Inflation is back. What’s left to see is what anyone does about it.

The Consumer Price Index (CPI) for January came in at a strong 2.1% over the last 12 months. That’s above the target rate of 2.0% set by the Federal Reserve for the fourth month in a row. There will be attempts to explain it away in various ways. In the noise that will be created over this what will count is action by the Federal Reserve one way or the other.

The presses are rollin’

The final analysis does seem to have wiggle room, as Bureau of Labor Statistics (BLS) numbers always do. The last 12 months saw an increase of 2.1% overall, yes, but much of that came from a 5.5% increase in the cost of energy, led by rising gasoline prices. The “core” rate, excluding food and energy, was only 1.8% for the second month in a row.

So everything is great as long as you don’t eat or drive.

None of this should come as a surprise, but what matters most about this figure is that it is a surprise. Markets were counting on sub-two inflation holding out, despite matching December. If ever there was a sign that markets are blinded by optimism, this is it. The CPI is rising steadily and clearly above 2.1%.

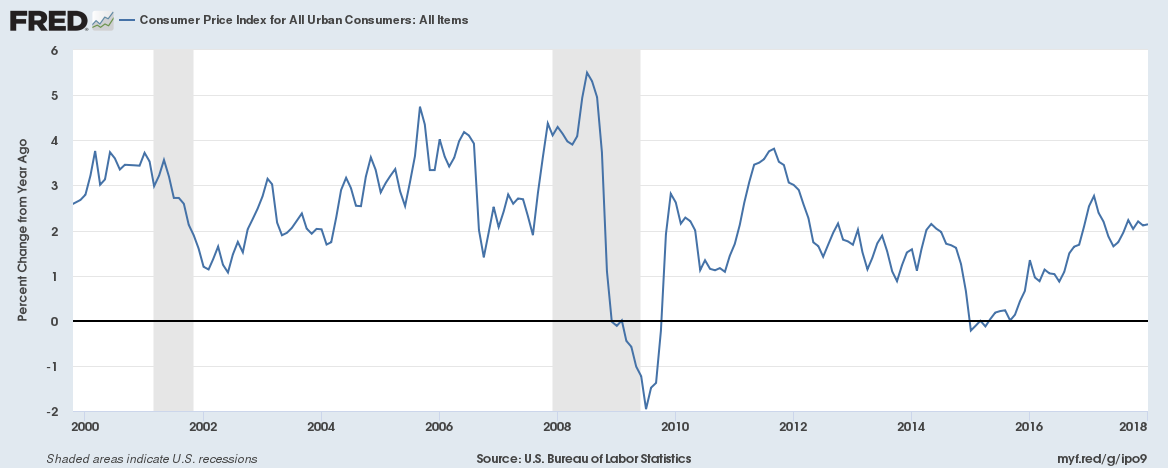

Change in the Consumer Price Index (CPI) since 2000. There is little doubt it is over 2.0% now, and rising steadily. Data from the St Louis Federal Reserve

The consensus for Fed rate hikes was three for 2018, at least until the December CPI was announced. Then, it was a hedgy 3-4 maybe. Before the January CPI announcement, prognosticators were leaning towards four.

Traders should be panicking about now.

As pointed out before, the Fed Funds Rate is far below any reasonable estimation of where it should be at this point. Eight hikes is not unreasonable, but let’s go with the consensus settling in around 4-5 for now.

That’s still ahead of where Cleveland Fed President Loretta Mester suggested just a month ago. Her prediction called for tame inflation, well below 2.0%, through 2018 and that suggested 2017’s pace of 0.75 total Fed Funds hike was about right. She saw 3-4 quarter point hikes in 2018.

We need to see where she stands now. Her vote may be a key indicator.

There will be arguments that “core” inflation is still at 1.8%, which are generally hooey. The implication is that food and energy are simply volatile and they will come down. As we reported before, this is not likely to happen for a number of reasons. Transportation costs are going to rise throughout the system and food is only likely to rise from here.

The net response from markets will also determine a lot. In early trading, 10yr treasuries looked as though they wanted to piece the boundary of a 3.0% yield, running up to 2.9%. This is going to be a strong signal to markets that bond traders are seeing more Fed action.

Money talks, but bonds have a nationally syndicated show.

Keep in mind that earlier predictions of a major market downturn were based solely on the need for government borrowing and that that does to the 10yr yield. This is on top of the demand for borrowing. We only have additional pressure as the economy overheats and calls out for Fed action.

Where will interest rates go in 2018? The question is best answered by the CPI. If you believe that 2.1% annual inflation four months in a row is some kind of fluke, you have a lot of unusually good company. Look to see if that changes in the next few days.

If it does, then we have only more pressure on the market for government debt and along with it the stock market. There is no reason to believe there is an upside to stocks right now, but a lot of potential downside.

The next month will be key. We will have our direction soon.

Rates need to go up A LOT. Inflation is definitely back.

The last few months show an acceleration. It’s very not good.

Pingback: Yes, But How is It All Screwed Up? | Barataria - The work of Erik Hare