If you want to know the future, ask the kids. It’s going to be their world one day and you can expect that it will be made in their image. Their attitudes, values, and goals will become what drives the economy once they kids of today become the parents and leaders tomorrow.

That’s why UBS asked Millenials (born 1982-1999, or currently 15-32 years old) about their financial and life goals. This is the generation that has been described as narcissistic, broke spenders among other things. If you believe that line, think again. The young people today are one of the most conservative generations yet financially, valuing happiness and security far more than a big pile of cash.

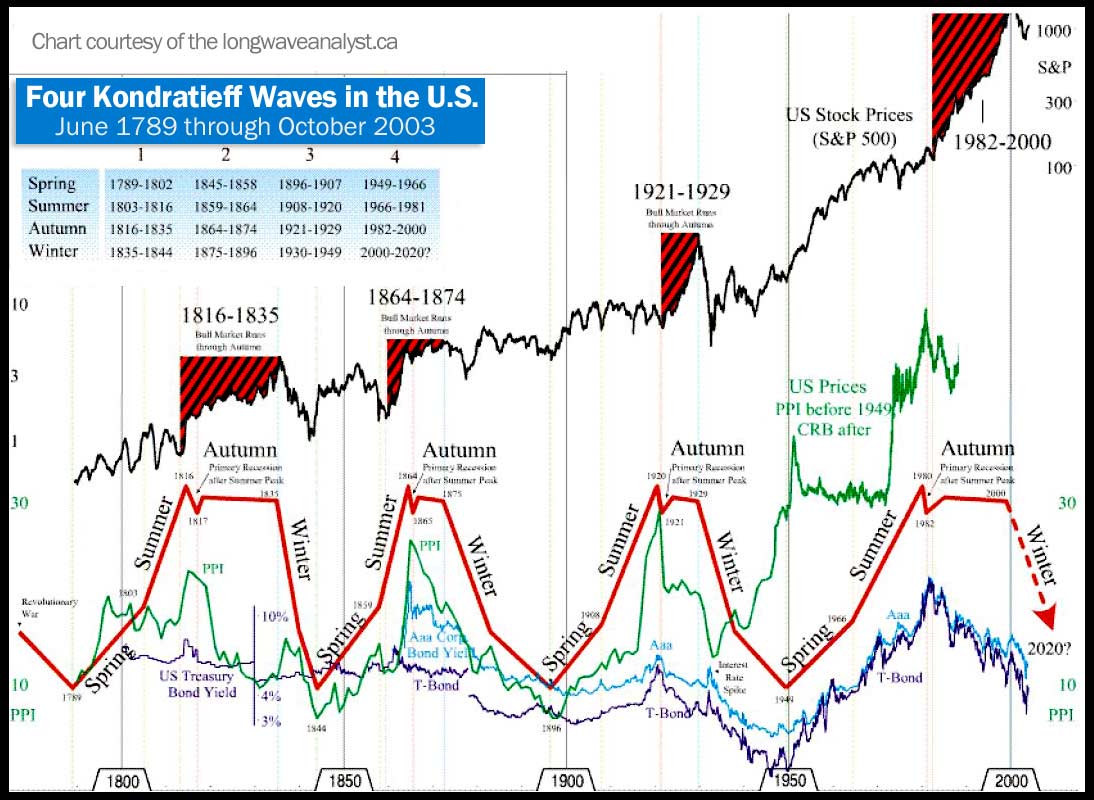

This describes our future, certainly, but more importantly it fits perfectly into the main reason why there are economic and business cycles in the first place.

They’re not all hipsters. They’re allright.

Who are Millenials? They are defined, like any generation, by the time they were born and the values and habits they learned at a young age. As kids, many saw their families struggle in the 1980s and learned to do without. The rebound of the 1990s was met with their search for a first job in after 2000, when good jobs were hard to come by.

These are mostly the kids of Baby Boomers, too, so a few values of the 1960s such as happiness and a life based on experience crept in as values taught in the cradle. We can see this reported in the very thorough UBS survey, which highlights just how much the young generation sees money as a tool, not an absolute goal.

The survey is not at all a cross section of the generation, but is a sample of people UBS saw as potential clients. It is based on the responses of 1,069 members of an affluent sub-group of millennials. Those under 30, for instance, have an income of at least $75,000 or investible assets of $50,000. Even with that the results are surprisingly conservative and show that Millenials with money to invest have more in common with their great-grandparents who also came of age in a depression.

For example, they are keeping 52% of their savings in cash and only 28% in the stock market, compared with a net 23% / 46% split for all of their elders (the balance in other investments). This portfolio strategy comes at a time in life when aggressive investment is considered both normal and healthy. But only 29% of them are pursuing an “aggressive” or “somewhat aggressive” strategy, compared with 31% for the older Gen-Xers.

For example, they are keeping 52% of their savings in cash and only 28% in the stock market, compared with a net 23% / 46% split for all of their elders (the balance in other investments). This portfolio strategy comes at a time in life when aggressive investment is considered both normal and healthy. But only 29% of them are pursuing an “aggressive” or “somewhat aggressive” strategy, compared with 31% for the older Gen-Xers.

Why so conservative? 39% consider success to come in emotional terms, with goals such as “having a happy family” and “having a meaningful relationship with my spouse”. 30% see success as being experimental, which is to say enjoying new experiences and finding meaningful work. Only 24% measure success with money, and even they are most likely to place financial freedom as their top goal.

Their top keys to success? Working hard (69% of all respondents) and saving (45%).

Missing from this survey, of course, are the young people who are struggling and can’t find work – the ones that Barataria has been keeping track of for more than a year now. They are starting to find jobs, but slowly. We can only expect that they will be even more conservative than their well-off classmates.

The reasons why Millenials are concerned with non-monetary happiness are obvious enough, given the circumstances that they grew up in. But as they age and hit their peak earning years in about 20 years they will come to dominate the economy and the financial markets. What they have learned as kids and the values they bring will dominate, meaning that high-flying casino stocks and hyped investments are likely to become investments of the past in the next economy.

This is exactly what we would expect as the next wave of the business cycle – an economic Spring that stresses fundamentals, value, and reliability. Business cycles are not an inevitable feature of the world. They are not written in stone – but they are written in blood. What people learn as kids becomes the values and value of the economy decades on. The next economy, made by these kids, will be very different from the high-flying casino that crashed hard in 2008.

Business Cycles, of “Kondratieff Waves”, since the founding of our Republic. Courtesy financialsense.com

They learned that lesson. Aggressive manipulation of money for money’s own sake won’t come back until Millenials are too old to stop it from happening, which is to say about one lifetime from now – much like the 71 year gap between the depressions of 1929 and 2000.

What is the future? In many ways, it’s the past. People learn when they are growing up and put those lessons to use all their lives. Today’s kids learned well and will make excellent stewards of the economy they will inherit. In 2017, they will be 18-35 years old and starting to dominate the job market. They’ll do very well, too, for a lot of very good reasons.

“have an income of at least $75,000 or investible assets of $50,000. ”

That must be inherited money at least for most of them.I don’t think too many kids have 50 grand to invest. Even those with a good salary are going to be paying off debt unless their parents paid for college.

I think the operative word here is “or”, but many of them did come from rich families, yes. But the hard times still left a mark all the same. I would expect the conservative nature of this generation to be even more pronounced among the middle-class and poor. I also think this begs for more in-depth questioning about why they don’t like stocks – I’ll bet they think the market is rigged and/or a casino.

Good for them! One thing missing is how much debt they are willing to accumulate in credit cards, ect. You said this is an elite group so it would be good to see how all millenials respond.

Credit card debt is declining, so my guess is that younger people are not picking up new debt, no. This poll does beg for more in depth questions and surveys of a broader population, yes.

This is what they say to the survey takers, I wonder what they really do. Any evidence?

I can’t find anything to confirm this. It’s an elite group money-wise, so you’d have to find a corresponding study of any kind on the same group. A quick search didn’t uncover anything. I’ll keep an eye out for anything similar.

US consumers may have taken on taken on too much debt in the years prior to 2008

But it is also true that unemployment rates have been lower in the US compared to the Euro area since the early 1980s. That’s a plus for the US, especially in light of the attention to employment rates in Barataria.

http://www.unc.edu/depts/europe/euroeconomics/Unemployment.php

Also GDP growth has been consistently higher in the US compared to the Euro area except for the early 2000s

http://www.unc.edu/depts/europe/euroeconomics/GDP.php

For the US and Europe these are partly policy choices as the US has a different mix of monetary policy and fiscal policy.

Inflation has been lower in the US compared to Euro area except in the middle 2000s

http://www.unc.edu/depts/europe/euroeconomics/Price%20Levels.php

Yes, the US has been doing much better than all the other developed economies – Eurozone, Japan, and even UK. That’s true over both the long and short term. So I can’t help but think we’re doing something quite right, generally.

The debt we took on may not have been so terrible – it promoted more growth generally. It would be better without , though, yes.

Good links, some useful charts there. Also, the writers included a lot of fundamentals which are very handy!

The Euro zone is weakening.

And the world wont’ have the BRICS to lean on

It is hard to say what’s up in Japan

http://www.tradingeconomics.com/japan/gdp-growth

The US will have to go it alone and rev things up. It’s up to us.

If one were to ask where was some of the credit coming from that was part of the recession. the answer would be Deutsche Bank.

Try googling litigation against Deutsche Bank

https://www.google.com/#q=litigation+against+deusche+bank

Deutsche Bank paid out $2.5 billion euros in fines and settlements

Pingback: Talking to Teens | Barataria - The work of Erik Hare