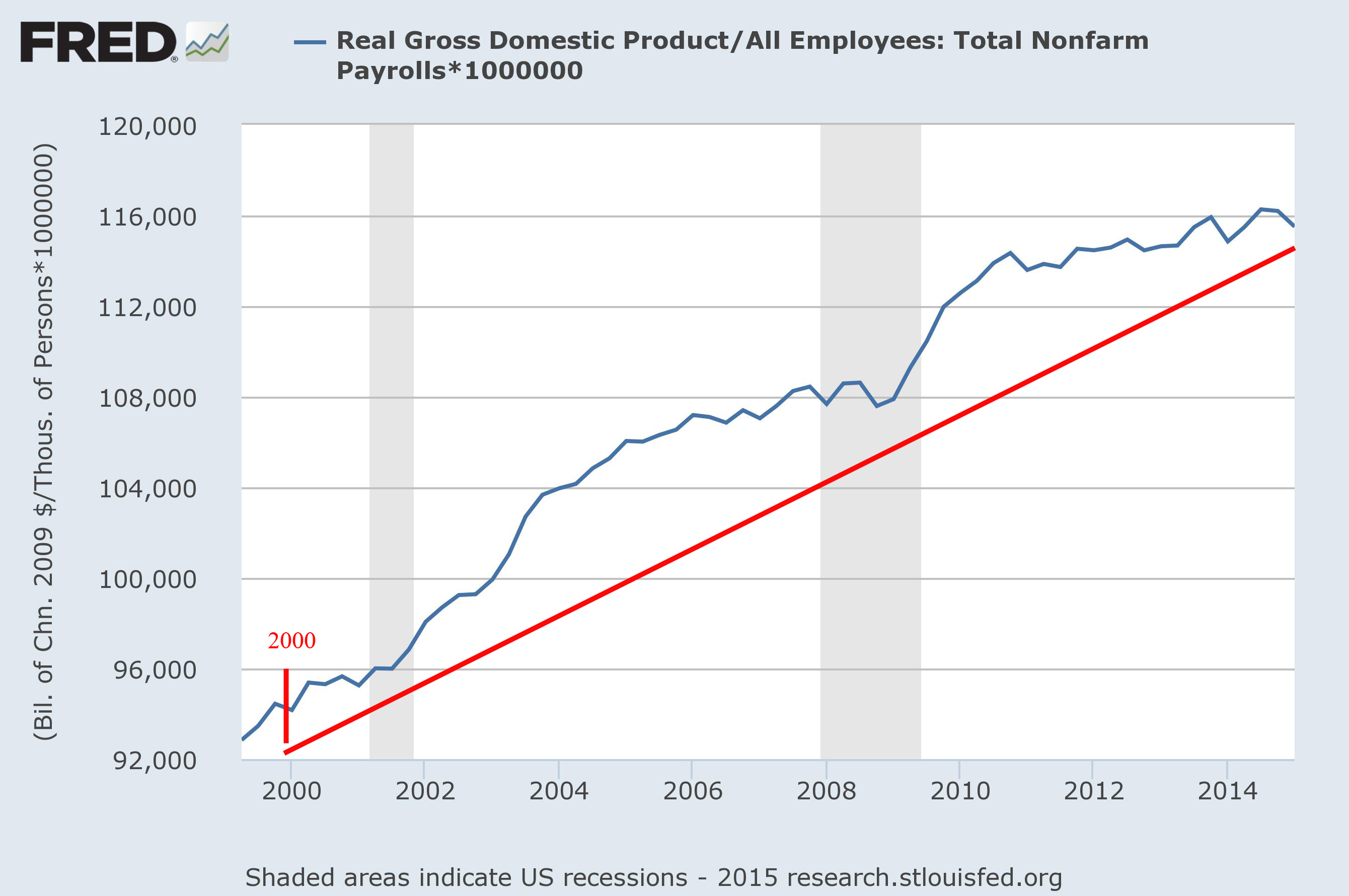

It’s worth looking at productivity since 2000 a bit more closely to see what has happened:

Productivity since 2000, in constant 2009 Dollars. Data from the St Louis Federal Reserve.

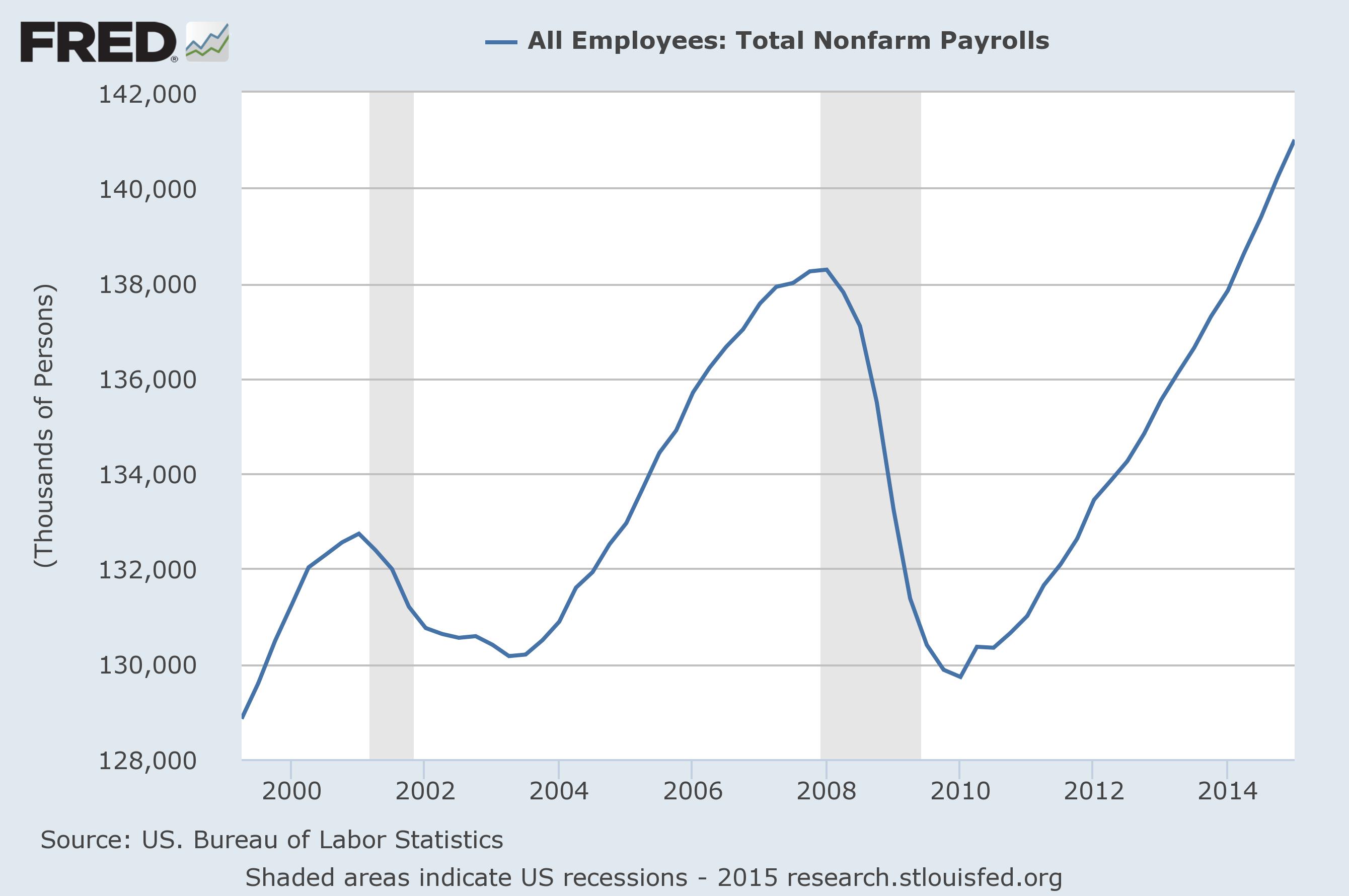

Note that when the official “recessions” of 2001 and 2008 came there was actually a net rise in productivity. By this chart, they look like good years for business even though we know they were terrible for the job loss and stock buying both. We can see what happened by paying attention to those times when productivity gains rose most substantially by comparing them to the chart of total employment in thousands in the same period:

Total employment since 2000. Data from the St Louis Federal Reserve.

The overall productivity growth was clearly maintained by shedding workers, not by actually growing. It’s as if the machinations of hiring and firing were nothing more than an attempt to paint a line on the productivity chart showing that everything was allright no matter how many people had to be fired to make it look good.

Clearly, productivity growth of $1.2k per year is expected in our world. The recent downturn in growth, which is shown in this chart, does seem worrisome. As we discussed before, hiring appears to have gotten a bit ahead of economic growth for the time being.

Oooooouch!

This is critical because these charts describe exactly what “austerity” means in this kind of downturn. The cycle that we are in, described as a “depression” or an economic “winter”, is caused by a shortage of demand for the goods and services produced. Prices can fall in a deflationary spiral if not propped up by cheap money thrown into the economy – which is exactly what policy makers have been doing through the Bush and Obama administrations.

That’s what we mean by a “Managed Depression”. It actually almost worked.

Yet the missing element that has not turned the economy around remains upward pressure on worker’s salaries. As we discussed before, the average worker’s pay would be about 16% higher if the split between labor and capital remained 50/50 as it was forty years ago. That’s about $700 per month to the average worker.

Given that this cycle is about lowered demand for goods and services, that would be a real boost to the economy.

Instead, we have downward pressure on wages which is accelerated by high long-term unemployment and many workers applying for every job at every wage. The cycle of reduced demand continues and the economy never seems to quite recover. A large wave of hiring at today’s conditions would only kill productivity numbers.

At some point you have to ask, “Who are the robots really working for?”

What can we determine from this analysis? That the current business cycle, featuring a lack of demand, is indeed perpetuated by increasing automation and reduced reliance on workers. This fits well with the classic analysis of business cycles as the process of absorbing disruptive technology through a period of first rapid economic gains followed by a bursting bubble as productivity gets ahead of demand.

Where this “Managed Depression” has been handled well in terms of maintaining a veneer of economic stability the mechanisms that have been used only accelerated income inequality by reducing demand for workers and suppressing wages.

It will end when there is a net shortage of workers, which we can still expect when the Baby Boom starts to retire in large numbers after 2017, as we have discussed before. Until that time, policies that encourage employment are essential to increasing demand for workers in order to end the spiraling lack of demand.

Austerity is exactly the wrong approach, as shown in Europe. But government spending to “prime the pump” may not be the best approach, either. The only thing that makes sense is reducing the overhead per employee and putting into practice a radical change – “Tax profits, not labor”.

Only then will workers be on a more even footing with automation in the drive for ever increasing productivity.

There are many links to previous articles, so if you want more information on a topic please follow them. Thanks!

That really makes sense. Profits are the only thing that is going up seeing how employment is all out sourced.(not going up). You’d have to get a universal agreement because there is always somewhere where the multinationals can do their thing without taxes.

Leslie

Agreed that this has to be as global as possible when we make changes, but I think there’s a lot we can do on our own. The less overhead per employee the cheaper our employees seem regardless of currency exchange, cost of living, etc. That must be a priority, IMHO. It’s very clear that labor is at a disadvantage in the US right now and anything we can do to even the score is going to help.

It is only my opinion, however, to depend upon trade as the only source to stimulate the economy is a fools game. We should supply our own territory with our own goods made here. Government policies should be supportive of that.

Leslie

I have come around to that thinking as well. One of the reasons I support a high speed rail system, for example, is that the more we can improve access for US manufacturers to the US market while reducing inventory the more jobs we can create making things for our market. It’s not always a matter of cost, after all, but a matter of customization and fashion. Speed matters, and the better our high-speed infrastructure the better our advantage in our own market vs the big containers coming from overseas.

Having said that, free trade does help as developing nations pick up. But that’s a long-term thing that should not be our bread and butter, IMHO.

Right now we are dealing with wide spread unemployment and underemployment. We still need food, clothing and shelter. To think we should depend upon other coutries to supply those needs is insane. Access to markets is crucial for sure. We are in need of big change and mind sets.

Leslie

I can go along with this. If the 50/50 split is desirable, which it seems to be, figuring out where to tax to make that happen does seem like a reasonable approach.

Exactly. There may be a lot more to it, but that is my place to start.

Reblogged this on My Blog News.

I think this has to go back to the skills gap again. I think there is one but I know you don’t. But isn’t that the real problem, that there aren’t enough qualified people to do the work that is available?

It’s not that I don’t think there is a skills gap, it’s that it seems to be very different than people think.

The old industrial model was based on learning a good foundation in school and then getting an entry level job where you would gain experience and learn. That doesn’t happen anymore. Companies are so slow to hire that when they do it’s only for a very specific, immediate need. They don’t invest in employees because there is no loyalty – which works both ways.

Also, we are in a rapidly changing economy, meaning that there will be a skills gap given that it takes time for people to learn how to navigate what’s out there. That can only be closed by time and there is little that can be done policy-wise to correct it. So we have to ride that one out, IMHO.

Is there a skills gap? Yes, I think the evidence is there. But we can’t solve it through the old model of “let’s educate the kids in what they need today.” It will take a commitment to lifelong learning, business investment in employees, and an acknowledgement that some skills are just hard to obtain immediately.

Excellent blog. BTW what happened to the old comment page?

Thanks! I don’t know what you mean about the comment page, can you elaborate?

One thing that would help workers is a higher inflation rate. But Janet Yellen is has been failing American workers.

Hey, I was wondering about something. Does a lower rate for capital skew production towards automation, or is it more likely that all capital investment needs someone to run the thing and therefor low capital cost still encourages employment?

I’m wondering if you have found anything good on the relationship between the two. I think I don’t even know what to search for. Thanks!

Ok I will check.

http://www.nber.org/papers/w21003

This author found no effect on investment.

As I understand it capital gains reduction or elimination is based on the claim shareholder dividends already get taxed and business income has already, so why tax the gains. The justification for a capital tax is that it is a wealth tax and can fund measures to enhance equality.

We know that these endless debates about the tax structure and rates have to do with the need for revenue vs. any effects on businesess, households and macroeconomics.

The reason to have higher worker salaries would be to help retain workers and keep morale up. Who wants lower wages.

What share between workers and owners is highly important because this embodies the whole fairness question about industrialization and capitalism.

OK, I think we’re totally on the same page here. Since you got all progressive there, I’ll have to allow that I really do think this is all about the market for labor and there being too many workers for the available jobs, keeping wages low.

As for investment per worker, I put together this graph: https://research.stlouisfed.org/fred2/graph/?graph_id=246736&category_id=

I don’t know what, if anything, it really means, but I can tell you that the net investment per worker has gone up 4X since 1947, and aside from some nasty bumps along the way it’s rather linear. The recent dips seem to follow the job loss, so it implies that each worker needs a net investment of about $20k worth of equipment today and that investment in capital does create jobs more than it destroys them.

I think, that is … not entirely sure yet.

Here’s another thing – with about $2.8T in capital investment, the roughly 10M unemployed (by U6) need a net bump of $200B in additional capital investment, or a net increase of 7%. It’s actually do-able.

Pingback: Bear or Bull? | Barataria - The work of Erik Hare

Pingback: Crisis and Calm | Barataria - The work of Erik Hare

Pingback: End “Quarterly Capitalism”! | Barataria - The work of Erik Hare

Pingback: Fight for $15 | Barataria - The work of Erik Hare

Pingback: A Critical Weekend | Barataria - The work of Erik Hare

Pingback: Paint the Map Blue! | Barataria - The work of Erik Hare

Pingback: Trade Deals – Bad Deals? | Barataria - The work of Erik Hare

Pingback: The Next Economy – An 8 Point Plan | Barataria - The work of Erik Hare

Pingback: Spring is Coming! | Barataria - The work of Erik Hare

Pingback: Energy Independence – and Beyond | Barataria - The work of Erik Hare