The economy has been expanding since the start of 2010. It hasn’t been rapid, and It’s only now enough to absorb the workers who need jobs, but it’s real. It’s only natural for economists to ask, “When does it end?”

That’s not because they are extremely un-fun people. It’s their job. Recessions are a much bigger problem when no one sees them coming, and history shows that we never really see them coming. And that economists are always worried about the next recession, but we don’t really listen to them.

So is it time to panic? As Groucho tells us, “There’ll be plenty of time to panic later.”

Good times. Rollin’?

It’s not just the longevity of this boom that has market watchers worried that something bad is about to happen. The top reasons for concern are always related to a bubble, or the value of investments simply getting too far ahead of real market conditions. This is in many ways a variation on the arguments in favor of a stable money supply in that rises in asset prices essentially mean that there is more potential wealth in the system. Once some people try to convert that to cash, it simply goes away. It doesn’t actually exist.

Is there a huge bubble in asset prices that will bring down the whole economy when it collapses? That is what happened in 2008 when a series of bubbles, more than simply housing, went south in a hurry. While there is a lot of worry that investment markets for stocks, bonds, and commodities are experiencing bubbles to varying degrees, there isn’t enough there to bring down the economy.

Stock prices have so little to do with the real economy that they can go up or down as they please.

It’s never all about stocks.

Another common concern is that rising interest rates are going to be a threat to the economy. After more than a decade of extremely cheap money, this is genuinely going to reshape the economy. But how much? And will it cause a recession? The short answer is that it has to slow down growth, but not necessarily turn it negative. The Fed clearly doesn’t want to run rates up quickly, although it may feel a need to catch up quickly if inflation really takes off.

That has the potential for seriously derailing everything. Like many recessions, the net result could well be that money is diverted into better investments all around, rather than simply seeking a higher yield regardless of how junky it might be. But that’s far from the only issue with interest rates.

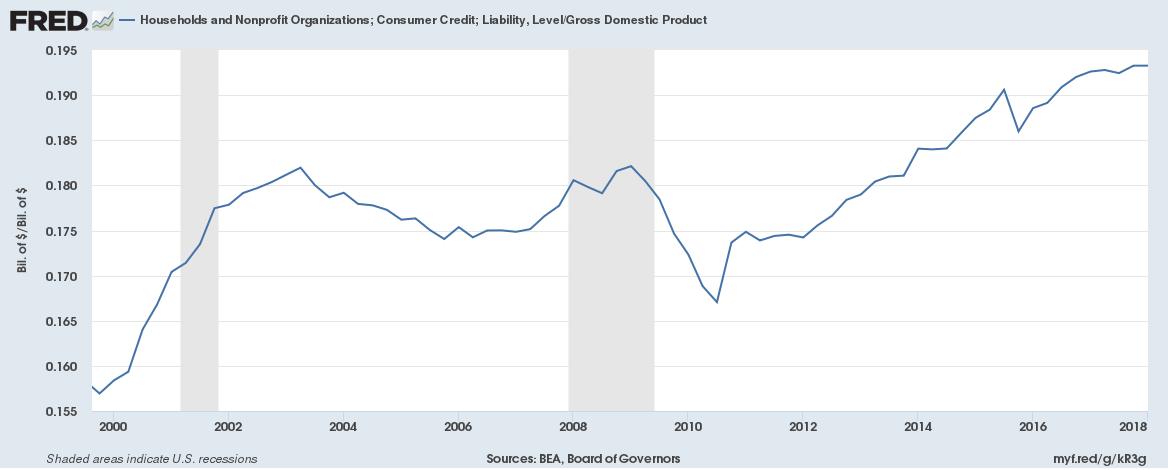

The chart below shows net consumer credit divided by GDP since the start of the last Depression. Notice a clear trend:

Consumer debt liabilities divided by GDP. Data from teh St Louis Federal Reserve

This growth is outpacing economic growth rather dramatically. Where it stood at 16% of GDP in 2000, it quickly rose to 18% through the first official recession of the 2000s – this was a big part of the inflation of the bubble. After not quite falling back down to where it started, it roared back recently and now stands well over 19%. In terms of household debt, the US is even weaker than it was in 2007.

It’s worth noting that even the 16% level in 2000 was an historic high. All of this is uncharted waters.

It’s still all about the jobs.

So is there a threat of a recession? The long and short of it is that yes, rising interest rates have a unique ability to really throttle back not just investments, but consumer spending. All of this at a time when Baby Boomer retirement is likely to keep the economy in check. At this point, the path to salvation is essentially a race between real (inflation adjusted) wages increasing to a level where consumers can pay down that debt or at least maintain spending if interest rates rise.

Is there a potential for a recession? Very much so. But the indicators most watched have nothing on the level of debt as a warning sign. It’s always the things no one is looking for that can get us, and consumer debt is definitely in that category now.

If you’d really like to panic, that’s a good reason for it.