In 1981, America stood at a genuine crossroads of the Postwar era. It seemed as though everything had been floundering for nearly a decade. Watergate, oil price shocks, and inflation were eating away at the faith and the paychecks of American workers. Millions of them had entered the workforce as Baby Boomers came of age, only to find that working life was no longer a ticket to any kind of American Dream.

Into this rode a hero as if on horseback. The assault on runaway inflation had been orchestrated since 1979, but it was about to come to full fruition. No, that hero wasn’t Ronald Reagan, it was Federal Reserve Chairman Paul Volcker. Interest rates rose to 21%, the highest the Fed has ever seen. It worked. Volcker would eventually be mythologized heavily for his role in killing inflation once and for all.

It’s an important story because inflation, the villain of the 1970s, is definitely back.

That’s the stuff.

The consumer price index rose 2.9% in June. This is considerably ahead of the Federal Reserve’s 2.0% target and similar to the 2.8% rate in May. It doesn’t appear to be accelerating, so the Federal Reserve is strangely unconcerned. “Core” inflation, which excludes the more volatile food and energy prices, is only at 2.3%.

While inflation doesn’t seem like a serious problem yet, it is likely to become one. As we’ve noted before, there is a worker shortage in many key areas, especially transportation. While the cost of finding truck drivers is going up, companies have yet to really past this on to consumers. When they do, it is likely to affect everything that is shipped – which is to say absolutely everything.

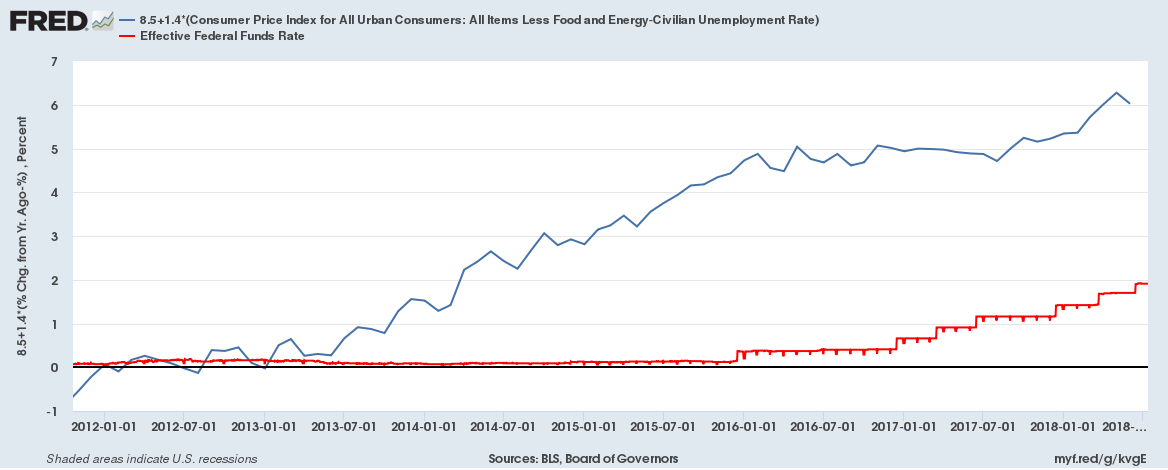

Currently, the Fed Funds rate stands at 2.0%. By the Mankiw estimation, it should be about 6.0%. That means that it not only needs to rise, it needs to rise quickly to tame inflation:

Current Fed Funds Rate in red, estimated target in blue.

But is it really that bad? In the 1980, the rise in the consumer price index hit an annualized rate of 14%, much higher than it is now. The current rate is really nothing more than the average since 1990, really. There aren’t any signs that it is accelerating, just staying higher than we’ve been used to.

Former Fed Chair Volcker

This is where Volcker’s actions become important. In October 1979, he changed the focus of the Federal Reserve away from inflation itself to the growth in money supply. He essentially put the Fed Funds rate on autopilot, freeing himself from having to explain its actions. It was an easier sell, all in all. If the net interest rate on everything went up dramatically, well, it’s just what was needed and nothing more.

The action was delayed a bit for reasons that are not clear, but by the middle of 1981 the Fed Funds Rate hit 22.4%. The resulting recession was nearly catastrophic, but it did tame inflation. No one has seriously worried about it since.

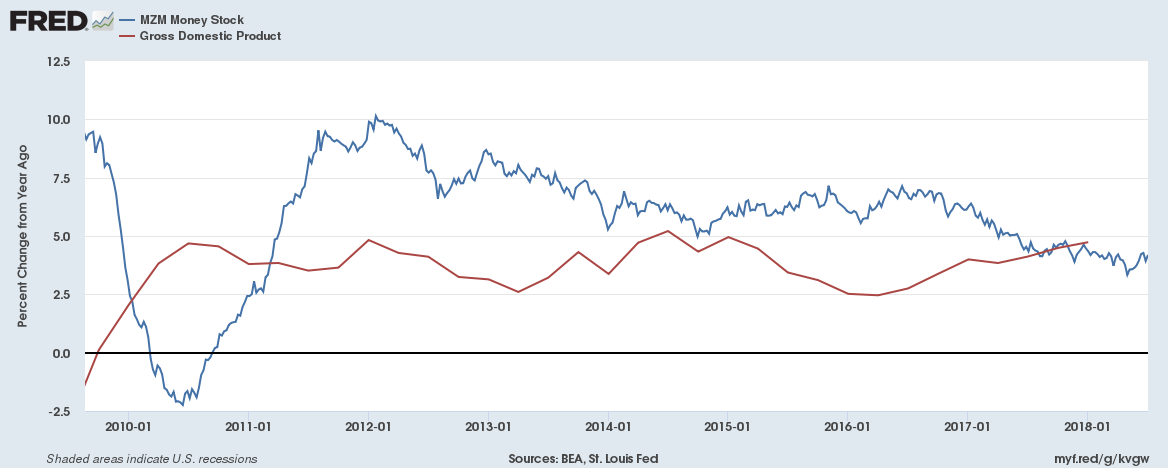

It is all about the growth in the money supply, however. Particularly when it outstrips real GDP increases over a long period of time. And we can see that it has been doing just that, too:

Money supply growth as the broad MZM, in blue with GDP growth in red. Money supply growth consistently outstripping GDP has to eventually be inflationary.

Will we see a bigger spike in inflation ahead? The short answer is that we have to, for various reasons. If wages ever do rise, it will certainly lag the effects of inflation that are already in place. That will only feed the upward spiral.

The Fed will have to increase interest rates rather dramatically over the next year in order to tame inflation, or it will risk being in a situation where a Volcker Shock is the only option. One way or the other, it’s safe to bet on higher rates. It’s simply a question of when and how much.

I totally see prices rising everywhere. Not just food and gas & gas seems to have leveled off. There is no doubt that inflation is a problem, just look at rents & how they are skyrocketing. You can’t get anything under $1000 for rent in the Twin Cities.

Pingback: Inflation is Hip | Barataria - The work of Erik Hare

Pingback: Panic, But Slowly | Barataria - The work of Erik Hare

Pingback: Capital Controls | Barataria - The work of Erik Hare