17 September is the date. We find out then, at the end of the Federal Reserve Open Market Committee (FOMC) meeting, whether or not the benchmark Fed Funds Rate is raised. Nearly everyone agrees that it’s likely to happen, either in September or in December. But trillions of dollars will be riding on the moment when the press release is issued on the Fed’s website telling people what exactly is happening.

Except for one thing – we won’t know exactly what will happen because the stock and bond markets may react in odd ways that are not easily predicted. The same is true for currency traders.

What it all comes down to is whether or not the FOMC thinks it is a good time to start or not. The arguments for and against are fairly easily summarized, but to Barataria the case is strong for a rise – especially if the net medium-term effect is that consumer rates go down.

There’s always a fight. This one is more interesting.

Discussions about the need to raise rates are more fun than many public debates because they don’t fall neatly along party lines. The more business minded Republicans tend to think that rates should go up sooner rather than later to end the distortion of the market, while Tea Party types tend to be skeptical of anything that the Federal Reserve does. Similarly, establishment Democrats tend to believe that a rate increase is inevitable while the progressive wing thinks of it as a pro-establishment job killer.

In all cases, however, a general distrust of data that suggests that we are no longer in a dire emergency is usually discounted. August’s reading of a 5.1% unemployment rate is usually met with skepticism that the numbers are all cooked. The public seems to understand what the press doesn’t – that the “headline” unemployment rate (aka U3) is rather meaningless.

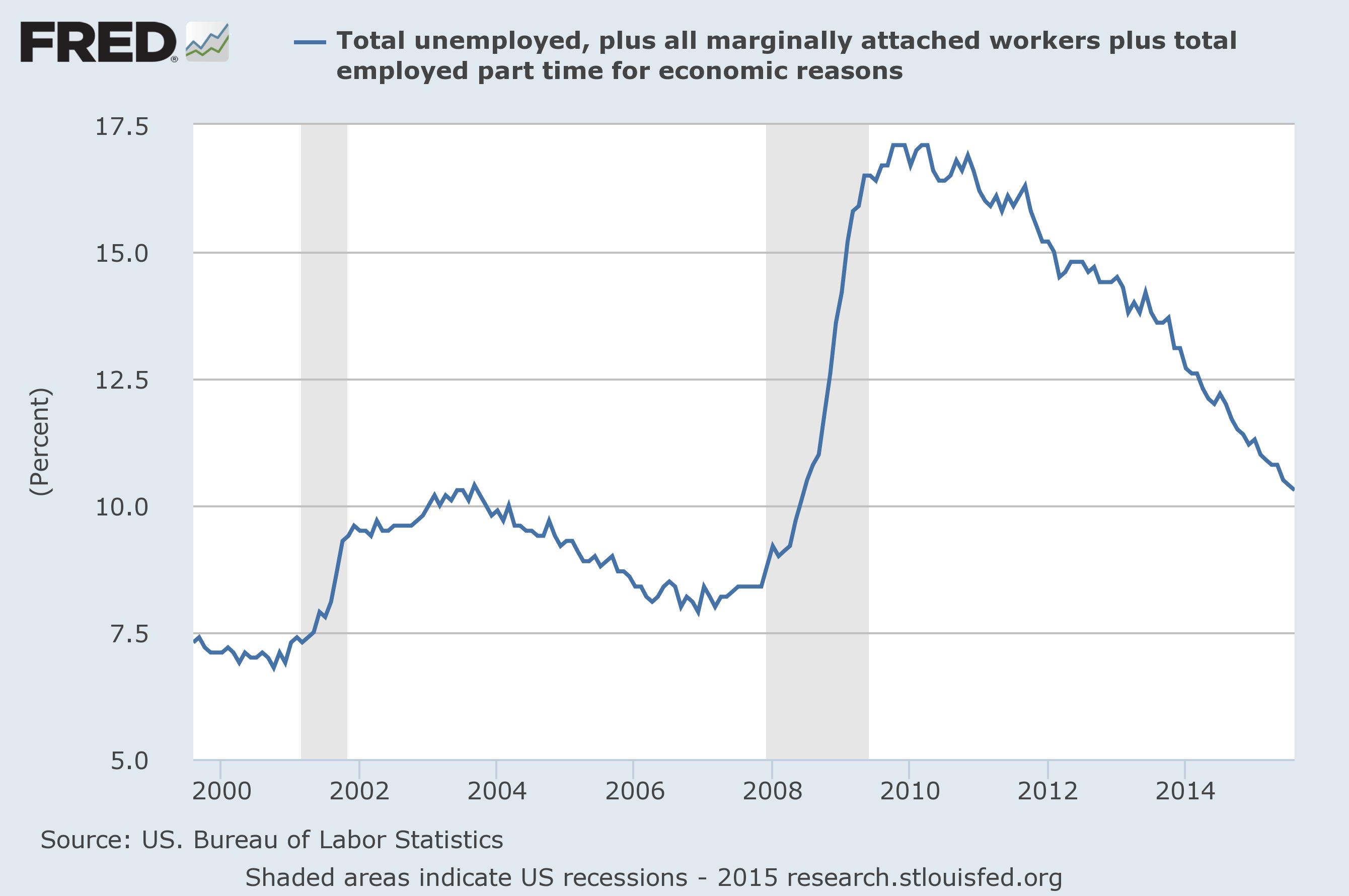

The argument using the more comprehensive U6 unemployment, which includes everyone not working as much as they’d like, probably makes the case better than anything else. The fall to 10.3% in August doesn’t sound great, but it’s a lot better than it has been:

U6 unemployment since 2000. Data from the St Louis Federal Reserve.

Note that we are finally down below the worst peak after the official recession of 2001, and that U6 has never gone below 6.8%. We can’t call this the dire emergency that created a zero Fed Funds Rate any longer. Granted, that’s about 5 million people more that don’t have the hours they want, so there is still a problem. But what is a quarter point or so in the grand scheme of things?

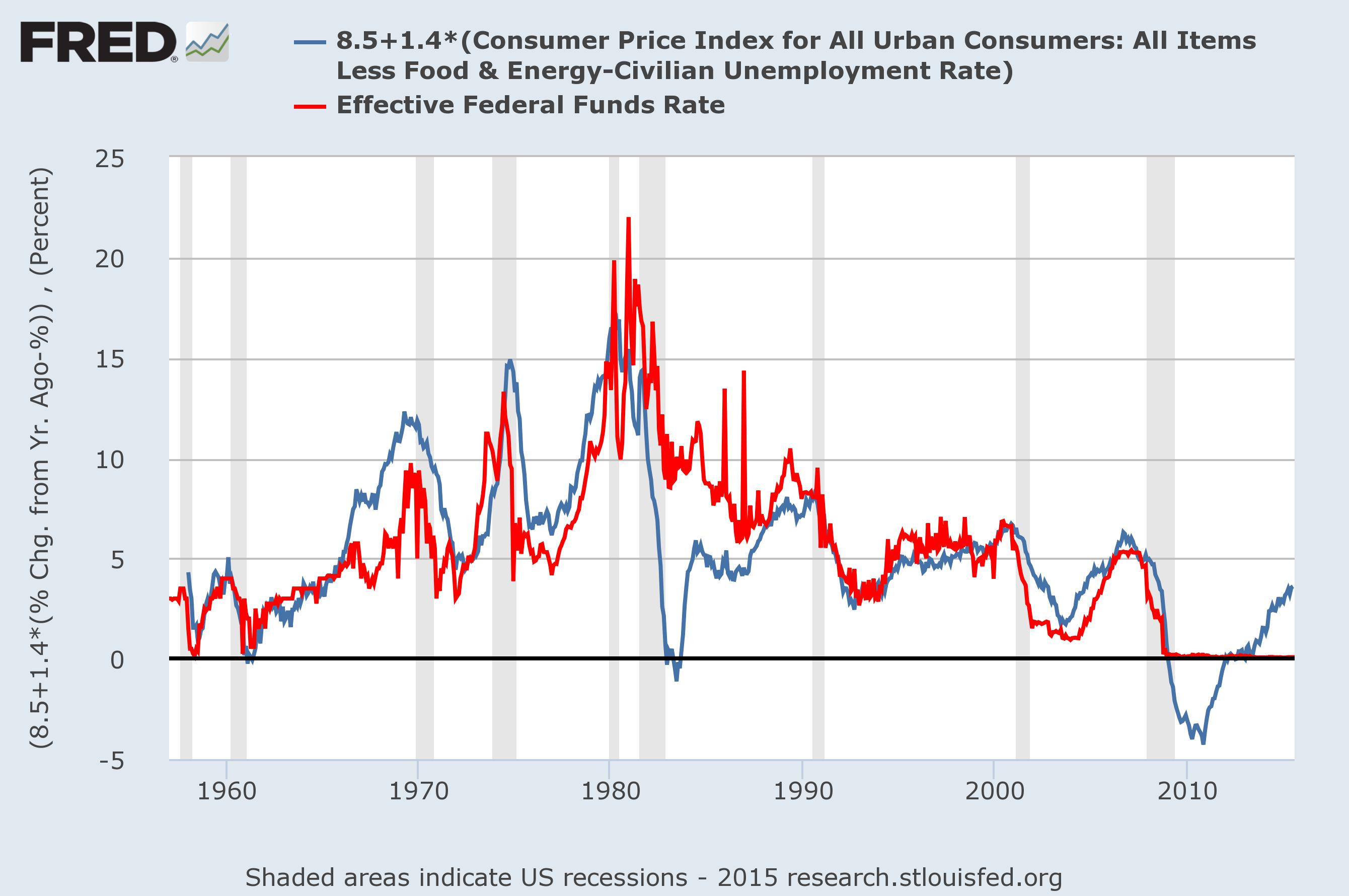

It’s worth revisiting the Mankiw Equation, a rough approximation of the Fed’s target. Named for its inventor, Harvard Professor Greg Mankiw, it has done a decent job of tracking the Fed Funds rate as far back as you want to go.

Federal funds rate = 8.5 + 1.4 * (Core inflation – Unemployment)

This balances the twin responsibilities of the Fed to maximize employment and keep inflation under control. The calculation, in blue, is shown against the actual Fed Funds rate in red:

The Mankiw Equation, in blue, vs the actual Fed Funds Rate, in red, since 1957. Data from the St Louis Federal Reserve.

Note that we should be, by this approximation around 3.6% today. And that the last time U6 was in the low 10% range the Fed Funds Rate was about 1%. We can take this as a reasonable range that the Fed is likely to target.

“This is how it is. Got it?”

No matter what, it’s a long way from zero.

So how does this play out as an argument? The idea that rates have to go up should be taken as a given. Yes, the headline U3 unemployment rate is rather meaningless, so we should use the best number we have – the more comprehensive U6. That tells us that a small rate increase makes sense as we are clearly moving towards a more normal situation.

Both sides of both parties do have a point, but there is a plenty of wiggle room between zero and 1%. A gentle start to it now only makes sense from any perspective.

But will this argument win out in a week? Stay tuned to find out.

They should have raised a long time ago. It’s like planting a tree – the second best time is today.

Good way to look at it. Watching the stock market will drive anyone nuts, even the Fed. Just do it!

I think hostility to the Fed is based, ultimately, on a correct perception that the Fed system is much closer to bankster interests than worker interests.

I am sure you are right. But I would like my friends on the left to really see that chart of interest rates and really listen to Yellen, Kocherlakota, Bullard, and some of the others there and understand how much they deeply care about working people and how they have really stuck their necks out to keep the stimulus as hot as they can for a long time in order to create jobs.

Yes, the whole system has serious problems. But there are good people in high places within it all the same. We must recognize them if we’re ever going to get anywhere.

I’ve never had much to say about the Fed, and don’t know enough to say much. But, I don’t see much discussion about whether the basic structure is appropriate, whether a more “responsible” (in the political sense) system would work better, or whether it would then move in the direction of the often irresponsible and dishonest fiscal and monetary policies we get from the President and the Congress.

The Fed deserves criticism for their regulatory functions, which I think everyone agrees are done in a very lax and chummy environment. I think they should be stripped of them and left to concentrate on being the central bank. So I consider that criticism more than valid.

But to go after them for how they set rates, especially now that they are far more open than in the past, seems really unfair to me.

I sometimes feel that everything is different now that a woman is in charge of the Fed. It seems like under Greenspan and Bernanke they could do no wrong but now they can do nothing right.

I don’t know that she is being treated that differently, but it does seem that there is a loss of respect for the Fed as an institution. Given their unusually dovish position that seems reasonable to me, which is to say I’m not sure we can blame it on her gender. But this is an excellent question. I will look through the more disparaging articles and see if I can sense any sexism.

It’s like taking off a band aid – get it over with.

Excellent analogy! Unless you want to wait for it to just fall off on its own. 🙂

9/9/2015

Re: Liftoff for continuing tighter monetary policy

Yes, anything you say, Mr. Reagan. As discussed at our confidential meeting the fed is committed to tighter monetary policy to tamp down inflationary expections, to create an optimum investment environment for Wall Street. Good call.

Truly yours,

Paul Volcker (for Janet Yellen)

Now is not time to raise interest rates. I stand stand with workers and families in opposing interest rate hikes, not with Wall Street fat cats and rich, white males.

http://www.levyinstitute.org/publications/fiscal-austerity-dollar-appreciation-and-maldistribution-will-derail-the-us-economy

From the Levy Economics Institute:

Fiscal Austerity, Dollar Appreciation, and Maldistribution Will Derail the US Economy

In this latest Strategic Analysis, the Institute’s Macro Modeling Team examines the current, anemic recovery of the US economy. The authors identify three structural obstacles—the weak performance of net exports, a prevailing fiscal conservatism, and high income inequality—that, in combination with continued household sector deleveraging, explain the recovery’s slow pace. Their baseline macro scenario shows that the Congressional Budget Office’s latest GDP growth projections require a rise in private sector spending in excess of income—the same unsustainable path that preceded both the 2001 recession and the Great Recession of 2007–9. To better understand the risks to the US economy, the authors also examine three alternative scenarios for the period 2015–18: a 1 percent reduction in the real GDP growth rate of US trading partners, a 25 percent appreciation of the dollar over the next four years, and the combined impact of both changes. All three scenarios show that further dollar appreciation and/or a growth slowdown in the trading partner economies will lead to an increase in the foreign deficit and a decrease in the projected growth rate, while heightening the need for private (and government) borrowing and adding to the economy’s fragility

This was published last May and the fundamentals of the American and world economy are weak.

Several problems with this. One is household deleveraging, which has stopped – in fact, consumer credit is expanding right now. The other is that I’m not so sure the USD will appreciate, assuming the carry trade is killed off – demand for US Dollars may go down very low, especially with commodities cheap, and drive the value of it down. Lastly, there are signs that GDP growth is accelerating and there is upward pressure on wages.

The key to it all is that stupid carry trade, IMHO. If trillions of US dollars are repatriated we will see interest rates have a net fall – or at least stay stable as the Fed Funds Rate goes up. It’s totally counter-intuitive, but reasonable. The spread between the 10yr and the FFR is at the top end of its range at 2.2% right now – if that falls back to the average 1% and the FFR is at 0.75%, we have a 10yr at only 1.75% – quite a bit lower than today. There is room for that to happen if USD is repatriated like I think it will be.

Dollars may try to repatriate if the fed increases interest rates. However things are interactive–other countries may raise interest rates or the market may devalue their currencies.

The good US data is certainly there but the stagnating or deteriorating BRIC and Europe and Japan is the problem.

Your whole running argument about inequality in the US and labor force participation rates to me says that macro should be focus not the micro of reducing low cost money.

The macro makes more sense to me, yes, the old fashioned Keynesian creating work and priming the pump stuff. But part of me believes there is no actual “macro”, which is to say I’m starting to really by the whole “Behavioral Economics” way of thinking.

But on the whole, the idea that we can increase the money supply as a way out of this seems ludicrous. Call me an old fashioned demand sider – at least for now.

Pingback: Curtain Rises on Kashkari | Barataria - The work of Erik Hare

Pingback: Careful What You Wish For | Barataria - The work of Erik Hare

Pingback: No More Games | Barataria - The work of Erik Hare

Pingback: A New Fed? | Barataria - The work of Erik Hare

Pingback: Inflation | Barataria - The work of Erik Hare