As the eight year old bull on Wall Street is slaughtered for its meat, several questions come to mind. Is the fall likely to continue? Where will it stop? And, for those on the sidelines looking to score political points, who is to blame?

The answers to these questions are easy and a little terrifying. Yes, this is going to go on for a while. It may not stop until a lot of money is lost. And while you can’t blame anyone for actions which are cyclical, you can blame those who make things worse. The US economy is a large engine, and any good mechanic knows that while you can do a few small, smart things to make it run better it is much easier to really screw it up.

Bad stock news requires a picture like this. Apparently, these traders still exist.

We need to start with what is happening. Amid record corporate profits and a labor market so tight that wages are rising, there is a lot of trouble. Interest rates are rising, meaning that money is not going to be as cheap as it has been over the eight years of rising stocks.

Ten year treasuries are currently yielding over 2.8% interest. That’s a large jump from the bottom of 1.4% set in June 2016. It means that money for expansion of businesses, new homes, and all the things which expand the economy is already much more expensive than it was just a short time ago.

And we can be sure that it’s only going to get more expensive from here.

There are three significant forces which will drive up interest rates and thus put a damper on stocks. They are Federal Reserve policy based on a need to control inflation, a lack of foreign money coming into our markets, and finally a massive increase in federal deficit spending coming at exactly the wrong time. Let’s look at each of these one at a time.

The Fed Funds Rate is Going Up

The Federal Reserve Open Market Committee meets eight times a year to consider interest rates. In 2017, the rise was slow and capped out at 1.5%. We have every reason to believe that this will accelerate. A quarter point per meeting, or an additional 2% this year to bring it to 3.5%, is far from out of the question.

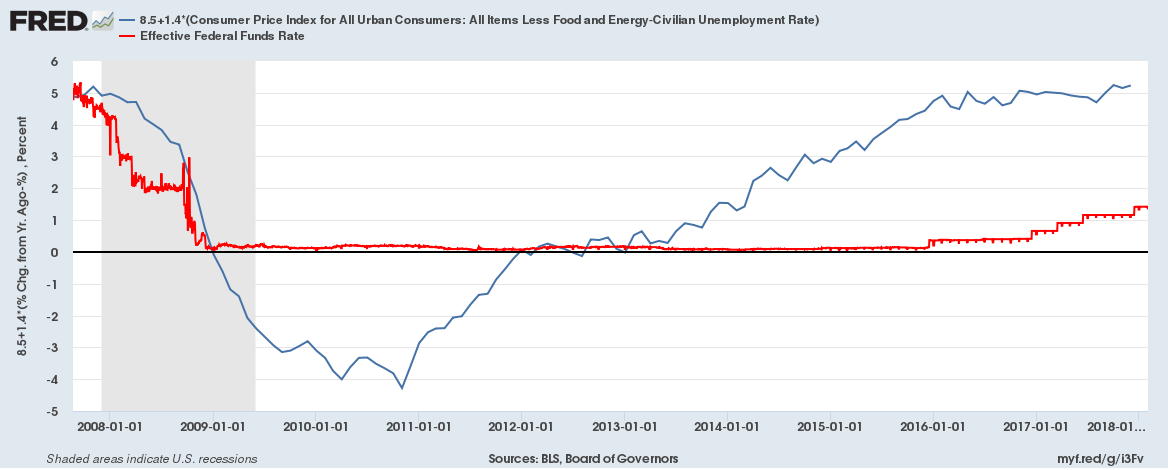

We can estimate where the Fed Funds rate should be based on an equation from economist Greg Mankiw. It’s been at least close before 2010, when it went negative:

The actual Fed Funds Rate in red, with the Makiw estimation in blue. Note that it only goes up from here.

As you can see, rates should be around 5.2% now, based on historical action by the Fed. The net gap between where we are and where we are likely to be soon is massive, larger than it ever has been. The Fed is likely to race to catch up quickly.

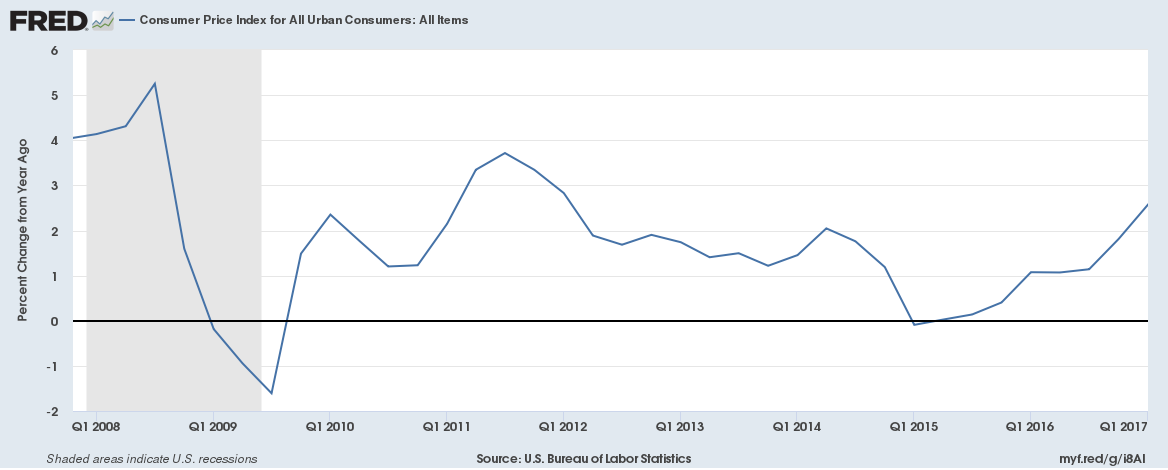

We can be sure of this because the 2% target rate of inflation has been breached already. This is caused by the same rise in worker’s salaries and the net inflows of money into the US, which we can talk about more. But what matters is that inflation is indeed taking off:

The consumer price index (CPI) since 2010. It’s firmly crossed the target of 2% and is expected to only increase from here.

Will the Fed Funds Rate hit 3.5% this year? It probably should. The last time Wall Street saw a regime of rising interest rates was over 20 years ago. Most of the traders on the floor now do not remember it. The mantra is always “Don’t Fight the Fed” in situations like this. Do they know that?

Foreign Money is Staying Home

You like your tea green or fermented?

As Barataria has discussed before, what fueled the dramatic drop in benchmark ten year treasuries, and corresponding drop in interest rates for businesses and consumers, was foreign money. Lots of it. Much of it came from China, but with Europe looking moribund the money came from everywhere. It was looking for a safe harbor, a place to sit, and nothing is safer than treasuries.

How much money? A total of $2 trillion came in from China alone between 2014-2017. Not all of that went into treasuries, but a lot certainly did. With a total publicly traded debt of $13.6 trillion there is no doubt that foreign money, peaking at the end of 2015, had a lot to do with the dramatic fall in interest rates.

With fixed dollar payouts every month, the interest rate for treasuries is essentially set by the market price. The net interest rate equals the interest payment over the value of the bond. Greater demand for bonds means the value goes up, so the rate goes down. Lower demand for bonds makes the rate go up.

China has stopped the bleeding of cash which fueled the dramatic rise in bonds and corresponding drop in net interest rates. Without that downward pressure, where would ten year treasuries have been as the Federal Reserve started raising interest rates? We’re about to find out – and then some.

The Deficit is Jumping – Bigtime

There’s always a fight.

The Federal deficit, or net need to sell treasuries, is about to rise. It was at $519 billion per year, but is expected to be $955 billion this year. The reason is a simple one – the large tax cut passed in December.

The net rise of over $400 billion in net sales was last seen in 2008, when the economy tanked. That time, however, was different, as the Fed Funds Rate was going down and ultimately set to zero. We have not seen a large increase in deficit spending at a time of rising rates for nearly 40 years, and that was catastrophic.

In October 1981, the 10yr treasury peaked at over 15%, a rate unimaginable today. It was also a period of high inflation and the Fed was determined to put a stop to it. We aren’t likely to see rates that high, given the long-term trend towards cheaper money and a much greater openness to money flows around the world.

But we can expect only more downward pressure on treasuries and even more downward pressure on stocks.

We will not know the full effect of this for over a year, but the stock market is very likely to respond through the summer. Constantly rising interest rates will start to put a damper on everything. Corporate profits may be up, but much of the rise in corporate investment has come from borrowing. That will not continue in this new regime.

Where We Go From Here

The happy daze are over.

There is no doubt that the stock market is falling for some very good reasons, and will continue to fall. Where will it land? We can’t say yet. That takes some more analysis and a few guesses as to sentiment.

We can’t underestimate the simple reality that today’s traders do not remember the last time interest rates rose dramatically or indeed the especially harsh period of the early 1980s. This will take some time to sink in, so dramatic one-day falls are only the start.

The long and short of it is that we should be prepared for a period of inflation and falling stocks. In the short term, sitting on cash looks like the way to go, but in the longer term a hedge against inflation is going to be critical. That market is simply not well defined.

Right now there is only one thing for sure – the stock market has to fall. It’s a matter of how much and how fast.

Wasn’t it just a bubble to start with? The tax cut was expected to keep the bubble going at least through the 2018 elections, if it kills the stock market instead it will only prove how stupid they really are.

It was and was not a bubble. If you believe the best case scenario, valuations were justified. If anything went wrong not so much. That’s where we are at – things are going wrong.

My prediction has been that we’ll see a market correction of about 20% over the next couple of years. Markets won’t start to rebound until the 2020 presidential elections (doesn’t matter who’s running, just the potential change in administration will shift the trend).

We are in the same range. I’m doing my best to come up with some good predictions for my next post, but to be honest the chartist people I’ve read so far are really in denial. I can’t find support levels which make a lot of sense to me.

My predictions are mostly intuitive – I don’t have hard numbers to prove it. But based on the fact that business and stock prices are cyclical, we’re over do for a fall. Also presidents tend to affect the emotions of Wall Street: optimism when a new one shows up, then depression when things don’t change as predicted and back to optimism as we throw the bum out.

Yes, but I said the same thing with more words and a few graphs. 🙂 Seriously, that is about how it goes. There are some underlying reasons as to why, for those who want to get into it, but intuition can tell you a lot as well.

To be fair, if you take the market now and look at it in 10 years it should go up. The market fluctuates but it is always slowly trending up

You said a week ago the economy was great, now your saying the stock market is overpriced. I realize they don’t necessarily relate to each other but some explaination would be good.

The market got ahead of itself, is all.

https://www.bloomberg.com/gadfly/articles/2018-02-05/stock-investors-don-t-need-to-worry-about-bonds-just-yet

This is a good article which attempts to justify the current stock market valuation. But I think it fails for the reasons outlined in the above piece.

The mark they set for justifying current valuation is a 10yr yield at 4.2%. At 2.8% they are not worried.

If you take a net spread between the FFR and the 10yr of around 1.2, as it is now, we could easily see a FFR around 3.0 and a 10yr at 4.2. But it’s more reasonable that we’ll go more in the 3.5 FFR and a more average 1.6 spread, or 5.1. And worst case is more in the 5.0 and 2.0 range in the next 2 years, or a 10yr of 7% !!

So what is the market worth? I’d say we have to lose about 20-25%, which is one Hell of a haircut. That puts the DJIA under 20k, for example, maybe as low as 18k.

It’s not that the economy isn’t strong, it’s that it’s so strong and the deficit is growing, meaning the 10yr just plain has to rise – perhaps substantially.

Reblogged this on Filosofa's Word and commented:

Curious as to why the stock market is plunging? I am not an economist, and while I have some understanding of the way the market works, I know just enough to be dangerous. So, I turn the explanations over to friend Erik Hare, who IS an economist and understands far better than I. Thank you, Erik, for well-written, understandable post!

Good summary. We knew the market had some euphoria priced in, so there is definite pull back from that (I heard one economist call it “frothiness.”). But, the interest rate rise and inflation risk is something that comes from heating up a pretty good economy which was forewarned by analysts last fall. The market will likely fall some more and stabilize for awhile or keep falling. Many economists think it will be the former, but who knows?

What concerns me most is the debt. It is expected to go from over $20 trillion to over $30 trillion by 2027 without the Tax Law change. Now, it is expected to go about by $1.5 trillion more with the change. So, not only did we not address that added debt, we made it worse. So, we will have to borrow more and the interest cost will rise and become a growing part of our annual budget. And, there will be no expense cuts this year, as it is an election year.

Per the nonpartisan Committee for a Responsible Federal Budget, we must have tax increases and spending cuts. They were adamantly against the Tax Law increasing debt. Going back to the Simpson-Bowles Deficit Reduction plan in December, 2010, they recommended $1 increases in tax revenue for every $2 in spending cuts. We have lost seven years of action and just threw gasoline on the fire.

What scares me is we have a day of reckoning coming when we have no choice. So, we you hear someone say we need only spending cuts, tell folks we cannot cut enough to solve this problem as the math will not work.

Yes, it is about the debt at some point. I’m all in favor of a budget being out of whack in a major downturn, as it was in 2008-2012. But right now it should be balanced or even in surplus.

To me, the fact that the Feds do not separate ordinary expenditures from capital expenditures is appalling. Racking up debt as a legitimate investment is one thing, but just to pay the bills? The ultimate amount is still important, but the first question we should be asking is why we have a deficit. If it’s for infrastructure, it may be justified.

So there are many ways to look at this as far as I am concerned. All of them point to this being a terrible way to run things right now. And there will be a reckoning – I think very shortly given the three things I have pointed out coming together.

Well said. Borrowing to build or improve an asset, leaves you with a higher valued asset. Borrowing to pay expenses, leaves you in a hole without the asset.

Pingback: Where Do Stocks Go Now? | Barataria - The work of Erik Hare

Dear Erik Hare,

Thanks for a little reality, “I’d say we have to lose about 20-25%, which is one Hell of a haircut. You explain this in a way that is easy to understand which I have a hard time doing.

I have been arguing that for the last 2 years, the US economy has been propped up by the trifecta of accelerating global growth, low inflation and loose central bank policies, two of which (inflation and tightening of policies/ quantitative easing by the Fed) can easily burst this bubble.

This market will be volatile.

At a time when the US is facing a dearth of employees with certain skill levels, the president is looking to cut back on legal immigration by 50%. Instead, the US could use a major influx of workers.

In short, the 2017 GOP tax cut in the way it was crafted was irresponsible and the president’s thinking on immigration and trade is short sighted..

Hugs, Gronda

Thank you. I explained a little more in the follow-up as to what to watch. Your point about controlling immigration in the face of full employment is also critical. There is often little that policy can do to make things much better, but it can always make things much worse. We are seeing that, I’m afraid.

Pingback: A Bold Prediction | Barataria - The work of Erik Hare

Pingback: Inflation is Back | Barataria - The work of Erik Hare

Bubble is super dangerous, not just for your investment but for the country itself. What are the best stocks to invest in during this volition time? We have a Breakout Alert!

I think once earnings come out in April, we will see movement to the positive

Pingback: Endgame? | Barataria - The work of Erik Hare